Can We Leverage Our Tools to Save Lives?

Suicide risk management for the public and insurers

February 2018 Web ExclusiveImagine you are afflicted with an aggressive, life-changing disease. The disease and/or its treatment might have excruciating side effects. Your pain may become so unbearable that you choose to end your life. With the tangible causal element of physical pain, your decision may be reluctantly accepted and, to some degree, understood by people in your orbit.

But what if your pain is emotional?

Research has shown that emotional and physical pain are experienced in the same region of the brain, but mental anguish is less tangible to others.1 We often minimize emotional pain. Those coping with emotional pain may reach a point when it overpowers their ability to cope. Suicide becomes an option, but people in that person’s orbit may be less accepting and understanding.

Dr. Bart Andrews, vice president of Clinical Practice/Evaluations at Behavioral Health Response (BHR) Worldwide, a leader in the behavioral health and addiction communities, describes several obstacles preventing people who are at risk of suicide from getting the care they need. Fear of hospitalization against one’s will is a legitimate concern. That approach is common, but sadly, its efficacy is not borne out by evidence.

Lack of access to proper care can also be a barrier, which is partly exacerbated by the lack of qualified mental health professionals to help. Most professionals, Dr. Andrews says, are not adequately trained in suicide assessment and intervention: more than 50 percent of mental health professionals do not believe they have the appropriate training or skills to work with people at risk of suicide, and only seven states require minimal post-licensure continuing education in suicide prevention.2

Suicide rates vary tremendously by country and change over time—sometimes dramatically. In 1990, the United States, the Netherlands and South Korea all had suicide rates of about 13 per 100,000. From 1990 to 1999, the U.S. age-adjusted rate of suicides per 100,000 lives drifted down to 11.5. (All age adjustments in this article use the World Health Organization [WHO] 2000–2025 standard.) Between 2000 and 2015, the rate reversed course and steadily increased to 12.5 suicides per 100,000 lives.

Figure 1 compares the progression of the annual suicide rate in the United States to those of the Netherlands and South Korea during the years 1990–2015. Their experiences have diverged in striking fashion.

Figure 1: Age-Adjusted Suicide Deaths per 100,000 Lives, 1990–2015

Source: Adapted from “GBD Results Tool.” 2018. GHDx. University of Washington Institute for Health Metrics and Evaluation.

The age-adjusted suicide rate in the Netherlands was just 8 percent lower than the U.S. rate in 1999. Since then, the Netherlands’ rate decreased and the U.S. rate increased. The Netherlands’ rate was nearly 25 percent lower than that of the United States by 2015. If the U.S. rate had matched that of the Netherlands in 2015, the death toll from suicides would have dropped by more than 9,000. Meanwhile, South Korean suicide rates in the years 1990–1994 were virtually identical to the United States at 12.8 per 100,000. By 2009, South Korea’s suicide rate climbed to more than 2.5 times greater than that of the United States.

Which direction will the U.S. rates move in the coming years? It is impossible to say, but managing suicide risk—with interventions targeted at both general and insured populations—increases the chances that we can slow or possibly reverse the increase in the suicide rate since 1999.

Suicide Risk Management

Understanding the risks across age groups is important to prevention: While ages 18–25 experience the most suicide attempts, ages 45–64 experience more lethal attempts.3 Dr. Andrews contends that current best efforts in prevention fall into three categories.

The first is limiting access to lethal means. For example, China and the United Kingdom have experienced success by limiting access to certain pesticides and to acetaminophens, respectively.4,5 Firearms account for nearly half of deaths by suicide in the United States. Figure 2 demonstrates how universal background checks and waiting periods for handguns showed significant decreases in suicide deaths.6

| Figure 2: Suicide Attempts by Means and Lethality | ||||

|---|---|---|---|---|

| Method | Fatal | Non-Fatal | Total Attempts | Percentage Fatal |

| Firearms | 22,018 | 3,878 | 25,896 | 85% |

| Suffocation/hanging | 11,855 | 2,989 | 14,844 | 80% |

| Poisoning/overdose | 6,816 | 263,822 | 270,638 | 3% |

| Falls | 1,008 | 3,334 | 4,342 | 23% |

| Cut/pierce | 763 | 113,736 | 114,499 | 1% |

| Other | 1,638 | 115,815 | 117,453 | 1% |

| Unspecified | 95 | 1,933 | 2,028 | 5% |

| Total | 44,193 | 505,507 | 549,700 | 8% |

Second, ZeroSuicide in health care has made strides in assessing and training staff to achieve a higher level of competency in suicide prevention.7 Agencies in which the system is implemented show a 75 percent reduction in suicides in a high-acuity population. “ZeroSuicide is as much about a culture change (at the agency) as it is suicide prevention tool,” Dr. Andrews notes.

Third are suicide prevention telephone helplines. The National Suicide Prevention Lifeline in the United States, which offers a nationwide approach, is one example.

Big data solutions are not yet ready to displace these prevention measures, but there is some promising preliminary work. For example, the U.S. Army partnered with the National Institute of Mental Health to use big data to identify risk factors for service members.8 Other researchers are exploring electronic medical records to determine causal risk factors for suicide9 or to gauge propensity risk.10 Research is also being conducted on social media to determine non-invasive methods of intervention.11

Managing Suicide Risk in the Life Insurance Industry

Early in my actuarial career, part of my job was to analyze claims and assemble interesting findings for the executive leadership. There was always a lot of curiosity regarding suicide claims and their impact on claims experience from quarter to quarter.

Dr. Andrews believes better risk identification strategies might mitigate financial risk and could lead to the potential for lifesaving interventions.

Dr. Andrews suggests the industry might be able to offer help at minimal cost in cases where mental health impairment might suggest greater suicide risk. He suggests that for customers who are issued insurance but are statistically identified at risk, a low-cost follow-up communication could be sent to the policyholder every six to 12 months. Non-demand caring letters of this sort have been shown to reduce suicides in at-risk populations.12 “Everyone has a role to play in suicide prevention, and low-cost communication strategies like this can have an impact and save a life.”

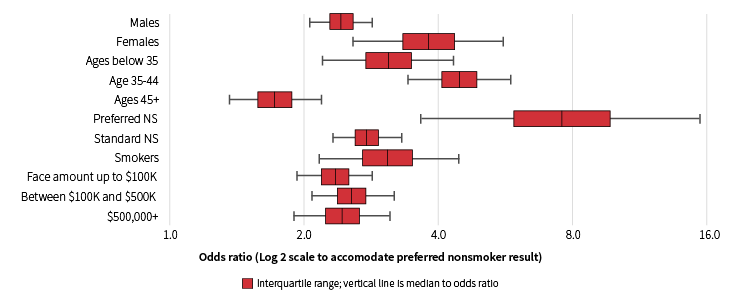

Fully underwritten life policies give insurers access to critical medical information that might signal applicants who are at risk. In a recent study, insured lives who died by suicide were paired with closely matched insured lives to study the impact of mental illness impairments. Results showed that insureds who died by suicide were 2.8 times more likely to have had a mental illness impairment at policy issue than a closely matched person without one. (An odds ratio of 1.0 would indicate there is no difference in suicides for the population under observation, and a ratio greater than 1.0 would indicate that they are more likely to die by suicide.)

Figure 3 demonstrates how that 2.8 odds ratio breaks down across various categorizations.

Figure 3: Suicide Deaths and Mental Illness Impairment Odds Ratios

Note: This figure displays odds ratios and 95 percent confidence intervals for odds that policyholders who died by suicide had a mental illness impairment at underwriting.

Source: McKinley, Jason. 2017. “Matched Pairs Analyses by Impairment and Cause of Death.” Unpublished Technical Document. RGA. Chesterfield, MO.

All cohorts have an odds ratio greater than 1.0, even at the low end of the confidence band. Confidence bands are large for preferred nonsmokers, but that should be expected since mental illness is less common in preferred underwriting classes.

The U.S. insured population suicide rates soared during the Great Recession, particularly in its peak years of 2009 and 2010 (see Figure 4). According to Dr. Andrews, suicide has a strong, demonstrated connection to cultural and economic factors. The economic changes the United States has experienced since the Great Recession have had a direct impact on our health, wellness and suicide rate.

Figure 4: Age-Adjusted Rates of Suicide per 100,000 Lives, U.S. Population Versus

RGA Insured Lives

Sources: RGA. 2017. “RGA 2005–2015 Internal Mortality Study.” Unpublished Technical Document. RGA. Chesterfield, MO.

“GBD Results Tool.” 2018. GHDx. University of Washington Institute for Health Metrics and Evaluation.

Underwriting can mitigate some of suicide’s financial risk to insurers. Figure 4 shows U.S. age-adjusted suicide rates for fully underwritten new business and for all business issued since 1997. The increase during the Great Recession and the sustained elevation since then are unmistakeable. Age-adjusted suicide rates for the total insured population even exceeded those of the U.S. population in 2009.

Research has shown that suicides increase by income quintile.13 Purchasers of life insurance are most likely to fall within the highest income quintile. However, the insured population usually has a lower rate of suicide than the general population, mostly due to underwriting. Although policies are still issued to those more at risk of suicide, pricing has also generally covered that risk.

Insurance companies typically have a one- to two-year contestability period to prevent purchase of insurance in advance of a planned suicide. A study that considered policies with a two-year contestability period indicated that some policyholders with suicidal ideation know about the contestability period and plan for it. By charting deaths by month of duration and cause of death as shown in Figure 5, the increase in suicides between the contestability period and the month following is striking.

Figure 5: Suicides as a Percentage of All Deaths by Duration Month

Source: RGA. 2017. “RGA 2005–2015 Internal Mortality Study.” Unpublished Technical Document. RGA. Chesterfield, MO.

Dr. Andrews referenced a general population study (not restricted to insured lives) that described the time frames and progressions from first suicidal ideation to attempt, giving some rationale into this phenomenon.14 “The relationship between impulsivity and suicide exists, but it is not a particularly strong relationship and is likely a distal, not proximal, predictor. Persons struggling with suicide move through a path that often starts years before an attempt, but environmental factors, interpersonal conflict and increased emotional distress can trigger an escalating reaction resulting in a suicide attempt.”

“We often operate under the mistaken notion that people battling a suicide crisis are irrational, and sometimes they are experiencing significant cognitive impairment. There is also no doubt that persons fighting suicide experience cognitive constriction and have reduced ability to problem-solve and engage in future-oriented thinking. It is certainly conceivable that the belief that their family would be taken care of financially could have an influence on a person’s likelihood of attempting suicide. In reviewing the data, it is possible that there is a group of policyholders who purchase life insurance with this intended purpose, but that the rate remains elevated suggests it may be a contributing vulnerability for those who are struggling with a suicide crisis,” Dr. Andrews says.

There are many social and emotional reasons behind suicide, and most are beyond the insurance industry’s control. Nevertheless, we are in the business of assessing risk, and our ever more sophisticated tools can be leveraged to save lives. Let us resolve to use those tools not just to help our companies attain their goals, but to enhance the lives of our policyholders and their families.

If you or someone you know needs help, call 1.800.273.8255.

I want to express my sincere gratitude to Dr. Bart Andrews of BHR Worldwide for lending his time and expertise to this article.

References:

- 1. Meerwijk, Esther L., Judith M. Ford, and Sandra J. Weiss. 2013. “Brain Regions Associated With Psychological Pain: Implications for a Neural Network and Its Relationship to Physical Pain.” Brain Imaging and Behavior 7 (1): 1–14. ↩

- 2. Schmidt, Robert C. 2016. “Mental Health Practitioners’ Perceived Levels of Preparedness, Levels of Confidence and Methods Used in the Assessment of Youth Suicide Risk.” The Professional Counselor 6 (1): 76–88. ↩

- 3. Piscopo, Kathryn Downey. 2017. “Suicidality and Death by Suicide Among Middle-aged Adults in the United States.” The Center for Behavioral Health Statistics and Quality Report. ↩

- 4. World Health Organization. 2016. Safer Access to Pesticides for Suicide Prevention: Experiences From Community Interventions. Geneva, Switzerland: WHO Document Production Services. ↩

- 5. Hawton, Kieth. 2013. “Long-term Effect of Reduced Pack Sizes of Paracetamol on Poisoning Deaths and Liver Transplant Activity in England and Wales: Interrupted Time Series Analyses.” British Medical Journal 346. ↩

- 6. Centers for Disease Control and Prevention. 2018. “Welcome to WISQARS.” Injury Prevention & Control. February 5. ↩

- 7. “Zero Suicide | In Health and Behavioral Healthcare.” Zero Suicide. ↩

- 8. Sukel, Kayat. 2015. “Big Data Help Prevent Army Suicides.” Monitor on Psychology 46 (4): 54. ↩

- 9. Karmakar, Chandan, Wei Luo, Truyen Tran, Michael Berk, and Svetha Venkatesh. 2016. “Predicting Risk of Suicide Attempt Using History of Physical Illnesses From Electronic Medical Records.” JMIR Mental Health 3 (3). ↩

- 10. Walsh, Colin G., Jessica D. Ribeiro, and Joseph C. Franklin. 2017. “Predicting Risk of Suicide Attempts Over Time Through Machine Learning.” Clinical Psychological Science 5 (3): 457–469. ↩

- 11. Coppersmith, Glen, Kim Ngo, Ryan Leary, and Anthony Wood. 2016. “Exploratory Analysis of Social Media Prior to a Suicide Attempt.” Proceedings of the Third Workshop on Computational Linguistics and Clinical Psychology: From Linguistic Signal to Clinical Reality, 106–117. San Diego: Association for Computational Linguistics. ↩

- 12. Motto, Jerome A., and Alan G. Bostrom. 2001. “A Randomized Controlled Trial of Trialof Postcrisis Suicide Prevention.” Psychiatric Services 52 (6): 828–833. ↩

- 13. Finkelstein, Yaron, Erin M. Macdonald, Simon Hollands, Marco L. A. Sivilotti, Janine R. Hutson, Muhammad M. Mamdani, Gideon Koren, and David N. Juurlink. 2015. “Risk of Suicide Following Deliberate Self-poisoning.” JAMA Psychiatry 72 (6): 570–575. ↩

- 14. Millner, Alexander J., Michael D. Lee, and Matthew K. Nock. 2017. “Describing and Measuring the Pathway to Suicide Attempts: A Preliminary Study.” Suicide and Life-threatening Behavior 47 (3): 353–369. ↩