Moving Past the Debate

The U.K. approach to resource and environment issues in actuarial work April/May 2018Statements of fact and opinions expressed herein are those of the individual author(s) and are not necessarily those of the Society of Actuaries or the respective authors’ employers.

The Institute and Faculty of Actuaries (IFoA) in the United Kingdom established its Resource and Environment (R&E) Board in early 2014. I was fortunate enough to gain a seat on that founding board, and it has been a fascinating and occasionally challenging journey. I am not, by background, an R&E actuary; my training and experience is in U.K. pensions. Working in a highly specialized environment like pensions, you get used to being the expert in the room. I don’t think many of the R&E Board members would describe themselves as “experts” with deep domain knowledge in what is such a massive and rapidly developing area, but I believe as a board we have made great strides. I also believe it is an area where actuaries can contribute, since resource and environment issues are fundamentally issues of long-term risk management. Indeed I could make a strong case that R&E issues are, at their core, financial and economic issues that also affect mortality and morbidity experience in a complex, dynamic feedback system.

This article is a personal reflection touching on some of the key themes and issues with which the R&E Board is involved. But I think it is worth saying that the very creation of this board was a major statement by the IFoA. There had been an active Members’ Interest Group (MIG) for some time, which had produced a number of thought-provoking papers and events on R&E topics. However, to elevate that MIG to full-blown “board” status signaled a real intention to lead on these issues.

While congratulating the IFoA on its leadership, my view is that this step can also be seen defensively. That is, it also flagged a determination that actuaries, in whatever sphere of the profession’s activities, should not be behind the curve on such crucial and all-pervasive issues such as those posed by climate change, of potential planetary limits to (economic) growth and of the potential for profound change that could limit the value of historical analysis in predicting the future. We live in a fast-changing world.

Since 2014, a lot of water has passed under the bridge. Many events have been held, discussions taken place, papers written. I would like to highlight a few of these in this article. I stress this is my personal view as a member of the R&E Board since its inception, and I am not attempting to cover all of the various work-streams and efforts of the past four years.

The Risk Alert

I think a good place to start in discussing the work the R&E Board has done would be our “Risk Alert.” This was issued to all IFoA members in May 2017. Risk Alerts are a series of emails from the IFoA, drawing attention to specific issues where the IFoA asks its members to think carefully about the consequences of the actions they take. The May 2017 alert states, “All actuaries should consider how climate change risks affect the advice they are providing.”1

The huge topic of climate risk can be broken down into three separate buckets: physical, transition and

The huge topic of climate risk can be broken down into three separate buckets: physical, transition and liability risk.

The alert draws on the framework developed by Mark Carney, governor of the Bank of England, in his seminal speech of September 2015, titled “Breaking the Tragedy of the Horizon—Climate Change and Financial Stability.”2 This short speech, in my view, is a model of clarity and very much worth 15 minutes of any actuary’s time to read. It decomposes the huge topic of climate risk into three separate buckets: physical, transition and liability risk. The first of these is the most obvious, representing the potential for damage caused by increasingly severe weather and rising sea levels. The second, transition risk, is a discussion of the potential to be on the wrong side of fast, severe and permanent movements in markets as the global economy shifts from a high- carbon to a low-carbon energy basis, and includes the risk of a disorderly transition. The third bucket is something we are already starting to see a lot more of: the threat of litigation for damages brought by those who are suffering the ill effects of climate change. As Governor Carney rightly predicted, the risk of litigation for loss and damage “will only increase as the science and evidence of climate change hardens.”3

The Practical Guides

For the IFoA, warning all its members (regardless of their practice area) to consider climate risks in their advice is clearly a huge step. But it begs the question, “How?”

To help to address this, the R&E Board has embarked on the production of a series of practical guides. The first of these was a practical guide for pension actuaries. It contains not only the basic background material you might expect, but it goes on to look specifically at areas of work pertinent to pension actuaries such as the strength of the sponsoring employer’s covenant, the setting of mortality assumptions and the pension fund’s investment strategy, and it discusses the sorts of questions the advising actuary might start to raise with his or her clients. See the “Resource and Environment Issues: A Practical Guide for Pension Actuaries” sidebar for more details.

The guide does not pretend to be a step-by-step manual for incorporating climate risk, or resource- and environment-related risks more generally, into the day-to-day advice given by (in this case) pension actuaries. In reality, we are all at the beginning of a journey in this respect, and there is therefore no single right answer. On the contrary, although we don’t know the right answer, our thesis is simply that we do know the wrong answer, and that is to ignore these risks and carry on regardless. We believe that would be a failure on many levels, not least of all the profession’s public interest duty as set out in its charter.

Resource and Environment Issues: A Practical Guide for Pension Actuaries

The Institute and Faculty of Actuaries (IFoA) Resource and Environment (R&E) Board has published a practical guide for pension actuaries on how to consider climate risks in their advice to clients. Here is an annotated extract from the guide:1

- Learn more about R&E risks to be equipped to discuss them with clients. (A set of references and study material is provided separately.)

- Encourage trustees to raise R&E issues in discussions with their covenant adviser and the employer. (Again, a set of questions on this topic is provided separately.)

- Find out how your clients are addressing R&E risks in their investment processes and consider whether your funding advice is consistent with these risks.

- Review whether your models adequately incorporate R&E risks and whether the documentation is adequate.

- Use scenario analysis to explore uncertainty in financial and demographic factors arising from R&E issues.

- Help trustees adopt an integrated risk management approach that includes R&E risks.

- When giving advice, communicate your approach to R&E risks and the associated uncertainty.

1 Hails, Robert, Jake Attfield, Evie Calcutt, Ruairi Campbell, Andrew Claringbold, Laura Duckering, Stuart Gray, Scott Harrison, Claire Jones, Stephan Le Roes, and Nick Spencer. 2017. “Resource and Environment Issues: A Practical Guide for Pension Actuaries.” Institute and Faculty of Actuaries. July 18. https://www.actuaries.org.uk/documents/practical-guide-pensions-actuaries.

We recently produced a more detailed follow-up paper that looks specifically at mortality and how resource and environment issues might affect U.K. mortality rates. The paper also drills into questions such as the effects of air quality and of temperature-related death rates. Similarly, a more detailed follow-up paper discussing sponsor covenant has been issued. A practical guide specifically for actuaries working in defined contribution (DC) pensions is forthcoming, and others focusing on practice areas such as general insurance and life insurance are planned. The target is to produce two to four guides per year. This is ambitious, particularly as we rely entirely on volunteers, but we intend to build a strong corpus of background information and assistance that distills these vast and complex topics so that actuaries can start to explicitly incorporate these fundamental risks into their work in a meaningful way.

The work of the IFoA R&E Board goes well beyond producing general guidance and material for actuaries in established practice areas such as life or pensions. We also spend significant time and effort thinking about and responding to specific questions and consultations. I would like to highlight one of these areas in particular, as I believe it has potentially far-reaching ramifications. This is the consultation and resulting recommendations of the Financial Stability Board’s Task Force on Climate-related Financial Disclosures (TCFD). The recommendations, if implemented widely, have the potential to have an impact both directly and indirectly on the work of many, if not all, actuaries. The IFoA responded to the Task Force’s consultation and strongly supports what have become known as the Bloomberg Recommendations, named after the Task Force’s Chair, Michael Bloomberg.

The Bloomberg Recommendations: “What Gets Measured Better Gets Managed Better”

In the United Kingdom generally, the fact that there is a scientific basis for concern over the effects of climate change is no longer an active debate. Rather, it is more common to get push-back on the question of what to do about this risk, and in some quarters, the view seems to be more or less that we should not worry overly about it. Technology will sort it all out, and omniscient, perfectly working, perfectly efficient markets will at all times ensure a smooth incorporation of the true price of this climate risk, such that market signals will automatically and seamlessly move us from the current paradigm into a low- or zero-carbon future.

While existing laws throughout the G20 require corporate disclosure of material risks, when it comes to climate risk, at best this tends to be relegated to a sustainability report and confined to information about levels of greenhouse gas emissions.

While existing laws throughout the G20 require corporate disclosure of material risks, when it comes to climate risk, at best this tends to be relegated to a sustainability report and confined to information about levels of greenhouse gas emissions.Suffice it to say that this line of thought does not accord with good actuarial risk management practice. The Financial Stability Board (FSB) was so concerned about the possibility of severe financial shock that it established the TCFD. With one eye firmly on the crisis of 2008, the FSB worried that a lack of information about (climate) risks could lead to a mispricing of assets/misallocation of capital, and potentially give rise to concerns about global financial stability “since markets can be vulnerable to abrupt corrections.”

While existing laws throughout the G20 require corporate disclosure of material risks, when it comes to climate risk, at best this tends to be relegated to a sustainability report and confined to information about levels of greenhouse gas (GHG) emissions. Generally, such reporting never touches the all-important financial pages of the report and accounts.

Bloomberg’s task force was asked to design “disclosures that will help financial market participants understand their climate-related risks … [that] … could promote more informed investment, credit and insurance underwriting decisions” and, in turn, “would enable stakeholders to understand better the concentrations of carbon-related assets in the financial sector and the financial system’s exposures to climate-related risks.”4

The resulting report is very detailed, but boils down to four recommendations for forward-looking disclosures about climate risk that should appear within an organization’s financial filings.

The recommendations are for voluntary adoption but, as of Dec. 12, 2017, 237 companies with a combined market capitalization of more than $6.3 trillion have publicly committed to support the initiative. Naturally this includes a number of large insurance companies. However, I believe all actuarial practice areas will feel the impact. The recommendations specifically extend to asset owners as well, including public and private sector pension plans. The recommendations clearly speak to the entire length of the investment chain, from issuance to credit rating, from stock exchanges to investment management.

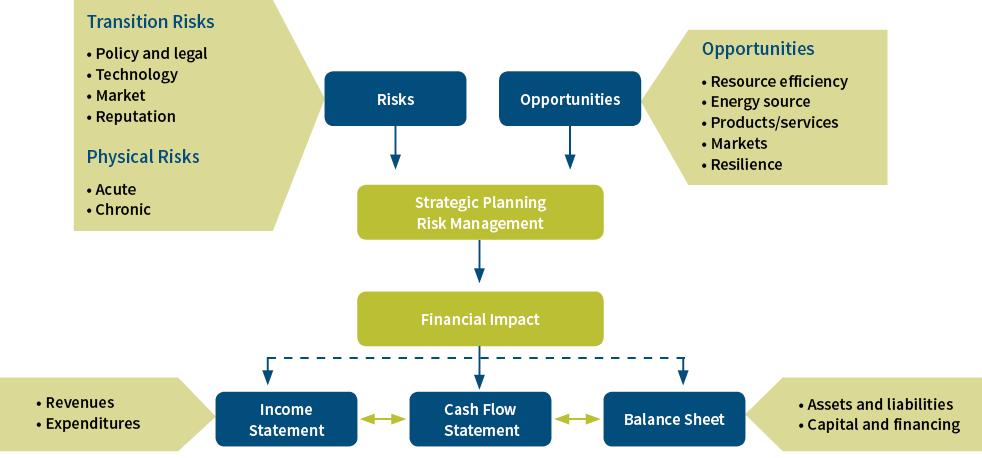

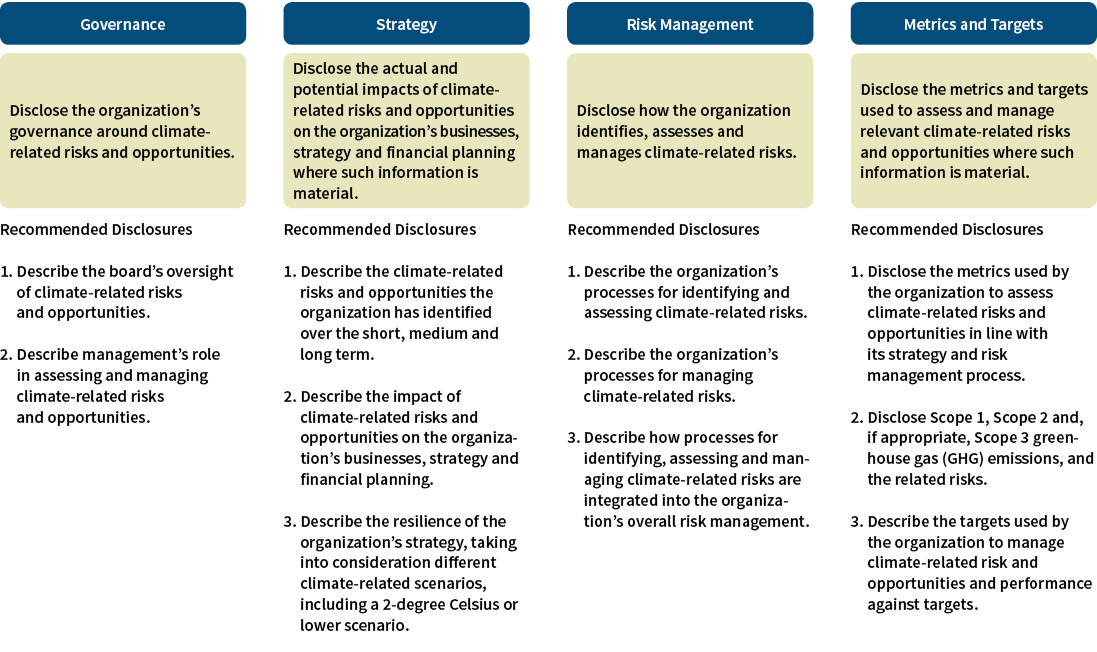

For me, there are two key diagrams in the final set of recommendations that go a long way to summarize the issue (Figure 1) and the proposed approach (Figure 2).

Figure 1 Climate-related Risks, Opportunities and Financial Impact

Source: Task Force on Climate-related Financial Disclosures. 2017. Final Report: Recommendations of the Task Force on Climate-related Financial Disclosures. June. https://www.fsb-tcfd.org/wp-content/uploads/2017/06/FINAL-TCFD-Report-062817.pdf.

Figure 1 deals with risk, opportunity and impact. Any actuary can immediately see this will apply directly at the corporate level for those working in general insurance. However, it also has pertinence in the life sector, via impacts on mortality (changing patterns of extremes of heat/cold, flooding and severe weather deaths, increased energy and food prices, disruptions to economic growth and consequential health care knock-on effects, changing disease-borne vectors, water and air quality issues, food security, etc.). But most obviously, it affects companies in the general economy, which means share prices and debt ratings. And I mean all companies, not just the oil, coal and gas majors. Every company relies on energy and transport to get products to customers. Therefore, the same logic applies to pension and investment actuaries, too.

Figure 2 Recommendations and Supporting Recommended Disclosures

Source: Task Force on Climate-related Financial Disclosures. 2017. Final Report: Recommendations of the Task Force on Climate-related Financial Disclosures. June. https://www.fsb-tcfd.org/wp-content/uploads/2017/06/FINAL-TCFD-Report-062817.pdf.

Figure 2 starts to unpack the recommendations. These FSB-endorsed recommendations, accepted by the G20, pertain to all actuaries since they directly apply to all insurance companies, investment managers and pension funds. In terms of reporting, it is true that some asset owners (pension funds) have no public reporting requirement, while others provide for extensive public reporting. For purposes of adopting the task force’s recommendations, asset owners should “use their existing channels of financial reporting to their beneficiaries and others where relevant and feasible.”

Asset managers should also up their game, providing more detailed reporting, including “items such as the aggregate carbon intensity of the portfolio compared with a benchmark, the portfolio’s exposure to green revenue (and how this changes over time) or insight into portfolio positioning under different climate scenarios.”

It will take some time to fully digest the TCFD recommendations. However, the approach has been, from the start, an industry-led one, with task force members from across the G20 with different sectors represented, each with competing interests, different politics and legislative tensions. Yet it has come together very quickly and reached consensus to deliver a coherent set of detailed proposals.

Key to this is the shift to financial disclosure. GHG emissions disclosure is all very good, but really the big question is what does it mean for P&L and the balance sheet? Thus the disclosure should now sit within the financial statements. This has implications for corporate risk/audit committees and for auditors themselves. Further, these disclosures will need to be forward looking, not just backward reporting. This is the hardest and most bold piece of the puzzle and will require the preparation and publication of detailed and coherent future scenarios of the financial implications for the reporting entity of the potential impacts of a “two degree economy.” That is, a world in which the current best estimates of the preconditions for keeping global warming to under 2 degrees Celsius are attained. A future economic scenario based on a complex dynamic system? Sound like an actuarial discipline? It does to me. I said earlier I would return to the subject of scenarios. I think that Bloomberg and the FSB are putting complex scenario generation at the heart of all financial disclosures. Actuaries have a chance therefore to put themselves in that same place, at the core of the analysis, no matter which type of actuary they are. The opportunity is immense, as will be the need, as there are no ready-made solutions out there.

The scope of the recommendations covers all listed companies, plus, as I have said, asset owners and managers throughout the G20, reaching some 80 percent of all global economic activity. It is very clear that some of the most powerful institutions in the world are becoming ever more serious about the potential impacts of climate change.

As I said at the outset of this article, in the United Kingdom and throughout Europe, the debate on climate change has moved on, and now the argument concerns the timing and the means by which targets will be met. I am aware that in the United States and Canada, the climate debate is far more politicized. But with the explicit endorsement of so many companies (including more than 150 financial firms, responsible for assets of more than $81.7 trillion), it may well be that whether you happen to agree with it, this train is leaving the station and the agenda is being transformed. The IFoA is therefore making these Bloomberg Recommendations a key focus for raising awareness within our actuarial communities.

References:

- 1. Institute and Faculty of Actuaries. 2017. “IFoA Warns on Climate Change Financial Risks.” May 12. https://www.actuaries.org.uk/news-and-insights/media-centre/media-releases-and-statements/ifoa-warns-climate-change-financial-risks. ↩

- 2. Carney, Mark. 2015. “Breaking the Tragedy of the Horizon—Climate Change and Financial Stability.” Bank for International Settlements. Speech, September 29, 2015. https://www.bis.org/review/r151009a.pdf. ↩

- 3. Ibid. ↩

- 4. Task Force on Climate-related Financial Disclosures. 2017. Final Report: Recommendations of the Task Force on Climate-related Financial Disclosures. June. https://www.fsb-tcfd.org/wp-content/uploads/2017/06/FINAL-TCFD-Report-062817.pdf. ↩