Understanding Nature-related Risks vs. Climate Risks

A paradigm shift for financial institutions

August 2024The Conference of the Parties (COP) is a governing and decision-making body of certain United Nations (UN) conventions. Alongside the COP to the UN Framework Convention on Climate Change—an important annual event—another significant gathering has run in parallel since 1994: the UN COP to the Convention on Biological Diversity. While typically getting less media attention, the latter is no less crucial. The most recent Convention on Biological Diversity marked a historic milestone with the establishment of the Kunming-Montreal Global Biodiversity Framework. This framework paves the way toward sustainable economies in harmony with nature, outlining four overarching goals to be met by 2050 and 23 actionable targets for signatory countries to achieve by 2030.

The framework aligns with a growing global awareness of our economies’ inherent reliance on nature, but it contrasts with the ongoing degradation of natural systems due to human activity. This awareness notably is reflected in the World Economic Forum’s The Global Risks Report 2024, where the top four risks in terms of potential severity over the next decade are related to nature. Moreover, there is a shifting landscape in identifying and managing nature-related risks and opportunities as more tools and frameworks emerge, such as the Task Force on Nature-related Financial Disclosures (TNFD). These developments could help various industries get up to speed, including the financial services sector where many actuaries operate.

The Specifics of Nature-related Risks

Nature-related risks are the potential threats to an organization stemming from its (or society’s) dependencies and impacts on nature. These risks may manifest as financial losses when ecosystem services—benefits derived from various natural resources constituting natural capital—that businesses depend on are adversely affected. Analogous to risks associated with climate change, nature-related risks can be broadly categorized into two main types: physical and transition.

While transition risks related to climate and nature share similarities—stemming from policy changes, technological advancements and so on—the perspective on physical risks differs. Nature-related physical risks encompass sudden or gradual impacts on natural systems and are broader than those triggered by climate-related events. It’s also important to note that while climate impacts are global in nature, dependencies on and impacts to nature are often specific to a particular location. For instance, an organization may rely on water flow at a specific plant to produce goods or affect water quality while producing those goods.

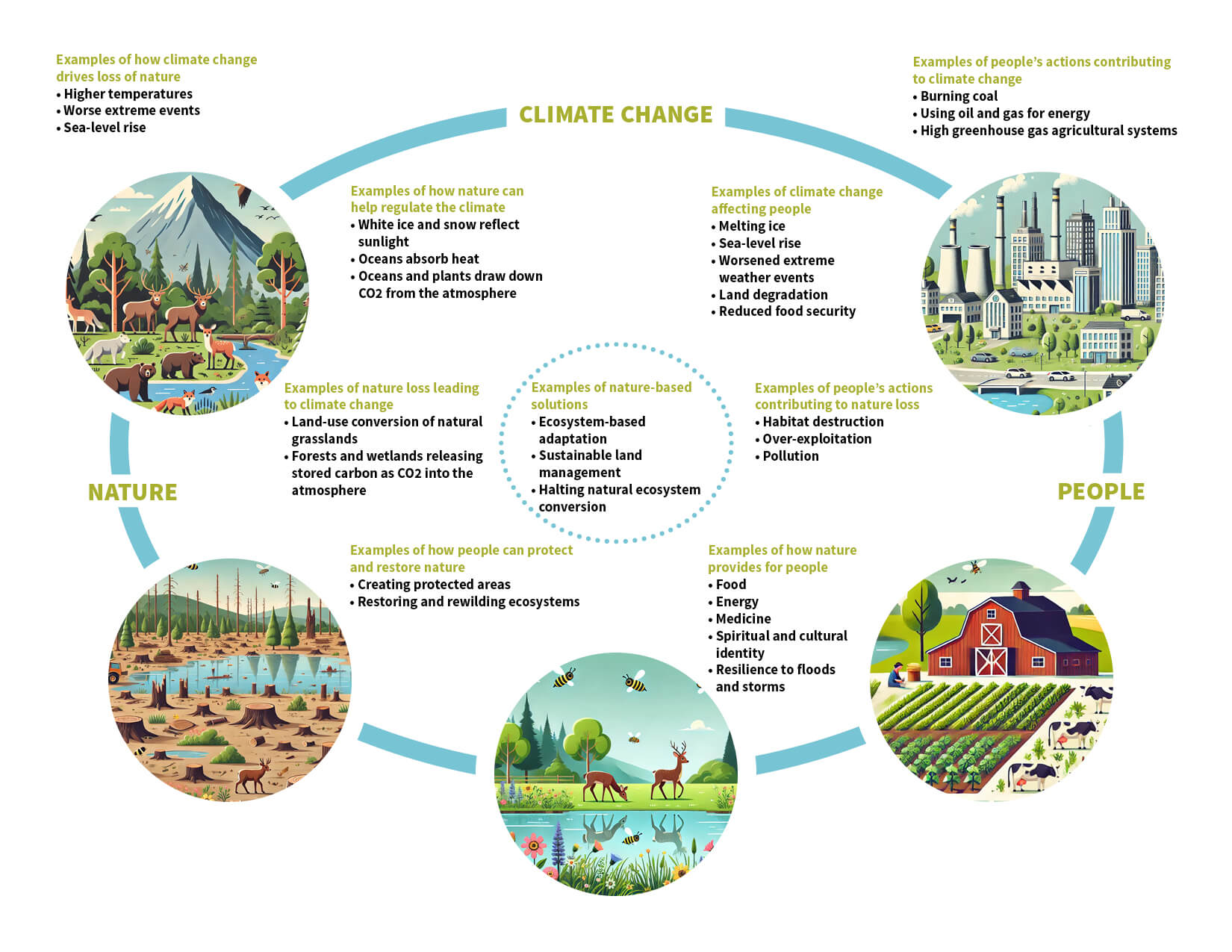

When contemplating nature-related considerations, I believe it’s crucial for companies to explore their interplay with climate and human activity. More specifically, the connection between nature and climate embodies a complex web of synergies and trade-offs, where interactions can yield both positive and negative outcomes. These can be categorized into four key pillars:

- Climate change drives nature loss. The 2019-2020 Australian wildfires, exacerbated by a combination of climate effects (drought, high temperature and low rainfall), killed or displaced an estimated 3 billion animals.1

- Nature is fundamental for climate mitigation and adaptation. Wetlands have the ability to both sequester carbon and protect surrounding areas from flooding.2

- Nature solutions can affect the climate negatively. Desalination, a common process used to address water scarcity, is mostly generated using fossil fuel energy.3

- Climate action can affect nature negatively. Solar and wind farms that require large land areas can destroy natural areas and cause wildlife fatalities.4

While acknowledging the added complexity, particularly as many financial institutions are still navigating the specifics of the climate domain, I believe it’s imperative to account for this interplay within a comprehensive climate strategy and risk management framework. Failure to do so may lead to future decisions being made with incomplete information, hence the recent trend among financial organizations to address nature and climate considerations in an integrated manner. See Figure 1 for examples of how climate change, people and nature are interconnected.

Figure 1: Interactions Between Climate Change, People and Nature

Click Image to Enlarge

Source: World Wildlife Fund

The Role of Financial Institutions and Actuaries

It is widely acknowledged that financial institutions play a crucial role not only in climate action but also in global nature protection and restoration efforts. As institutional investors and economic facilitators, they have the capacity to invest in, finance or insure initiatives that foster positive outcomes for nature, thereby unlocking new business opportunities and bolstering long-term profitability. Moreover, financial institutions are well-positioned to understand and effectively manage associated risks.

It’s important to underline the unique risk profile of insurers since they are exposed to nature-related risks on both sides of their balance sheet. For instance, the destruction of natural barriers like coral reefs, which serve as protection against storm surges, can result in increased property losses (for property and casualty insurance). Similarly, declines in plant and fungi populations, vital sources of ingredients for both modern and traditional medicines, can have secondary impacts on human health (life and health insurance). Additionally, shifts in public policies pertaining to nature can adversely affect corporate business models, thereby impacting investment portfolios.

Another significant uncertainty lies in the evolving regulatory landscape. While financial institutions are familiar with navigating regulatory changes, the realm of nature-related regulations presents unexplored territory, similar to the challenges faced in the climate sphere a few years ago. Drawing from the trajectory of climate regulations—many of which are based on recommendations that originated with the Task Force on Climate-related Financial Disclosures (TCFD), which disbanded in late 2023, and the International Sustainability Standards Board (ISSB) S2 standards, we can reasonably anticipate future developments. The recent ISSB announcement regarding a research project on nature-related risks and opportunities, informed by initiatives like the TNFD’s work, offers insights into the regulatory direction.

Anticipating that the TNFD’s proposed framework will heavily influence the future landscape, it is appropriate for financial institutions to familiarize themselves with these recommendations. Inspired by the structure of the TCFD’s framework, four key pillars anchor the TNFD’s framework as well:

- Governance

- Strategy

- Risk and impact management

- Metrics and targets

Thus, financial institutions might leverage their existing work in climate-related initiatives to integrate nature considerations effectively. Moreover, TNFD’s additional guidance for financial institutions, in conjunction with global recommendations, may serve as a foundation for incorporating nature considerations into existing frameworks through current-state assessments, gap analyses and the establishment of roadmaps.

For More Information

- Access the SOA’s Catastrophe & Climate Newsletters.

- Read the SOA’s latest Quarterly Global Warming report.

Of particular interest to actuaries are the last two pillars: risk and impact management and metrics and targets. It is here that their quantitative skills come into play, from conducting materiality assessments to performing scenario analysis and developing key risk indicators. Actuarial bodies worldwide also have issued papers that advocate for greater engagement of actuaries in this field and dig deeper into potential methodologies.

The following are great North American examples:

- A recent report by the Canadian Institute of Actuaries (CIA), “Integrating Nature in Climate Scenario Analysis for Enhanced Resilience,” underscores the pivotal role actuaries can play in integrating nature into climate scenario analysis to support informed decision-making.

- An International Actuarial Association (IAA) report, “The Climate Change Adaptation Gap: An Actuarial Perspective,” delves into issues with adapting to climate change and identifies areas where actuaries can participate.

Let’s Move the Needle

From an economic perspective, integrating nature into decision-making processes could necessitate a fundamental shift in how we assess value and risk to accurately reflect natural capital. This entails accounting for “environmental externalities,” as outlined in The Economics of Biodiversity: The Dasgupta Review, which represents the costs of exploiting ecosystem services. Achieving this requires widespread education and awareness across all levels of companies, representing an essential initial step for financial institutions.

Another significant challenge lies in the lack of valuation frameworks for natural capital, making it difficult to translate harm inflicted on nature into financial impacts and thus provide compelling financial incentives for financial institutions to restore and enhance nature.

Despite the inherent challenges and complexities, some global financial organizations already have begun assessing nature-related risks, underscoring the importance of viewing this exercise as a multiyear journey rather than waiting for perfection. Moreover, early adopters stand to minimize compliance costs, maximize synergies—particularly with climate initiatives—and potentially uncover new opportunities.

When coupled with existing or future stakeholder pressure, these factors serve as compelling reasons for the industry to, at the very least, remain informed about and begin contemplating nature-related risks and opportunities.

Statements of fact and opinions expressed herein are those of the individual authors and are not necessarily those of the Society of Actuaries or the respective authors’ employers.

SOURCES:

References:

- 1. WWF Australia. Australia’s 2019-2020 Bushfires: The Wildlife Toll. WWF, July 24, 2020 (accessed June 25, 2024). ↩

- 2. Osman, Hisham, and Sumeep Bath. Wetlands: Protecting Us From Floods and Saving Us Money. IISD, July 27, 2017 (accessed June 25, 2024). ↩

- 3. Robbins, Jim. As Water Scarcity Increases, Desalination Plants Are on the Rise. YaleEnvironment360, June 11, 2019 (accessed June 25, 2024). ↩

- 4. Organisation for Economic Cooperation and Development. Mainstreaming Biodiversity into Renewable Power Infrastructure. OECD iLibrary, January 30, 2024 (accessed June 25, 2024). ↩

Copyright © 2024 by the Society of Actuaries, Chicago, Illinois.