Actuarial Insights on IFRS 17

Two actuaries offer their perspectives on IFRS 17 and the quest for modernization, post-implementation

September 2024Photo: Getty Images/PeopleImages

The global implementation of International Financial Reporting Standard 17 (IFRS 17) has significantly transformed the financial reporting landscape for insurance contracts. This new standard aims to enhance transparency and comparability across the global insurance industry. From our perspective, the transition to IFRS 17 has not been without its challenges. Insurers have had to grapple with the complex requirements of the standard and adjust their existing systems and processes. As a result, we’ve witnessed that they have been operating in a demanding environment.

This article takes a dual perspective on the post-implementation environment of IFRS 17, highlighting issues auditors and advisors face, as well as efficiency concerns of insurance companies. Additionally, we revisit some prior predictions of post-implementation enhancements and outline measures some insurers are taking to remediate, modernize and transform their financial reporting function. Through a comprehensive examination of these aspects, we hope to shed light on the current state and future trajectory of the insurance industry in the post-IFRS 17 implementation era.

Taking a Look at the Issues

The adoption of IFRS 17, a new international financial reporting standard for insurance contracts, has posed significant challenges for the insurance industry.1 The intricacies of the standard, coupled with the need for adjustments in existing systems and processes, have created a high-pressure environment for both insurers and auditors.

Here are three thematic issues that we’ve seen in IFRS 17 financial reporting processes in our work supporting auditors and clients through IFRS 17 adoption.

Issue 1: Support for Methodologies Through Accounting and Actuarial Standards

In our experience, one of the primary difficulties during the auditing process has been the insurers’ struggle to substantiate their methodologies with a comprehensive interpretation of the standard and its thorough application to specific contract situations. For example, IFRS 17 mandates insurers to calculate insurance contract liabilities using current estimates of future cash flows, discount rates and an explicit risk adjustment for nonfinancial risk. This necessitates a profound understanding of the standard and its application to a variety of insurance products and contract terms.

We’ve experienced that numerous insurers have found it challenging to prove that their methodologies for estimating these components fully comply with IFRS 17. The intricacy of the standard’s requirements, along with the diverse range of insurance contracts, often make it difficult for insurers to apply a consistent and transparent approach. In our experience, this leads to challenges during audits, as auditors require clear and justifiable methodologies to ensure the reliability and accuracy of financial statements.

Issue 2: Delays Due to Limitations of Systems and Processes

We’ve also witnessed that the implementation of IFRS 17 has been further complicated by existing technological solutions, such as subledgers and extract, transform, load (ETL) processes. These technologies often lack the adaptability required to accommodate new methodologies and perform timely and accurate analyses of results, such as drivers of earnings and sensitivities.

Subledgers, originally designed to manage detailed transaction data, often require substantial reconfiguration to perform detailed attrition analysis of IFRS 17 results for controls and results analytics. Similarly, ETL processes, which are used for transferring and transforming data between systems, can be rigid and slow to adapt to data requirements and partial workflows involved in ad-hoc analysis. This lack of flexibility hinders insurers’ ability to promptly analyze results and make necessary adjustments, leading to delays and potential inaccuracies in financial reporting.

Issue 3: Controllership of New Processes and Systems

The introduction of new processes and systems under IFRS 17 has brought to light weaknesses in controllership within insurers. The responsibility for processes, risk management and internal audit and control is sometimes ambiguous or inadequately defined. Additionally, the coverage of internal controls may not be comprehensive enough. Effective ownership and oversight are crucial for ensuring the integrity and reliability of financial reporting, especially under a complex standard like IFRS 17.

We’ve found that it’s not uncommon for insurers to lack clearly defined responsibilities for the new processes and systems IFRS 17 introduced. This can lead to gaps in oversight and control, increasing the risk of errors and inconsistencies in financial reporting. Effective risk management and internal audit functions play a vital role in identifying and addressing these risks. However, for these functions to be effective, their roles and responsibilities must be clearly defined and communicated. This includes establishing clear lines of accountability, implementing robust risk management practices and fostering a culture of internal control and compliance. Such measures will help strengthen the integrity and reliability of financial reporting and ensure compliance with IFRS 17 requirements.

A Perspective From Insurance Companies

In 2024, the Deloitte Canada team conducted a survey2 of 25 life, health and general insurers of varying scales and operational locations. The survey focused on post-implementation considerations such as technology, processes and resourcing for IFRS 17 financial reporting.

Unlike auditors, whose focus is on accuracy, control and financial results, insurers are generally more concerned with the time and cost efficiency of the financial reporting process.

Time Efficiency: IFRS 17 Survey Results Highlights—Current State

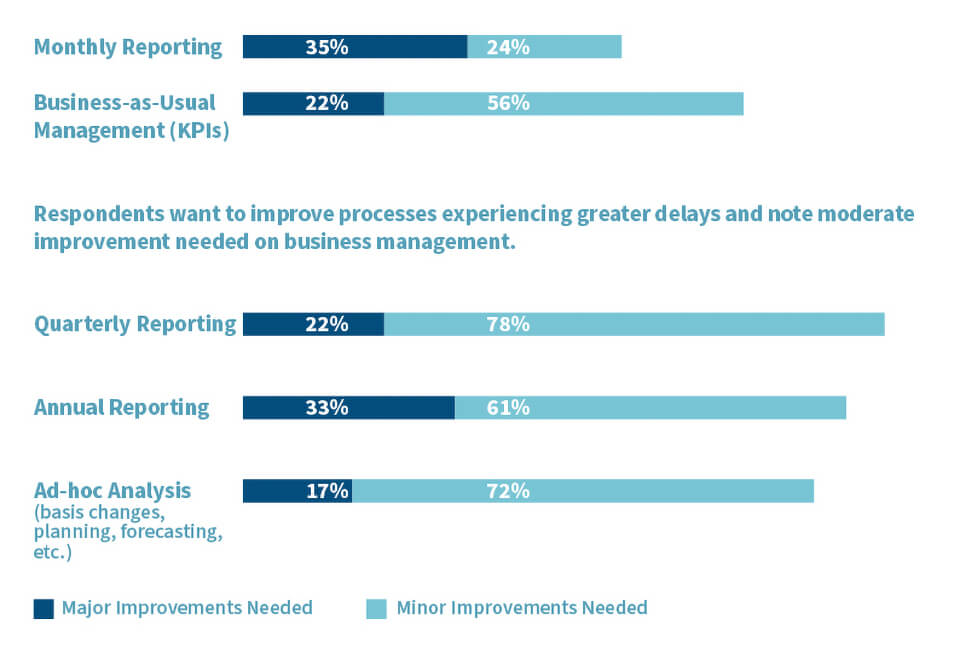

All 25 respondents of the Deloitte survey experienced different degrees of lengthening of their financial reporting and analysis processes after they adopted IFRS 17, which complicated the calculation and disclosure requirements. We asked respondents about their acceleration priorities, and they rated quarterly and annual reporting as top concerns given the extent of deceleration and the external image of these activities. Specific complex analyses, such as earning analysis and business planning, were lower in priority, as shown in Figure 1.

Figure 1: Delays and Acceleration Enhancements on Financial Reporting

Source: Deloitte Canada Insurance IFRS 17 Day 2 Survey

Due to the complexity and interdependencies involved in the measurements required of IFRS 17, insurers—particularly life and health carriers with long-duration contracts—have experienced extended timelines across most financial reporting-related processes.

Given the lengthened working day timetable resulting from the increased workload and complexity associated with IFRS 17, we can attest that insurers have faced challenges in meeting reporting deadlines and ensuring the completeness and accuracy of their financial statements. In addition, the importance of public disclosures further emphasizes the need for insurers to prioritize improvements that are more visible to both internal management and external stakeholders.

As a result, insurers are focusing their efforts on enhancing processes and systems that directly affect financial reporting and public disclosures. For example, they may invest in:

- Improving data collection, consolidation and validation processes

- Implementing robust controls and review framework

- Enhancing reporting tools to provide more transparent and comprehensive information to management and external stakeholders

By striking a balance between visible improvements and addressing the underlying complexities of IFRS 17, insurers could enhance their financial reporting processes and maintain the confidence of both internal management and external stakeholders.

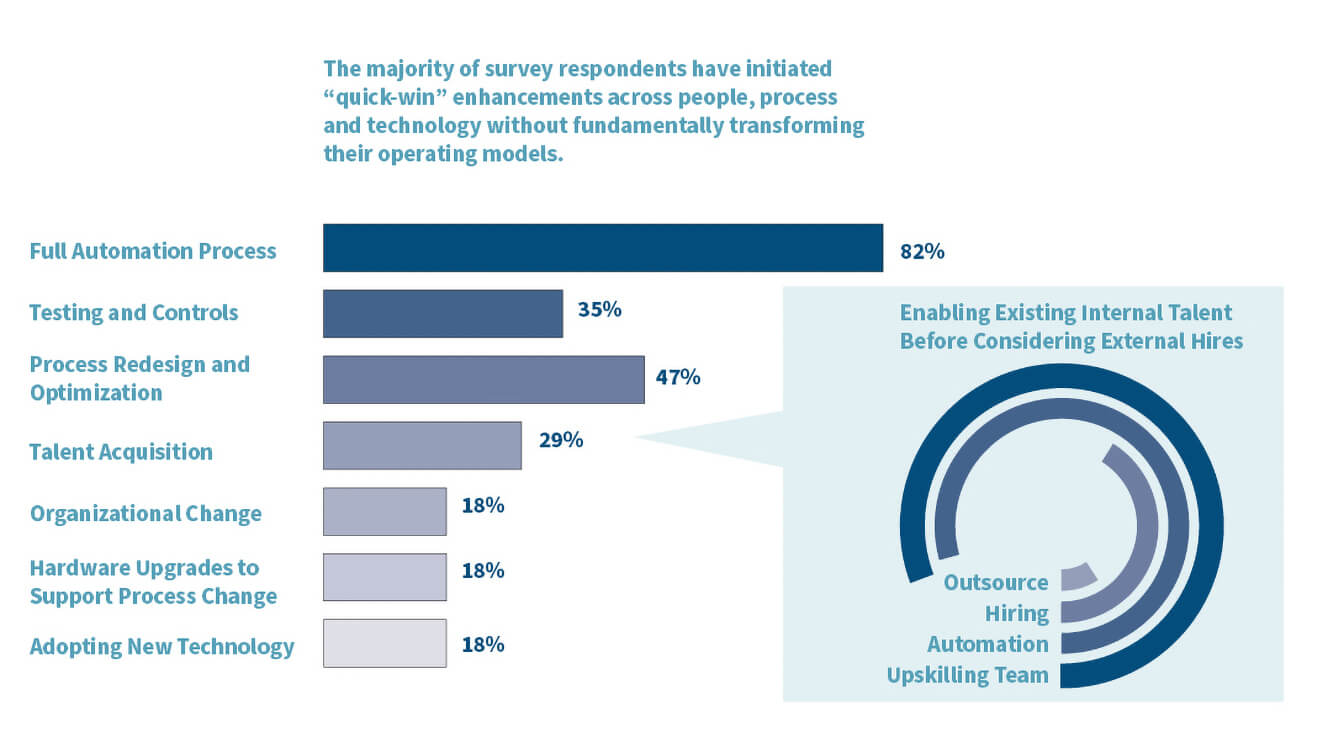

Cost Efficiency: IFRS 17 Survey Results Highlights—Enhancement Initiatives

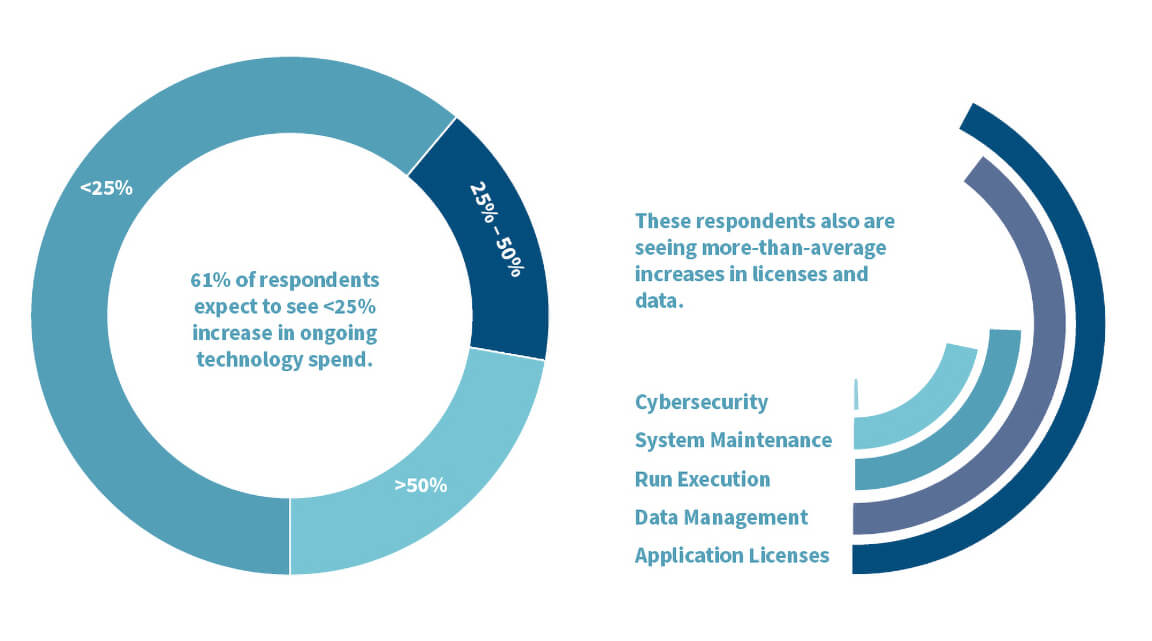

Despite the fact that the new IFRS 17 measurements resulted in increased license costs and data and computation infrastructure, our respondents are expecting the overall technology spend over time to be contained to less than 25%. So far, the enhancement initiatives focus on efficiency through automation and process streamlining. Technology changes are slightly farfetched, according to our respondents, as there are no strong contenders in the market offering obvious savings, as shown in Figure 2.

Figure 2: Cost Efficiency Enhancement of Financial Reporting Processes

Source: Deloitte Canada Insurance IFRS 17 Day 2 Survey

Technology and people, orchestrated by processes, form the foundation of financial reporting operations, we believe. The increasing granularity of data and analytical requirements necessitates a greater need for data storage and computational resources within the IT infrastructure. Some insurers have reported that their IT expenditure on financial reporting doubled in the first year of IFRS 17 reporting for the year 2023. In response, they have taken decisive measures to limit technology spending to an increase of 25%–50% from the pre-IFRS 17 era, as we heard in the IFRS 17 survey. The following are potential enhancements to achieve that goal:

- Implement a robust data management system. This helps ensure the accuracy, completeness and consistency of data and involves implementing data validation checks, data reconciliation processes and data governance frameworks.

- Improve documentation and implement strong internal controls. This ensures transparency and auditability of financial reporting processes.

- Invest in or consolidate technology. Consider technology solutions that can streamline and automate financial reporting processes. This may include implementing or consolidating reporting software, data analytics tools and cloud-based solutions. Automation can reduce manual errors, improve efficiency and provide real-time insights into financial performance.

- Provide training and education. Conduct regular training and education programs for employees involved in the financial reporting process. This will help them understand the requirements, enhance their technical skills and ensure consistent interpretation and application of IFRS 17.

Furthermore, the stabilization of methodologies, production procedures, analysis and controls also provides opportunities for automation and helps reduce the skills gap needed for IFRS 17 reporting, improving overall efficiency.

Revisiting Earlier Predictions

Our recent discussions with industry actuarial and finance leaders have revealed that their ongoing enhancement initiatives align with the themes predicted in our colleagues’ 2022 The Actuary article.3 However, there were some surprising aspects to their approach and progress, which we elaborate on here.

Remediation

What Matthew Garnier and Raj Matharu predicted in 2022: Immediately following the implementation of IFRS 17, companies would shift their attention toward addressing any shortcomings and refining their systems. The focus would be on ensuring the accuracy of financial statements and identifying crucial key performance indicators (KPIs). These KPIs would play a pivotal role in managing performance and augmenting communication with stakeholders.

What surprised us: The scale of remediation

The inaugural year of IFRS 17 implementation has yielded invaluable data and insights, enabling insurers to revisit and refine their methodologies. By benchmarking against their peers, insurers can identify best practices and areas for potential improvement. This entails analyzing both the financial and operational results obtained during the first year, comparing them with those of other insurers, and adjusting methodologies to ensure compliance, enhance results and increase accuracy.

The first wave of IFRS 17 reporting surprised both the insurance industry and the investment world, revealing significant diversity in positions, methodologies, practices and results, despite the uniformity expected from adherence to a common standard.

One of the primary objectives of IFRS 17 is to standardize the measurement of insurance operations globally. As a result, multinational insurance companies now find themselves needing to justify their IFRS 17 methods in comparison to global peers rather than solely those operating within the same market. This shift also exposes the accounting and actuarial practices each market inherited from its previous reporting standard. For example, the market-consistent measurements of insurance contracts with embedded options and guarantees exhibited a range of practices, varying from methodologies to the degree of simplification. During discussions with auditors and individuals within investment companies, we learned the investment community and financial statement users are urging companies that adopted significant simplifications to refine their practices to achieve the comparability promised by the standard.

On the other hand, life and health companies that began working on IFRS 17 between 2017 and 2020 likely could not have anticipated the current economic environment. Accounting policies and actuarial methods determined during that time may no longer be applicable in the face of rising interest rates. In recent survey result debriefs with our clients, prudent players were just starting to analyze the release of the first full annual report and revisiting their policy and methodology decisions to recalibrate for market comparability.

Lastly, the complexity of the reporting and disclosure landscape for insurance companies was underestimated. Determining the appropriate set of KPIs and the right language to communicate them has proven to be a challenging task given the diverse audiences that include management, investors, regulators, rating agencies and other users of financial reporting and disclosures.

Modernization

What Garnier and Matharu predicted in 2022: Insurers were poised to enhance efficiency through process automation and integration of the broader reporting and disclosure function. Cross-collaboration among actuarial, finance and information system teams would continue, with investments in advanced analytics and reporting tools.

What surprised us: The “divide-and-conquer” approach

To expedite and enhance cost-effectiveness in integrated reporting, insurers prioritized piecemeal and quick wins rather than making substantial changes to their software and system connections. These quick wins can come in the form of visible value generated through streamlining existing processes, augmenting data quality and bolstering collaboration among different departments.

Integrated reporting requires flawless coordination among various functions, including finance, actuarial and IT. By implementing incremental enhancements, insurers can gradually improve their reporting processes without the need for extensive system overhauls. These improvements can facilitate more prompt and precise financial reporting, which is critical for compliance and decision-making.

Following the implementation of IFRS 17, we’ve witnessed that insurers are now focused on cost rationalization during the business-as-usual phase. Maintaining data and computational infrastructure can be costly, especially considering the increased data requirements and complex calculations mandated by IFRS 17. The key areas for cost rationalization include expenses related to data and computational infrastructure and maintenance personnel costs. Figure 3 contains a brief list of some of the costs related to maintaining actuarial data and systems.

Figure 3: Costs Associated With Maintaining and Utilizing Data

| Categories | Cost Items |

| IaaS and PaaS service |

|

| Infrastructure maintenance |

|

| Database administration |

|

Management, in our experience, was surprised to realize the cumulative cost of maintaining and utilizing data. As a result, insurers are now investigating opportunities to optimize their infrastructure, such as adopting cloud-based solutions or outsourcing certain functions. Similarly, the cost associated with maintenance personnel can be reduced by automating routine tasks and investing in training to improve efficiency.

By rationalizing costs in these areas, insurers can achieve greater efficiency and cost-effectiveness in their financial reporting processes. This not only helps ensure the long-term sustainability of these processes but also contributes to the overall business profitability and competitiveness.

Transformation

What Garnier and Matharu predicted in 2022: Within two to five years following the effective date, once companies have rectified and modernized their processes, they would reassign resources to more expansive objectives. This transition would involve a shift toward the automation of manual tasks and the application of predictive modeling, machine learning and artificial intelligence (AI). In this transformed landscape, actuarial and finance functions would be pivotal in delivering actionable insights and bolstering strategies that promote sustainable business growth.

What surprised us: The race has already begun

Contrary to initial expectations of insurers solely focusing on remediating and modernizing their financial reporting processes, we discovered that companies are already implementing a variety of transformation initiatives.

Insurance companies have started leveraging the power of IFRS 17 financials to guide their strategic decisions. For example, firms are utilizing IFRS 17 metrics to improve the accuracy of their forecasts and construct more strategic business plans. Simultaneously, they are implementing operational changes in areas such as investments and asset-liability management and communicating to optimize their financial outcomes.

The complexities of actuarial modeling and multistructured data analysis are stretching the boundaries of traditional computational capabilities. In response, innovative solutions are emerging from the computer science realm to fulfill the actuarial and analytical needs of insurance companies. These advanced solutions range from NoSQL databases, which facilitate complex real-time data analysis, to GPU computing that accelerates stochastic modeling and machine learning algorithms.

Generative AI (GenAI) also is making significant strides across the commercial sector. To us, its primary role in actuarial and finance processes appears to be reducing the technical hurdles associated with complex analysis, programming, information processing and generation. Several proof-of-concepts (PoCs)4 have been carried out using GenAI prototypes, which are designed to assist with actuarial report drafting, legal contract comprehension and actuarial modeling. Leaders such as Manulife5 and Sun Life6 have even deployed some of these tools.

Conclusion

The implementation of IFRS 17 has posed significant challenges for insurers, particularly in terms of supporting methodologies, adapting technological solutions and ensuring effective controllership. However, by taking proactive steps to remediate, modernize and transform financial reporting, we believe insurers can meet these challenges and create value from the processes.

The first year of implementation provides a valuable opportunity for insurers to learn from their experiences and make necessary adjustments. By persistently refining their approaches and adopting best practices, we believe insurers could ensure compliance with IFRS 17 and achieve their financial reporting and business management objectives.

Statements of fact and opinions expressed herein are those of the individual authors and are not necessarily those of the Society of Actuaries or the respective authors’ employers.

References:

- 1. Effect Analysis of IFRS 17 Insurance Contracts. International Accounting Standards Board, 2017. ↩

- 2. Deloitte’s survey covered topics of post-implementation (“Day 2”) and included methodologies and practices, technology, process and human resources. Among the life and health respondents, three are Canada-based multinational companies, three are global insurance companies with U.S.-based operations, four are global insurance companies with significant Asia–Pacific (APAC) footprints, six are large Canadian insurers and one is a reinsurer. Survey results are not publicly published, but queries to specific areas are available upon request. ↩

- 3. Garnier, Matthew, and Raj Matharu. Beyond IFRS 17 Implementation. The Actuary, July 2022. ↩

- 4. Drabik, Laura. A Reality Check for Generative AI. Insurance Thought Leadership, February 29, 2024. ↩

- 5. Amardeil, Tania. How Manulife Is Harnessing the Power of Generative AI and LLMs. Innovating Canada. ↩

- 6. Galer, Susan. Sun Life Spotlights the Incredible Market Growth Power of Digital Modernization. SAP, July 16, 2024. ↩

Copyright © 2024 by the Society of Actuaries, Chicago, Illinois.