All in a Day’s Work

Risk mitigation from a trader’s perspective

December 2019/January 2020Photo: Getty Images

Actuaries and insurance risk managers are aware of the many risks embedded in insurance products. In addition to exogenous shocks and contractual risks tied to policyholder behavior, some products are more exposed to financial market risks. This article focuses primarily on the financial market risks and the multifaceted role a financial trader plays in risk mitigation. A trader is responsible for the life-cycle management of traded securities; serves as a bridge between insurance portfolio risk managers and the broker-dealers; aggregates and communicates relevant market, policy and regulatory information; and helps design better operational and technology-enabled interfaces for executing trades.

The financial risks in insurance contracts arise primarily from exposure to the payoffs tied to the product’s underlying assets—namely equities, sovereign bonds, corporate bonds, foreign exchange and commodities. The liability payoff structure is primarily sensitive to the historical and implied forecasts of the performance and volatility of the asset over the life of the product, and the relevant discount rate used to calculate the net present value of the product.

Financial risk management in the insurance industry begins with the mapping of underwriting cash flows of the insurance product into tradable financial indices or benchmarks. The trader then transfers the underwriting risks to the capital markets through the trading of securities tied to those indices.

A Framework for Risk Trading

A trader follows a framework of managing the tradable assets in relation to the value of liabilities originated due to the sale of an insurance product. A foundation based on asset-liability management (ALM) is fundamental to understanding the portfolio risk and decision-making process of the trader. A trader attempts to understand the assumptions used to value the products and deduce the sensitivity of the product’s value to key financial variables such as interest rates and volatility. The sensitivities of the product value to the change in the underlying asset are the first order of risks the trader strives to mitigate. This approach compels the trader to think in terms of the assets they need to buy or sell to match the needs of the liabilities. For example, a liability portfolio deficient in treasury securities should accumulate treasuries. Similarly, liabilities that have an embedded insurance against falling equity indices should sell short equity indices.

A Valuation Perspective

Valuation has always lagged behind product innovation. As insurers come up with new and innovative product designs, features and underwriting methods, the regulations and accounting methodologies are always trying to catch up—it is only natural that the regulatory bodies are not able to predict every new idea. But valuation has been evolving. …

The securities held in the asset portfolio can be levered or bought using cash. From the point of view of capital efficiency, is borrowing a security intrinsically less punitive than buying it? Leverage is also used to position for a short on an index in an asset portfolio that needs to match a liability portfolio that has guaranteed a payoff tied to the falling index value. Traders can create leverage using contracts that derive value from the performance of an underlying entity: derivatives. There are two common forms of derivatives: futures and options. Futures follow major equity indices and sovereign bonds, and options give the buyer the right to buy or sell the underlying asset at a fixed price at a future date. Traders also use over-the-counter instruments, which can be customized according to maturity, strikes and underlying assets.

In addition, the stock of hedge assets considered as part of assets may constitute either a static or dynamic hedging strategy. A static hedge is one that does not need to be rebalanced as the price or value of characteristics of the hedged item changes. This contrasts with a dynamic hedge, which requires constant rebalancing. Most hedged portfolios contain securities that will expire or mature. A static hedge used as a supplement to dynamic hedges will need to be periodically adjusted or reconstructed, usually at comparatively longer intervals than its dynamic counterpart.

A Day in the Life of a Trader

Let’s examine the operational flow underpinning the framework described. It starts with generating asset and liability risk sensitivities, and it ends with the execution of trades to close the mismatch between the two. Risk sensitivities for assets and liabilities are generated using a valuation framework based on the closing prices of a previous day, and forecasts of performance and implied volatilities of various equity, interest rate, foreign exchange and other asset classes. The valuation framework may incorporate a simulation of both financial and behavioral assumptions tied to liabilities. The risk sensitivities are made available to the risk managers and traders early in the day. The trader reconciles the available sensitivities to expected sensitivities based on market moves on financial variables the day before. This requires some understanding of higher-order sensitivities and familiarity with the liability profile. In case of inconsistencies, the trader can report them to the risk managers and the pricing and valuation actuaries. Such inconsistencies can be caught and corrected using an attribution of assets and liabilities, if required. An attribution report explains the changes in the value of assets and liabilities to the changes in the underlying benchmarks over a period of time.

Based on the mismatch between assets and liabilities, a trader will need to rebalance the portfolio by trading futures or options to close any gap within a predetermined tolerance measure. The risk tolerance metrics themselves may be based on economic value, solvency surplus, accounting surplus and liquidity buffers, and they are guided by regulatory, accounting and internal performance measures.1 Trading during widely watched economic data release dates (like change in nonfarm payrolls and retail sales) are typically volatile. The trader should focus not only on liquidity and heightened volatility, but also on the change in correlations between the different assets they need to execute. Spreads between certain assets may diverge by large measures temporarily, and the trader may need additional time and access to execution tactics, participation, spreading and liquidity- driven strategies. The trader should be cognizant that the marketable instruments used to mitigate the risks may not correspond exactly to the underlying asset risks, leaving some basis risk in the process.

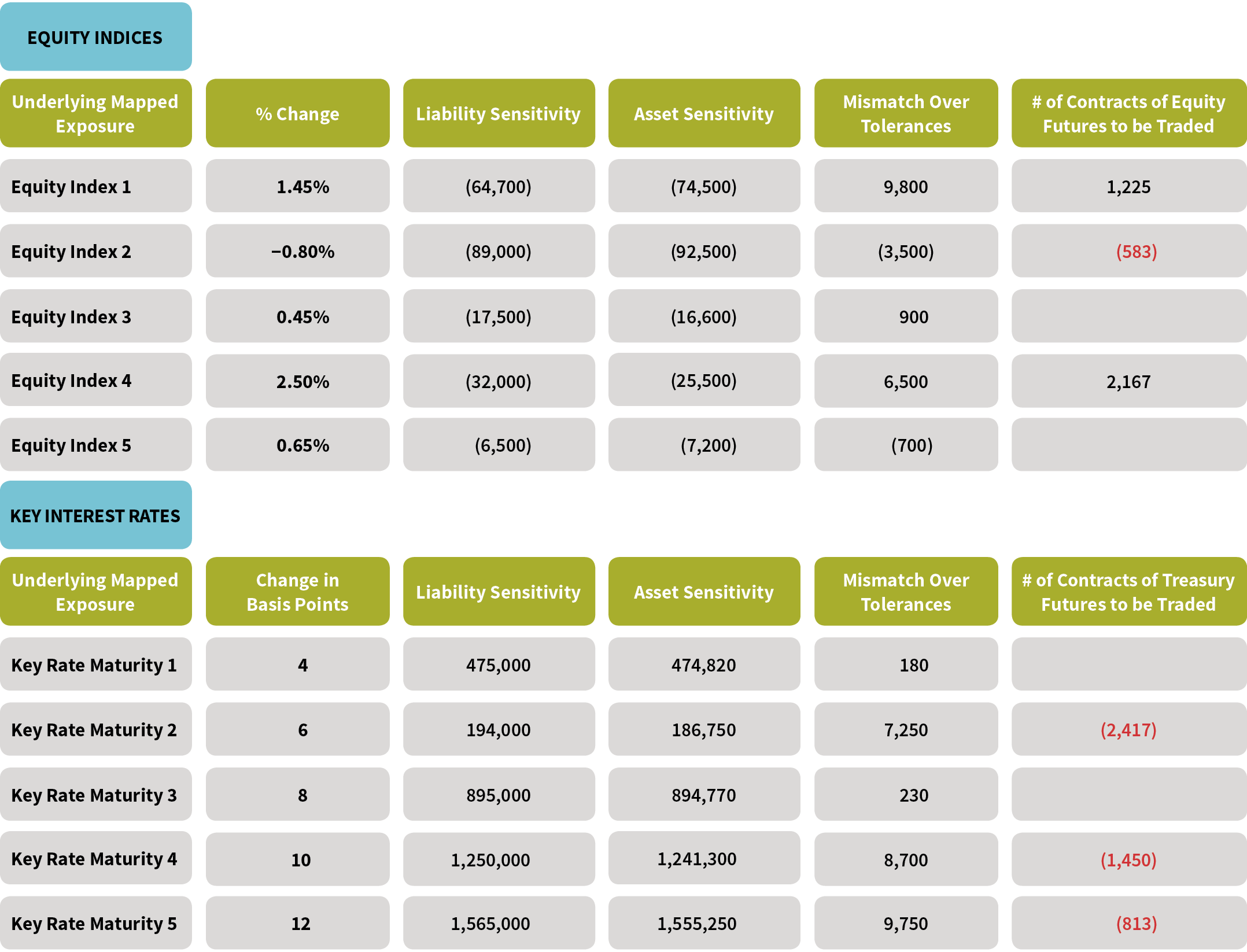

Figure 1 illustrates how the exposure to equity indices and maturities across key Treasury rates has breached the tolerances due to market moves in the underlying benchmarks. A trader will execute trades to bring the tolerance within an acceptable level. Occasionally, the trader may find that the liabilities to which asset indices are mapped exhibit an imperfect correlation due to the nature of liabilities, which subjects the portfolio to basis risk. The trader may subjectively decide to over-weigh one index vs. another in anticipation of reducing the basis risk. Historical correlations between indices and asset classes also may break down, and the trader may need to use experience to de-risk the portfolio.

Figure 1: Hypothetical Hedging Dashboard

While rebalancing a liability portfolio with embedded optionality with only linear instruments like futures, the asset-liability mismatch suffers from the lack of convexity. Such short convex portfolios need to buy the underlying assets when such assets appreciate, and vice versa. One way to compensate for a lack of optionality in an asset portfolio is to own convexity by buying options. By buying options, static hedges are sometimes added on top of a dynamic rebalancing strategy to add convexity to the asset portfolio.

Throughout the day, the trader focuses on the performance of the different financial asset markets. Following the global markets is vital and includes paying close attention to economic numbers, central bank rate decisions and member speeches, policymakers’ talks, earnings releases, bond auctions and the issue of new securities. The trader summarizes any relevant details to portfolio and risk managers, which can be escalated further to actuaries and financial officers at the firm.

Similar to rebalancing trades at the beginning of the day, the trader closes any mismatches by the end of the day by executing trades. Over a period of time, daily rebalancing trades that are needed to close the asset-liability mismatch can be cumulatively analyzed to calculate the hedge effectiveness of the program.

Simplistically, the hedge effectiveness is the extent to which changes in fair value or cash flows of the hedging instrument offset the changes in the fair value or cash flows of the hedged item. One can also calculate a quantitative measure of hedge effectiveness based on regression analysis to figure out the correlation between the hedged item and the hedging instrument. It is one of the key measures that indicates the success of a hedging program.

Finally, premiums raised from underwriting contingent claims are invested in stocks; developed and emerging market sovereign and corporate bonds; and other interest-bearing instruments, namely mortgages, securities lending, real estate and preferred stock. A trader helps portfolio managers with asset allocation, investing the premiums after reserving for potential claims. The investment income helps pay claims, commissions and administrative costs while financing operations for the insurance firm. The trader monitors new issues coming to the market, dealer inventory and available information on holdings across existing buyers to source securities. Traders help with security sourcing where portfolios may be restricted in terms of concentrations on maturities, ratings, sectors and other characteristics.

Optimizing the Trade Execution Life Cycle

A trader spends a significant amount of time studying market microstructure to understand liquidity and market participant behavior. They also study research on pre- and post-trade analysis to improve execution strategies.

Pre-trade analysis separates trade orders based on the time of day or month, order size, underlying assets, sectors and portfolios. Pre-trade transaction costs analysis (TCA) provides portfolio managers with estimates of trade costs and market impact based on extensive study of historical trade execution. It evaluates all pertinent trade execution methods and highlights the strategy that is most consistent with a manager’s risk preferences. The trader considers different algorithms based on tactics, participation, schedule, spreading, liquidity, execution rate and crossing networks to reduce execution cost and slippage.

Post-trade TCA helps firms analyze trader performance across numerous metrics. Trade execution quality can be assessed by comparing actual executed prices to selected benchmark prices. A range of benchmarks can be considered, including volume-weighted average price, opportunity cost, performance and open/close/previous close prices.

Such feedback can help align a trader’s execution strategies to the objectives of the fundamental and quantitative portfolios and managers. Traders continually seek to improve execution strategies, align behavioral profiles with implementation strategies, and optimize trading strategies driven by portfolio and client constraints.

The trader is also accountable for support with supplementary functions related to post-trade settlement issues, choosing execution and clearing venues, and maintaining regulatory upkeep such as LIBOR to SOFR transition. A trader provides valuable input during negotiations and signing of credit support annexes, and choosing the types of collateral that can be posted to preserve capital and minimize counterparty risk. A trader helps choose an optimal instrument to gain exposure to an underlying asset based on initial and variation margin, eligible collateral, easy-to-access venues, clearinghouse requirements, liquidity, funding costs and dealer balance sheet constraints. For example, to gain exposure to a given underlying asset, a trader can use futures, exchange-traded funds (ETFs), cleared and bilateral swaps, or even options based on some of the criteria cited. The choice of the trading instrument is crucial to optimize the risk capital used for the hedging program.

Integrating Risk, Actuarial and Finance to Develop ALM for Future Products

In the future, there is an expectation that the regulatory framework governing insurance companies converges to the broader financial sector. This should call for consistency between statutory and economic risks. Broader financial market integration also necessitates that diverse regulations be harmonized across jurisdictions.

In the same vein, ALM based on the different metrics discussed should converge toward a more market- consistent measure based on economic risks. Robust modeling of liability profile and policyholder behavior, lapses, surrenders, and income utilization using big data and predictive analytics can help with market-consistent pricing, reserving and risk management of product blocks. Business groups like finance, risk and actuarial that traditionally have worked in silos will need to share a common set of core data, underlying infrastructure and assumptions.

Insurance product managers and actuaries developing new products will seek input from ALM groups and traders to create products that can be hedged readily using liquid instruments. Traders will play a significant role in providing market-consistent input data that can facilitate the valuation and pricing of new product launches. Feedback from traders is important when structuring products that can be readily hedged and features that can be easily priced. Another vital consideration is the amount of effort required to unwind a contract with a counterparty in case they are surrendered—there should be minimal effort involved. Aligning the objectives of product managers and risk managers will be key in designing a new generation of products.

References:

- 1. Schneider, Richard. 2018. The Great Juggling Act. The Actuary, May. ↩

Copyright © 2019 by the Society of Actuaries, Chicago, Illinois.