ALM in the Taiwan Insurance Market

Actuarial insights on a unified approach to asset-liability management under IFRS 17

October 2024Photo: Getty Images/tampatra

The insurance industry in Taiwan has experienced a flurry of regulatory changes in recent years, such as the transition in valuation rules from Actuarial Guideline 43 (AG43) to Valuation Manual 21 (VM21) for variable annuity products. There also have been newly revised interest rate declaration formulas for interest-sensitive plans, impact studies for Insurance Capital Standard (ICS) and the implementation of International Financial Reporting Standard 17 (IFRS 17).

Amid these changes, asset-liability management (ALM) has emerged for insurers looking to understand and mitigate financial impacts while transitioning to market-consistent international standards. These changes not only represent regulatory challenges for insurers but also offer an opportunity to optimize capital, if managed properly.

In response to these changes, several insurers in Taiwan have engaged me to assist in enhancing their asset models. Surprisingly, in my observation, a few insurers in the region either lack a robust asset model or rely on simplistic deterministic approaches, overlooking critical asset-liability interactions.

Traditionally, the segregation of ALM between the investment and actuarial departments has hindered optimal collaboration. Thus, this article seeks to address the fundamental shift toward a unified ALM approach across processes, systems and models to facilitate seamless management of assets and liabilities in today’s dynamic market environment, thereby fostering sustainable business growth.

ALM: The Process

ALM is the process of managing the use of assets and cash flows to reduce the insurer’s risk of loss from not paying a liability on time. While complete elimination of mismatches is not always feasible, prudent management entails earning returns to offset higher capital requirements associated with such mismatches. Since both assets and liabilities are evaluated in fair value under the new IFRS 17 standards, monitoring the impact of interest rate changes provides insightful information in ALM. Well-managed assets and liabilities reduce potential loss and enhance business profits.

In my experience, the investment department made decisions based on target return and expected average duration provided by the actuarial department. The asset class and its impact on risk requirements seldomly were considered. Going forward, more collaboration between the investment and actuarial departments is expected, as well as with the risk management, finance and IT departments. During product pricing, actuaries could test the asset cash flows with liability profile, taking the risk capital, financial reports and potential supports from IT into consideration.

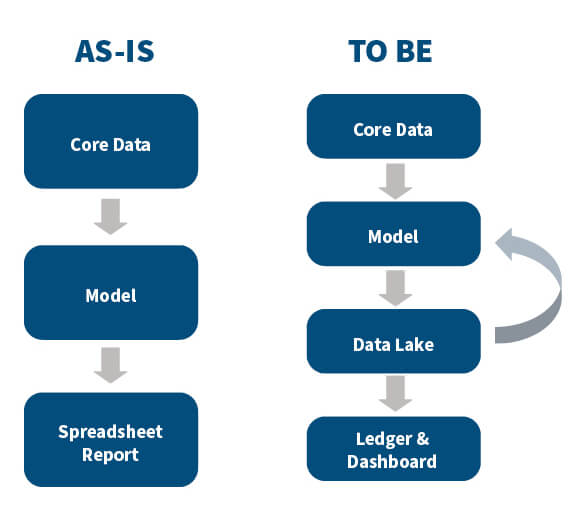

In addition, with advancements in financial reporting software, the reporting process could transform from being heavily dependent on manual spreadsheet report work to having more interactions and feedback loops between the model and data lake. The numerical output will be transformed by ledger and dashboard software in presentations, which business decision makers can more easily understand.

Figure 1: Data Flow of Financial Reporting

ALM: The System

With the implementation of IFRS 17, the process for actuarial reporting and analysis has shifted to a modernized solution through systems. The new regulatory changes require more granular data and more detailed calculations that must be processed by policy issue cohort and other means. New attributes such as loss components and amortization of contractual service margin and risk adjustment also are required in the new regime. Manually summarizing or analyzing the data is no longer an efficient way of reporting—for most. Embracing a more sophisticated system may offer advantages across various dimensions, including data management, enhanced data quality, comprehensive reporting and analysis, and process automation.

Data Management and Enhanced Data Quality

ALM systems can centralize data from various sources, including policyholder information, financial data, market data and economic indicators. By consolidating data into a single repository, insurers can streamline data management and reporting processes, ensuring data consistency and accuracy. Implementing a robust validation process within the systems can effectively detect errors in the data, thereby ensuring high-quality data. While many insurance companies may have established such processes on the liability side, it’s equally crucial to extend these measures to the asset side.

When receiving asset data from investment firms, conducting thorough validations becomes imperative to verify the accuracy of the information provided to ensure compliance with regulatory standards.

Comprehensive Reporting and Analysis

With all data and information stored in a single repository, insurance companies can enhance their capacity for granular analysis of their assets and liabilities significantly by aggregating or disaggregating data across all relevant dimensions to gain deeper insight into the underlying drivers of financial performance and risk. Moreover, visualization tools such as Microsoft Power BI can be implemented to elevate result presentation and facilitate advanced analysis aided by AI capabilities.

This empowers actuaries with real-time reporting functionalities and enables predictive analytics tasks, including estimating risk and forecasting future required capital, thereby fostering proactive decision-making and strategic planning initiatives.

Process Automation

ALM systems can automate the process from data collection to reporting. Automation can help reduce manual process risk, enabling actuaries to focus on more strategic analysis and business decisions. By defining workflows, rules and triggers within the system, insurers can streamline operational processes, improve efficiency and reduce operational costs.

ALM: The Model

Underpinning the ALM framework is the actuarial cash flow model, which has assumed heightened importance under new accounting and solvency standards. The dynamic interactions between assets and liabilities can be considered within an ALM framework for insurers to gain better insights from the interest rate changes. Centralizing the model allows the same calculation logic to be applied for all reporting bases and thereby guarantees consistency in results and better model performance. A single model that is shared among different actuarial reporting teams (e.g., IFRS 17, embedded value [EV], capital management, risk management) and utilizes the same subset of formulas and cash flows also provides better transparency by clearly showing the discrepancies in calculation methodologies and assumptions applied in the model. It streamlines the process and avoids different views of the results.

Additionally, using a single model can help a company save time and costs associated with model maintenance and respond promptly to changing requirements. Another advantage a centralized model can offer is detailed audit trails that improve accountability and traceability when making model changes. By implementing strong model governance and control processes, organizations can clearly define roles and responsibilities across actuarial functions, possibly reducing the risk of model errors and ensuring regulatory compliance with more confidence.

Supporting the ALM Process and Moving It Forward

Actuaries could take on the responsibility of communicating the importance of ALM and the benefits of the transformation outweighing any additional costs in the short term to boards of directors and senior management. Communication is more important than ever.

With the substantial volume of calculations mandated for regulatory and ALM reporting, establishing a dedicated team for model management could be key to ensuring the ongoing refinement and accuracy of the model. Requests for model modifications may arise due to factors such as new product introductions, repricing initiatives, adjustments to assumptions, regulatory mandates and internal policy changes.

To maintain robust modeling practices, I believe it’s essential to institute a comprehensive modeling process guideline. This guideline could encompass thorough validations and reconciliations throughout the modeling process. Additionally, comprehensive documentation could provide clarity and transparency for all stakeholders, including modelers, users, managers, reviewers and external auditors.

Based on my observations of the Taiwan market, the current marketplace is already experiencing a notable shortage of modeling actuaries, presenting a formidable challenge for insurance companies striving to maintain a dedicated model team. In light of this scarcity, exploring alternative solutions becomes feasible and pragmatic. Options such as shared services, managed services, outsourcing and co-sourcing offer pathways for companies to bolster their modeling capabilities while navigating the talent shortage. By strategically leveraging these alternatives, insurers could effectively address staffing challenges and continue to develop and refine their modeling functions.

Conclusion

To achieve excellence in ALM, a concerted effort and alignment across processes, systems and models is likely required. The current era of rapid modernization and a shifting regulatory environment require insurers to respond to market changes faster than ever. Adopting a new operating model for ALM, which includes processes, data management systems and models, could be crucial in saving resources and time on number-crunching to allow actuaries to focus more on results analysis. Gaining budgetary support, recruiting personnel with the right technical skills and providing staff with the latest training will likely be key in the present and near future.

Statements of fact and opinions expressed herein are those of the individual authors and are not necessarily those of the Society of Actuaries or the respective authors’ employers.

Copyright © 2024 by the Society of Actuaries, Chicago, Illinois.