Assumption Governance

A spoonful of strategy helps the governance go down

January 2021Photo: iStock.com/Siphotography

Assumptions garner lots of attention from many interested stakeholders, in part because they often involve a significant amount of “actuarial judgment,” a phrase that may invoke a sense of mystery to those who aren’t familiar with it.

Actuaries rely on assumptions for pricing, forecasting, reserving and modeling. The better the assumptions, the better the model. Assumptions inform our expectations for financial results and help us understand the variance when actual results emerge differently. Although often the most subjective component, assumptions can be the most impactful aspect of an actuarial model. Simply, we cannot do our jobs without them.

Regulatory changes, emerging technology and pressure on profitability from a sustained low interest rate environment are further increasing the impact of assumptions. Modern actuarial models—based more on first principles than prescription—rely heavily on a company’s own expectations for the future, which can be challenging to support with imperfect data. Because assumptions have such broad applications, significant impacts and reliance on judgment, it is crucial to set them in a governed manner. Efforts to develop, approve and monitor assumptions can be overwhelming, especially when the focus is to comply with numerous regulatory requirements.

Investment in an optimized assumption governance framework that is aligned to business needs helps to create a culture where governance enhances the actuary’s work and is not simply a “check the box” exercise. When embedded in a company’s strategic objectives, a streamlined assumption development process can better focus resources on the most impactful areas and ultimately create an environment where actuaries gain deeper insights into their businesses.

The Problem With Compliance

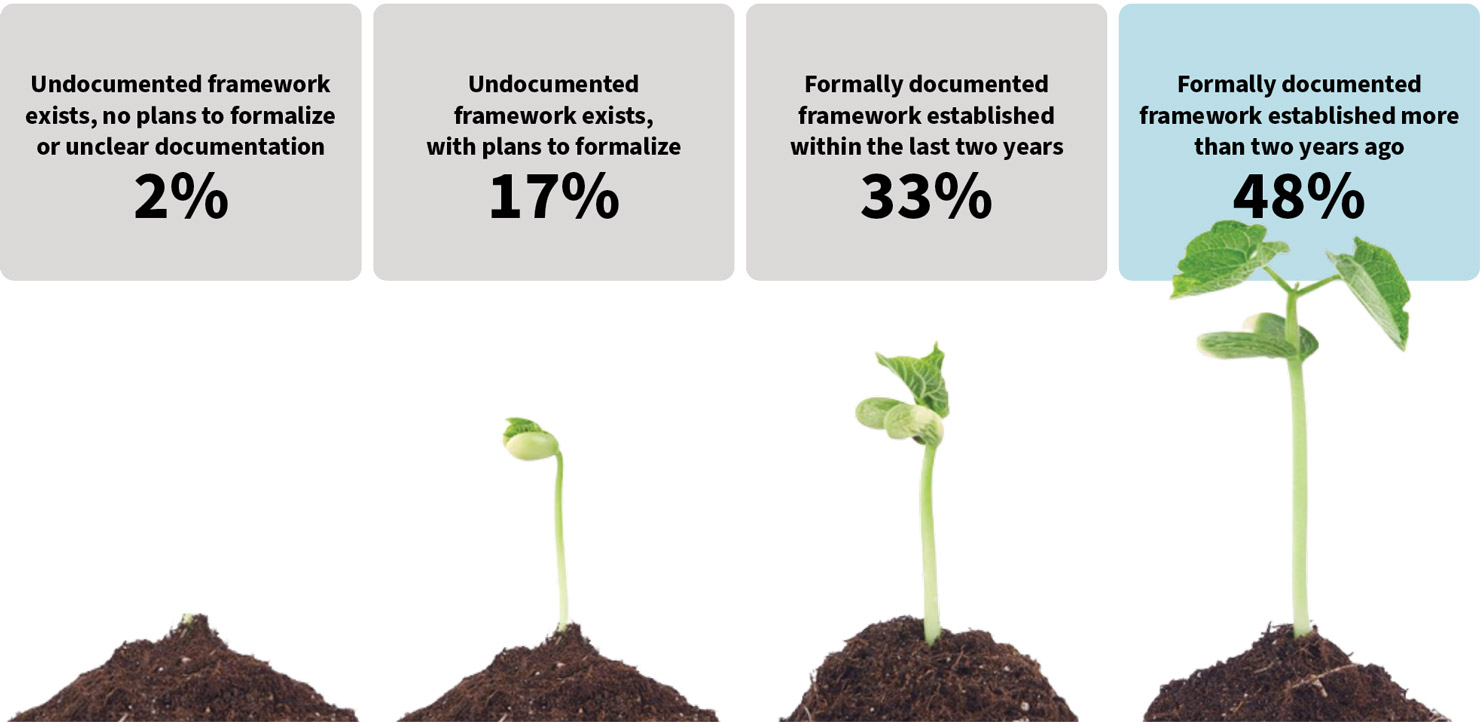

Over the last decade, many insurance companies formalized their assumption governance processes and policies. According to a recent Oliver Wyman industry survey,1 more than 80 percent of participants have a formally documented assumption governance framework, with one-third of those established within the last two years and nearly half established before that (see Figure 1).

Figure 1: Current State of Assumption Governance

Most companies already have a formalized framework or are planning to cultivate one.

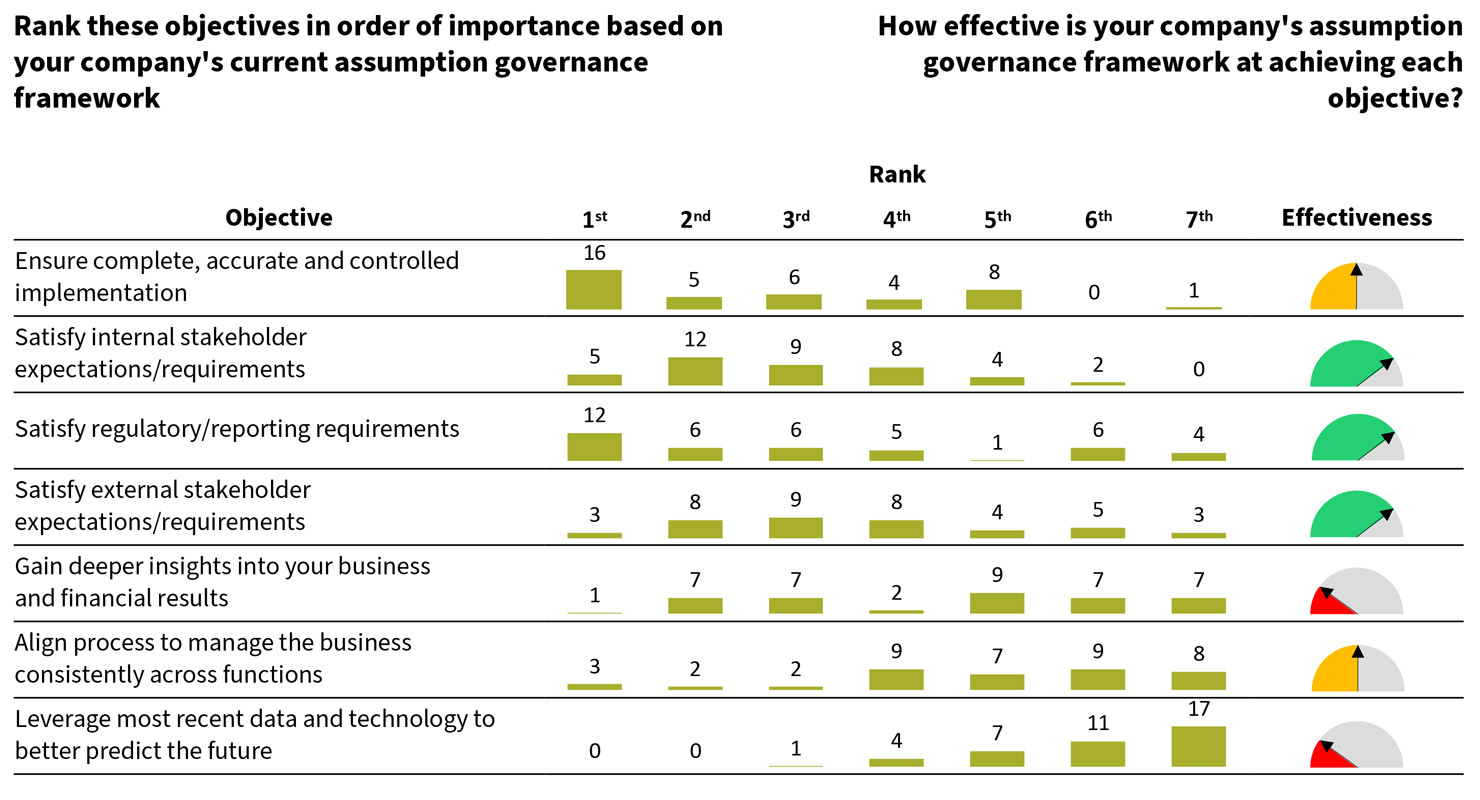

The survey also sheds light on the main objectives of these frameworks. As seen in Figure 2, the top responses are “ensure controlled implementation of assumptions into models” and “satisfy stakeholder expectations” (e.g., audit or regulatory requirements, management directives). Other objectives—gaining deeper business insights, achieving consistency across functions and improving the precision of models—were ranked lower. Unsurprisingly, the objectives that get deprioritized score lower in effectiveness.

Figure 2: Objectives and Effectiveness of Assumption Governance

The majority of participants prioritize accuracy and stakeholder requirements over improved management of the business; no more than six participants rate themselves as “extremely effective” for any single objective. When management of the business is prioritized as an objective and done effectively, stakeholder requirements will fall into place.

Insurance companies seem to approach assumption governance as a compliance exercise rather than a strategic initiative. While it is critical to comply with regulations and satisfy stakeholders, the effort that is spent on assumptions should be driven by their usefulness in solving actuarial problems and managing business, not by a mandate from above. Valuing compliance higher than better predicting the future only ensures the accurate implementation of a suboptimal assumption, which is clearly not an ideal outcome.

A compliance-focused approach is not sustainable in today’s actuarial landscape. The number of requirements and stakeholders that must be satisfied is growing. Figures 3 and 4 summarize recent accounting changes and new standards of practice that give more responsibility to actuaries and identify specific governance requirements.

Figure 3: Regulatory Impacts on Assumption Governance

| Regulation | Assumptions Impact | Governance Requirements |

| Principle-based reserving (PBR) | They should be based on company experience instead of prescribed assumptions. |

Valuation Manual-G assigns responsibility to the actuary to verify that assumptions reflect the requirements of the Valuation Manual and are prudent estimates. Valuation Manual-31 itemizes a wide range of assumption disclosures that must be covered in the annual PBR report. |

| Long duration targeted improvements (LDTI) | For traditional and limited-pay business, use current best estimates instead of assumptions set and locked in at issue. | Assumptions must be reviewed at least annually, and the results of such review must be justified to auditors. |

| International Financial Reporting Standard 17 (IFRS 17) | All insurance contracts must be measured using current estimate assumptions. | Assumptions are to be updated at each reporting date, and the actuary must demonstrate how the assumptions are consistent with current market information. |

Figure 4: ASOP Impacts on Assumption Governance

| Actuarial Standard of Practice 56—Modeling | Setting Assumptions Standard of Practice (Exposure Draft) |

| Provides guidance about information to be used in setting assumptions, consideration of a range of assumptions, consistency of assumptions and reasonability of assumptions in aggregate | Provides guidance and considerations for reviewing the reasonableness of assumptions |

| Compels the actuary to use reasonable governance and controls to mitigate model risk | Discusses how the actuary should consider changes in conditions that may impact the appropriateness of assumptions |

| Identifies several topics that should be disclosed in an actuarial communication about assumptions |

Sufficient resources are difficult to secure when the goal is to “check a box.” With a growing number of boxes, even the largest of actuarial departments will struggle. Nearly three-quarters of the Oliver Wyman survey participants identified shortage of resources as an obstacle to a fully effective governance framework.

Even with a fully staffed team, a compliance-based assumption governance framework will fall short of its potential. Per the assumption survey, existing frameworks are ineffective at maximizing insights (refer back to Figure 2), representing a missed opportunity when compliance is prioritized over strategy. When the primary goal is to satisfy a laundry list of requirements, the bigger picture will be missed—or at least not fully appreciated. With a tight timeline, already scarce resources have few opportunities to think strategically, so you may meet your regulatory requirements but miss out on valuable business insights. Even worse, your employees could be overworked and disengaged.

Changing the Governance Narrative

In 2014, The Actuary published a book review2 of The Checklist Manifesto: How to Get Things Right by Atul Gawande. The book discusses how checklists, when properly implemented, have been a powerful tool for improving outcomes in the medical profession. Gawande provides examples of success stories from other professions, and The Actuary’s review, written by Jay M. Jaffe, discusses a few examples of checklists in the actuarial field. The book has had a broad impact on the business world because the lessons can be generalized to any framework that identifies requisite steps to achieve a goal.

One particularly analogous quote from Gawande’s book echoes the frustration that actuaries currently experience with assumption governance: “We doctors remain a long way from actually embracing the idea. The checklist has arrived in our operating rooms mostly from the outside in and from the top down. It has come from finger-wagging health officials, who are regarded by surgeons as more or less the enemy, or from jug-eared hospital safety officers, who are about as beloved as the playground safety patrol.”

Replace “doctors” with “actuaries,” “checklist” with “governance,” “health officials” with “regulators” and “hospital safety officers” with “internal audit,” and the quote summarizes the current state of assumption governance in the actuarial field. Ticking boxes that someone else created does not stir up warm and fuzzy feelings.

Borrowing again from the medical profession, a study published in the Annals of Medicine shows how changing the narrative of a checklist can lead to a better outcome. In Canada, the surgical checklist was deployed by making it a law. Hospitals had to sign off that they performed the checklist to be compliant. These hospitals saw a 0 percent improvement in surgical death rates. In contrast, South Carolina’s implementation of the same checklist was voluntary and had a lengthy implementation process to ensure employees at the hospital understood the value of the checklist. They were encouraged to enhance it and make it their own based on their specific needs. These hospitals saw a 22 percent reduction in surgical deaths, or the equivalent of eliminating all car crash deaths in that same population.3

Both groups of surgeons used a similar process but had markedly different results. Where the motivation was homegrown and presented as a strategic initiative, the results were tremendous. Similarly, actuaries need to approach governance with strategic objectives in mind to foster engagement and have long-term success with managing assumptions. The overarching goal should be to develop the best assumptions possible. Period. The beneficial byproducts noted in Figure 5 naturally follow.

Figure 5: Byproducts of Strategic Governance

Optimizing Governance for Sustained Success

Following a strategic approach, effective governance sets a culture of discipline, not myriad procedures. It is no small task to properly frame or reframe an assumption governance framework, but companies have overcome the challenges with a variety of strategies. Three concepts are perhaps the most fundamental solutions to consider for sustainable assumption governance:

- Guardrails

- Risk-based framework and monitoring system

- Communication

Guardrails

Governance is incomplete without a foundation of policies, procedures and standards. However, as illustrated through examples from the medical profession, strict and perfunctory enforcement may not lead to improved outcomes. The most elaborate checklist cannot replace expert judgment. Governance policies are more effective when they encourage a disciplined culture and empower actuaries to maximize their impact on assumption-setting

To reinvent assumption governance, policies can be framed as “guardrails” along a path and not the singular path itself, a concept employed by the Actuarial Standards of Practice (ASOPs), which provide guidance without prescribing specific methods. A section about the consistency of assumptions in the new cross-industry ASOP 56 is a good example of providing guardrails that prioritize culture over inflexible procedures.

ASOP 56 requires that consistency in assumptions across models be considered and explained rather than mandating that all models have consistent assumptions—a subtle, yet important, nuance. The behavior, not the outcome, is tackled. In encouraging the right behaviors, the outcomes follow. As a result, actuaries will think deeply about the consistency of assumptions, which will result in the desired outcome of consistency. Left with the opportunity for appropriate instances of inconsistency, the actuary maintains the prerogative to make expert decisions.

Guardrails can be applied to commonly used aspects of assumption development, such as credibility standards or the number of years of data included in experience studies. There are several benefits to developing policies that one can reference “off the shelf” with the ability to deviate, if justified. If the policy is a five-year look-back period for experience studies, then no further explanation is needed when the actuary uses that standard, resulting in more consistency, less documentation of commonly used approaches and easier-to-explain decisions. Additional effort is required only when deviation from the standard needs to be justified. In turn, actuaries can spend more time on complicated cases where their expertise is more valuable.

Guardrails reduce routine work in normal circumstances and allow actuaries to be the experts in setting the best assumption, which is the ultimate goal.

Risk-based Framework and Monitoring System

For early adopters of strong assumption governance frameworks, a common challenge is “too much work in too short a time frame.” Most companies review and set assumptions on an annual and predefined cycle. Naturally, they encounter time and resource constraints when they attempt to “boil the ocean” every year. Companies with an ad-hoc schedule or judgment-based approach struggle to explain why certain assumptions received more attention than others.

A risk-based framework coupled with a monitoring system solves both problems and is the single biggest opportunity to alleviate resource strain during the assumption-setting season. A risk-based approach evaluates each assumption on quantitative and qualitative measures to define the risk level. Assumptions with the largest financial impact and the highest degree of complexity naturally rise to the top of the list, whereas more stable, less impactful assumptions fall in priority.

The most impactful assumptions undergo “enhanced” review procedures, receiving additional scrutiny commensurate with their business impact. Lower-risk assumptions receive a higher-level “standard” review, with a deep dive taking place a minimum of every three to five years. If the standard review uncovers new information, such as new or improved data or a change in materiality, the assumption may be promoted to an enhanced review.

Monitoring bridges gaps from one review cycle to the next. Monitoring activities are usually a subset of full assumption review procedures—such as refreshing a dynamic validation or updating your credibility metric—and are performed more frequently than full reviews. If monitoring activities reveal a potential material deviation, an off-cycle assumption change may be considered. This is critical for both higher- and lower-risk assumptions to ensure no surprises occur during the next full review, whether it’s in one quarter or five years. Moreover, if monitoring is properly documented and reviewed, stakeholders will be comfortable with a risk-based review schedule.

With assumption monitoring as a first line of defense for a risk-based framework, companies can better utilize their valuable resources for the highest impact.

Communication

Increased communication is essential to well-functioning governance and seemingly simple to implement (though often the most difficult). As data, experience studies, models and results become more complicated, communication among relevant experts is increasingly critical. A linear path of communication, with stepwise handoffs from one party to the next, is no longer effective; feedback loops and collaboration are required.

Legendary Chef Dan Barber said, “You are not what you eat; you are what you eat eats.” Similarly, actuarial modelers need to not only know the assumptions, but also how they were developed, including the data fed into the experience studies. Likewise, data and assumption owners need to better understand models to formulate the best assumptions that are fit for purpose.

Better conduits for experts to communicate throughout the process should be put in place. A simple addition of biweekly working groups during the assumption-setting season can bring together the right experts in data, assumptions, product design, valuation, tax and modeling to ensure all complexity and nuance are covered. Reframing the governance process as a strategic objective is invaluable in ensuring participants are engaged and do not skip meetings for seemingly higher priorities.

Beyond these three fundamental changes, companies can further refine their assumption governance by applying the suggested practices outlined in Figure 6.

Figure 6: Success Path for Overcoming Challenges

In Conclusion: Govern With a Strategic Focus

Although compliance is an important outcome of a well-functioning assumption governance process, it should not be the stated objective. As observed in other industries where highly trained professionals solve complex problems, the desired outcome rarely is achieved when compliance is the sole objective. Governance needs to be deeply embedded in an organization’s culture to encourage discipline. For true buy-in, governance must seek to achieve a strategic goal—set the best assumptions possible. A thoughtful approach that takes culture into account is the only way to achieve this goal, as it lets compliance objectives fall into place naturally.

The views or opinions expressed in this article are those of the authors and do not necessarily reflect the official policy or position of Oliver Wyman.

References:

- 1. Smith, Katie K., and Christopher Halloran. Assumption-Setting and Governance Survey. Oliver Wyman, 2020. ↩

- 2. Jaffe, Jay M. Actuarial Checklists. The Actuary, April/May 2014. ↩

- 3. Boyle, Tara, Shankar Vedantam, and Renee Klahr. You 2.0: Check Yourself. The Hidden Brain, NPR, August 27, 2018. ↩

Copyright © 2021 by the Society of Actuaries, Chicago, Illinois.