Achieving global climate targets requires industries to adopt a range of new technologies and processes that accelerate their decarbonization. As physical climate risks intensify,1 the need to accelerate the widescale deployment of new climate tech for industrial decarbonization at scale is becoming more acute. Globally, substantial efforts are underway to enable and expedite the decarbonization of heavy industries that are essential for economic development, such as steel, aluminum, cement, shipping, aviation and trucking, which contribute to more than 30% of global carbon emissions.

This article builds on a 2022 article from The Actuary, “Decarbonizing Our Economy,” and the 2024 Climate Tech and Insurance research from The Geneva Association. It also provides innovative suggestions on leveraging insurance and reinsurance companies’ expertise in risk engineering and underwriting to frame and develop risk mitigation strategies for untested risks, unlock capital and potentially expedite market readiness for widescale deployment.

Climate Tech: Deployment Challenges

Though significant progress has been made in developing innovative climate technologies, such as green hydrogen, long-duration energy storage (LDES), industrial geothermal and carbon management (point source or direct air capture, utilization and storage), most remain in the pre-commercialization stages. Among the reasons for this are huge funding gaps, challenges with scaling and market readiness, and scarcity of data on the new, untested risks they pose.

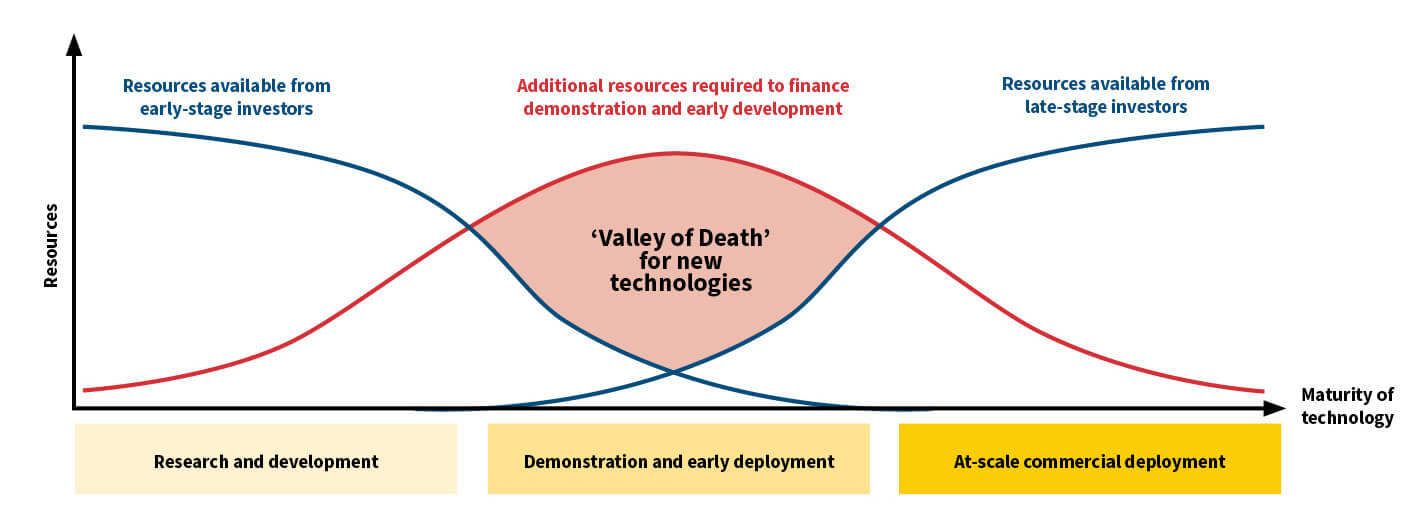

Climate tech innovation, demonstration and market readiness for at-scale commercial deployment would require trillions of dollars annually in transition funding. Even financing of first pilot projects is capital intensive, and many “potentially viable” technologies “die” and never make it to the market. This phenomenon is known as the “valley of death” (see Figure 1), which signifies the gap between availability of financing in the initial development of a technology and its commercialization. Closing this financing gap will require massive amounts of private capital; relying solely on public capital will not be sufficient.

Figure 1: Valley of Death: Major Investment Gap in Commercialization Pathway of Emerging Climate Tech

Source: The Geneva Association

Toward a Holistic Approach to Managing Risks From Early to Commercial Deployment

Demonstrating and deploying emerging technologies come with many challenges and untested risks. They will necessitate new ways of doing business and changes to traditional commercialization pathways. Historically, the Technology Readiness Level (TRL) Framework has been utilized to assess a technology’s maturity from research and development in the lab to at-scale commercial deployment. However, TRL does not capture many risks that hinder market readiness.2,3 Strong cross-sectoral collaboration can help frame and assess risks and develop risk management frameworks during different periods.

Traditionally, insurance and reinsurance companies engage when the technology has been demonstrated, risks are known and data is available to assess and price risks—generally, at the latest stages in the TRL Framework (see Figure 2 for an illustration). Perspectives from climate tech stakeholders and a survey of C-level executives in insurance have indicated that engaging insurance and reinsurance companies in the early phases of climate tech projects—from the demonstration and early deployment stages (TRL 6)—through the provision of risk engineering services could be beneficial for all stakeholders.4 However, a lack of mechanisms to involve insurers and reinsurers directly with climate tech developers from early stages, a limited number of projects and no established path to profitability are among the key roadblocks to insurers’ and reinsurers’ participation in the pre-commercialization stages.

Figure 2: Traditional Technology Readiness Level (TRL) Framework and Insurance and Reinsurance Companies’ Engagement

| Technology Stages | Technology Readiness Level (TRL) | |

|---|---|---|

| At-scale Commercial Deployment (Traditionally, reinsurers are engaged at this stage) |

9 | Wide-scale commercial deployment |

| 8 | Early commercial deployment | |

| Demonstration and Early Deployment | 7 | Complete system demonstration in an operational environment |

| 6 | Early field demonstration and system refinements completed (Early engagement of insurance companies’ risk engineering teams from TRL 6 could be mutually beneficial for all stakeholders) |

|

| 5 | Early system validation demonstrated in a laboratory or limited field application | |

| 4 | Subsystem or component validation in a laboratory environment to simulate service conditions | |

| Research and Development | 3 | Proof-of-concept validation |

| 2 | Technology concepts and/or application formulated | |

| 1 | Exploratory research transitioning basic science into laboratory applications | |

Source: NASA information, with modifications by The Geneva Association

Climate Tech: Changing Risk Landscape

Over the last few years, seven critical developments are affecting the emerging climate tech risk landscape, paving the way for expediting the commercialization and deployment of these technologies:5

- The Adoption Readiness Level (ARL)6 Framework, introduced in 2022 by the U.S. Department of Energy, has been designed to address factors that hinder market readiness of climate technologies and complements the TRL framework. ARL separates 17 risk types into four categories: value proposition, market acceptance, resource maturity and license to operate, which need to be addressed from pre-commercialization stages to pave the way for at-scale commercial deployment.

- Transformative public policy and new legislation have provided significant government subsidies since 2022. For example, in the United States, the Inflation Reduction Act and the bipartisan Infrastructure Act have availed nearly US$1 trillion in government subsidies.

- Growing concerns around energy insecurity have prompted new national critical materials strategies aimed at building a competitive advantage in material sourcing to secure access.7

- Since 2021, governments and companies in industrial and multilateral organizations have made proactive efforts to expedite market development and the emergence of early market adopters. Examples include the First Mover Coalition (FMC)8 and the North American Hydrogen partnership of the United States, Canada and Mexico.

- Efforts to coordinate philanthropic, private and public funding to scale and provide more cohesive financing across the climate technology supply chain have been increasing since 2017. This is particularly aimed at helping viable technologies overcome obstacles and advance, such as the first-of-a-kind (FOAK) pilots in the pilot and early deployment stages (as shown in Figure 1) that have been developed by organizations like Breakthrough Energy.

- The development of sustainable finance frameworks, along with taxonomies and regulations for disclosure and reporting,9 has enabled institutional investors to make informed investment decisions, particularly at the full commercialization stage.

- Emerging climate tech regional hubs are bringing together producers and customers to leverage existing infrastructure systems, provide a business marketplace, develop safety standards and promote the technology.

Climate Tech: The Critical Role of Insurance

I believe developing a full suite of affordable insurance solutions is essential for making climate technologies market-ready, securing financing and managing project liabilities.

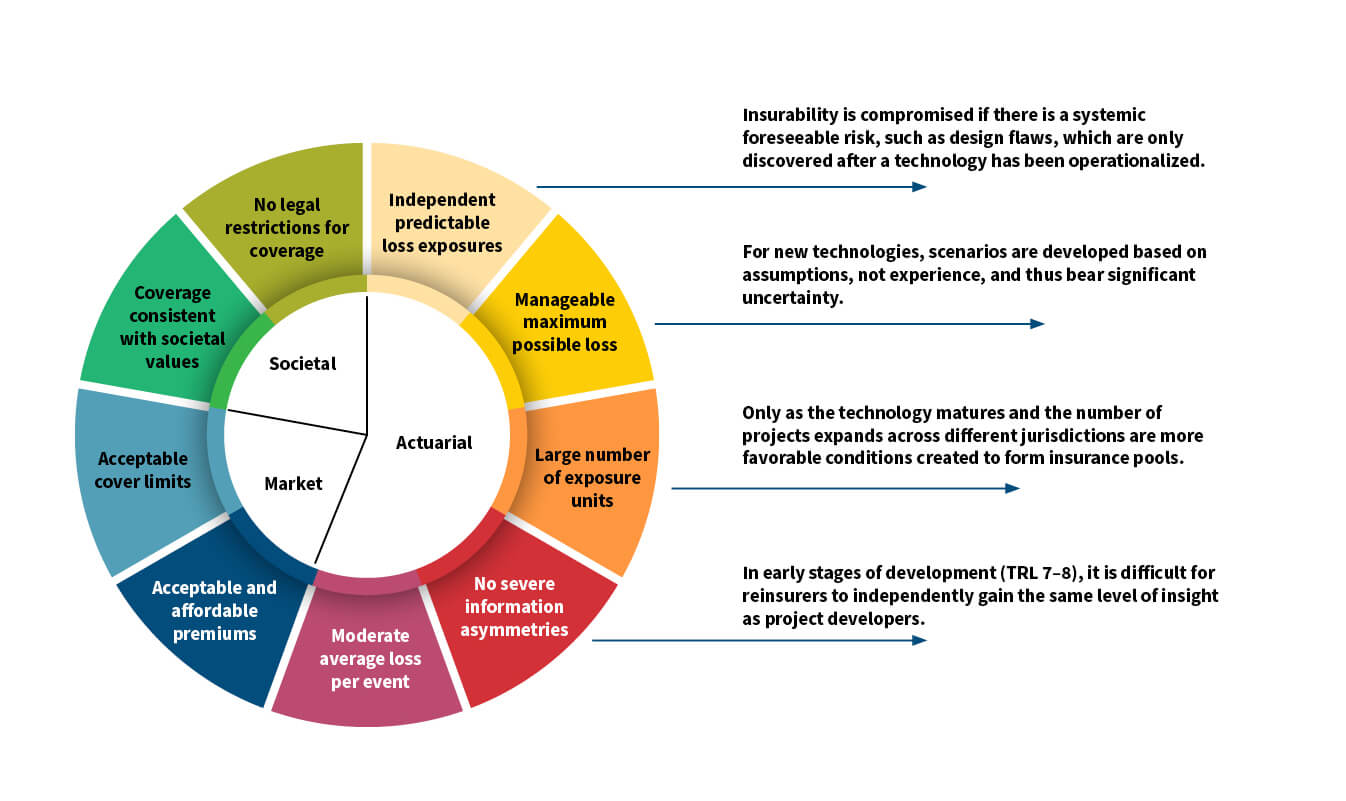

Assessing the insurability conditions for new technologies is time-consuming and complex. The decisions will not be binary (‘yes’ or ‘no’); instead, they will fall somewhere on a scale that will evolve as the technology matures and risks are identified, understood and mitigated—or at the very least, become more measurable. In the pre-commercialization stages, greater risk sharing among stakeholders (i.e., technology owners, project developers, investors, government agencies and insurers) could potentially help. As the technology matures, generally, deployment increases, risks are understood better, more data becomes available, the efficacy of risk mitigation strategies becomes more apparent and insurers could potentially take a greater share of the overall risk pool.

Figure 3 schematically outlines nine fundamental criteria of insurability10 and examples of related issues for emerging climate technologies.11

Figure 3: Assessing the Nine Fundamental Criteria of Insurability

Source: The Geneva Association

Benefits of Engaging Early With Insurance and Reinsurance Companies

Project developers may benefit from considering insurance needs as early as TRL 6 (Figure 2) as they start planning their FOAK pilot.12 Insurance-related issues also will change significantly from TRL 6 to 9. For example, the insurable value of assets at TRL 6 is relatively low, but risks and insurance needs evolve markedly for projects in commercial stages.

Engaging insurance and reinsurance companies’ risk engineers early, from pilot to early deployment stages, could potentially result in several mutual benefits:

- Increased transparency, data sharing and enhanced knowledge of the risks could permit a more holistic approach to developing the technology’s risk profile to assess insurability as it moves through the TRLs.

- Identification of data needs and monitoring requirements from an early stage may facilitate the development of databases for risk assessment and determining insurability conditions.

- Strengthened collaboration with climate tech stakeholders (e.g., project developers, policymakers, equipment manufacturers and suppliers, infrastructure operators) may aid the development of risk management strategies.

- Exposure to more projects as the TRL of the technology matures could lead to faster identification of systemic risks that could be mitigated, for example, through rethinking equipment design or government policies and interventions.

- The development of a “pool of projects” could help establish an insurance pool to spread the risks.

- Developing an understanding among climate tech stakeholders and the insurance industry could benefit the overall process. Understanding how risks could be transferred and how the risk-sharing balance might evolve over time as the technology matures could foster better relationships, especially as more risks become known or measurable.

- Identifying unique, tech-specific insurance needs could spark product innovation in commercial insurance markets and may lead to other interventions, such as public-private partnerships (PPPs) and government backstops (safety nets).

- Expedited development of risk management standards, guidelines and codes of practice may be fundamentally beneficial for project replication and widescale deployment.

Engaging Early in Project Development and Financing

Based on my experience, I’ve observed that property and casualty insurance and reinsurance companies traditionally are contacted after the project has been designed for development at an approved site. However, this often means insurance-related considerations may have been overlooked during engineering design, potentially leading to unanticipated surprises, both for untested (or not fully tested) risks and known risks that may not have been anticipated (e.g., trends of weather-related extremes). Such oversight could result in insurability challenges, delays or compromises in financing and executing the project.

Early engagement of insurers and reinsurers’ risk engineering teams at the start of pre-site selection could reduce the blind spots in risk assessment, enhance the project’s insurability and potentially shorten the due diligence period for obtaining insurance for financing, speeding up execution. Importantly, by engaging early, risk engineers could provide important feedback on critical decisions, such as where and how to build facilities and the risk mitigation strategies to consider in project design to maximize their insurability against extreme weather events over the project’s life cycle.

An Insurability Readiness Framework (IRF)

The Geneva Association recently developed a novel Insurability Readiness Framework (IRF) in collaboration with various partners across sectors to facilitate the early engagement of climate tech stakeholders with insurers’ and reinsurers’ risk engineering teams. The IRF provides a cohesive taxonomy of climate tech risks through an insurance lens. It breaks down the risks into seven insurance-relevant risk categories:

- Technology risk

- Project information and organization risk

- Legal, financial and compliance risk

- Location-specific physical climate risk (extreme weather events and trends)

- Business interruption and supply chain risk

- Long-term risk

- Environmental, social and governance (ESG) risk

For each of these risk categories, the IRF specifies a list of key issues for climate tech stakeholders to consider when framing risks in their dialogue with insurance companies. For example, under “technology risk,” issues range from a basic overview of the technology and the scale-up strategy to material selection, proof of performance, quality control and risk management in the development process.13 Importantly, the risks under IRF are linked to risk categories in the U.S. Department of Energy’s ARL framework, demonstrating the importance of insurance in enabling the various risks.14

Benefits of Utilizing the IRF

The IRF intends to enable more informed conversations among climate tech stakeholders and the insurance industry to frame risks, identify data needs, explore insurability conditions and consider risk management strategies. It also aims to focus on the most challenging risks from an insurability perspective. It may also help identify risks that may be considered uninsurable from a commercial insurance market lens that may require different interventions, such as PPPs or government backstops.

With project finance gaining more prominence in raising capital for FOAK pilots,15 transparency around insurance requirements from the early phase of project development could help align a project’s engineering design with insurance expectations—from as early as the site selection stage. This will enhance insurability at the project level, thus potentially streamlining the project development and financing process.

Applying the IRF to Two Climate Technologies

Through three Geneva Association workshops, the IRF framed and facilitated a cohesive dialogue around the range of risks associated with two major emerging technologies:

- Green hydrogen

- Carbon management (with focus on geological storage technologies and related carbon markets)

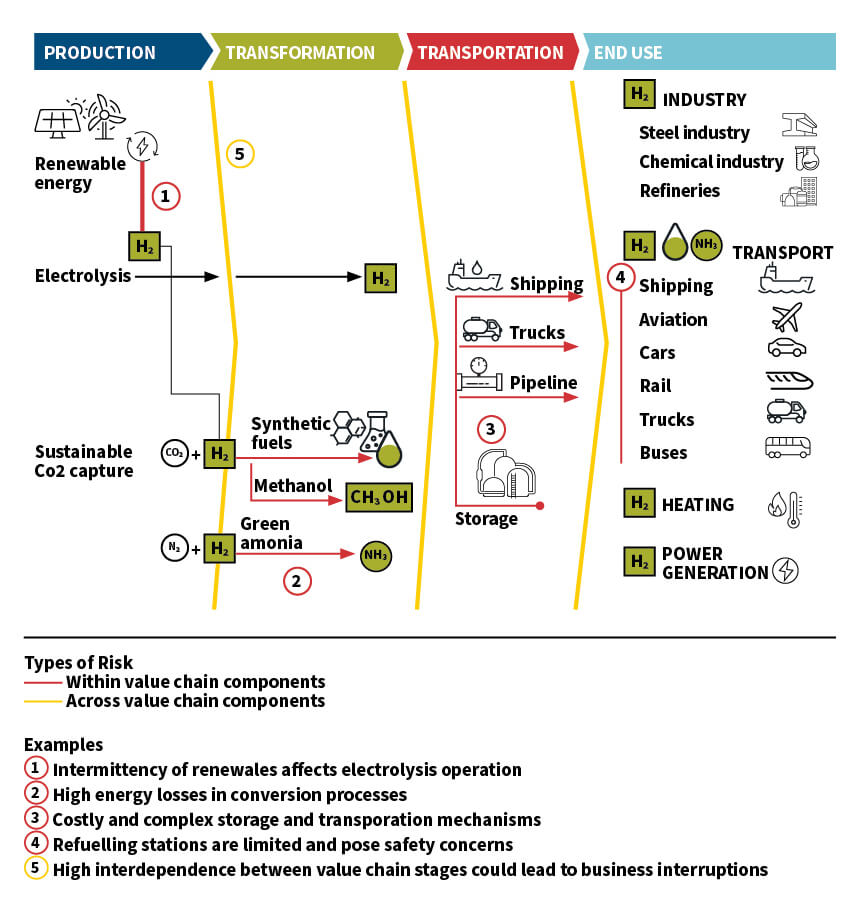

As examples, applying the IRF to complex hydrogen projects revealed risks within and across components of the project’s value chain (see Figure 4). A Geneva Association report provides more details.16

Figure 4: Complex Green Hydrogen Projects and Risks Along the Value Chain

Source: Modified by The Geneva Association from IRENA17

A Potential Way Forward—Suggestions

The insurance industry has a crucial role to play in supporting the rollout of new climate technologies. To realize these opportunities, insurance and reinsurance companies might consider the following:

- Investing strategically in building their internal expertise and capacity by expanding their risk engineering services for viable emerging climate technologies.

- Building partnerships with entities that have access to a pipeline of climate tech projects from TRL 6–7, such as EPCs, climate tech hubs, investor platforms and governments.

- Strengthening industry-level collaboration and partnerships to develop innovative risk management solutions for identifying the unique insurance needs of different climate technologies.

- Working with standard-setting and certification bodies to converge on best practices for the development of risk management frameworks and standards to facilitate project replication.18

- Emphasizing collaboration with governments, the scientific community, climate technologists and third-party technology verification and testing firms to compile data and analytics on emerging climate technologies that may already be available and translate these for insurance use.

Statements of fact and opinions expressed herein are those of the individual authors and are not necessarily those of the Society of Actuaries or the respective authors’ employers.

References:

- 1. Physical climate risk refers to impacts associated with changing severity and frequency of extreme weather events (e.g., floods, wildfires) and low changing climatic trends (e.g., water scarcity). ↩

- 2. The U.S. National Aeronautics and Space Administration (NASA) originally developed the TRL in 1974, and it was formally defined in 1989. ↩

- 3. NASA. 2023. Technology Readiness Levels. ↩

- 4. Golnaraghi, M., and I. Belanche-Guadas. 2024. Climate Tech for Industrial Decarbonization: What Role for Insurers? Zurich: The Geneva Association. ↩

- 5. For more examples and sources, see: Golnaraghi, M., H. Dimpflmaier, S. Thumm, J. Warton, L. Harding, A. Delargy, T. Krismer, E. Rauch, T. Dickson, M. Giachino, A. Norfolk, M. Repmann, M. Senac-Gayarre, J. Meister, G. Martin, F. Nieuwenhuijs and I. Belanche-Guadas. 2024. Bringing Climate Tech to Market: The Powerful Role of Insurance. Zurich: The Geneva Association. ↩

- 6. U.S. DoE Adoption Readiness Level Framework. ↩

- 7. Critical materials such as lithium, nickel and cobalt that are needed for the manufacturing of batteries, renewables and other new climate technologies for domestic use and international trade purposes. ↩

- 8. Launched by U.S. President Biden at the 2021 United Nations Climate Change Conference in Glasgow, FMC is a global initiative harnessing the purchasing power of companies (with support from governments). As of December 2022, 71 companies have joined the FMC. ↩

- 9. IFRS Sustainability Disclosure Standards. ↩

- 10. Schanz, K-U. 2023. The Value of Insurance in a Changing Risk Landscape. The Geneva Association. ↩

- 11. Berliner, B. 1985. Large Risks and Limits of Insurability. The Geneva Papers on Risk and Insurance – Issues and Practice 10, no. 37: 313–329. ↩

- 12. FOAK to Nth-of-a-Kind (NOAK) pilot projects in TRL 7 traditionally aim to assess and improve technological risks, such as technical performance, operational complexities and related safety issues to develop associated economic models. ↩

- 13. A complete template of the IRF with a list of key issues related to each risk is available in Appendix 2 of Golnaraghi, M., et. al. 2024. Bringing Climate Tech to Market: The Powerful Role of Insurance. Zurich: The Geneva Association. ↩

- 14. To see how these seven risks related to the 17 risk types in the U.S. Department of Energy’s Adoption Readiness Level Framework, see Table 3 in Golnaraghi, M., et. al. 2024. Bringing Climate Tech to Market: The Powerful Role of Insurance. Zurich: The Geneva Association. ↩

- 15. Climate Tech VC. 2024. From FOAK to NOAK. ↩

- 16. For analysis of IRF for green hydrogen and carbon management, see: Golnaraghi, M., et.al. 2024. Bringing Climate Tech to Market: The Powerful Role of Insurance. Zurich: The Geneva Association. ↩

- 17. IRENA. 2022. Geopolitics of the Energy Transformation: The Hydrogen Factor. (Figure 3.9). ↩

- 18. VdS. 2014. International Guidelines on the Risk Management of Offshore Wind Farms: Offshore Code of Practice. ↩