Coming of Age

How life insurers can cater to millennials as they become the largest living adult generation

August/September 2019Millennials have the distinction of being the most intimately observed and analyzed generation in human history. Simultaneously perceived as lazy/hard chargers, self-absorbed/altruistic and technology-addicted, this cohort can be both baffling and fascinating.

Let’s begin with some basic facts: The millennial population is, first of all, sizable. According to the U.S. Census Bureau, U.S. millennials will overtake baby boomers as the largest living adult generation in 2019, swelling to 73 million. Meanwhile, boomers, nearly half of whom are at retirement age or older, will shrink to 72 million in 2019, and Generation X, born between 1964 and 1979 (or 1981, depending on the source), will not overtake baby boomers in size until 2028.

Second, millennials are highly educated. The Pew Research Center found in a 2018 study that this generation’s members are reaching more advanced education levels at younger ages than their same-age counterparts did in prior generations. Approximately 50 percent hold at least a four-year college degree, and some of these individuals have more than one degree. Some of this is due to factors such as today’s need for a college degree for jobs that as recently as 50 years ago required only a high school education (if that), and technology’s increasing role both in work and in everyday life, requiring more advanced education and training.1 Millennials also are currently the largest component of the workforce. As baby boomers retire, millennials’ share of the workforce is rising—Pew Research Center reports this cohort comprises one-third of workers as of 2017.2

Third, millennials are society’s first “digital natives”—the first generation to be fully comfortable with and highly adept at navigating the digital world—and therefore more likely to turn to technology to research solutions for their needs. At the same time, they have a different perspective about business activity: Today’s “sharing economy” is a millennial-fostered development that encompasses ride-, car- and bicycle-sharing; crowdfunding and peer-to-peer lending; novel ways to barter for and share talent and knowledge; and more.

One difficulty, however, with analyzing millennials as a market and as a cohort is a basic lack of agreement as to who they are. Both Pew Research Center and Oracle, for example, say millennials (sometimes referred to as Generation Y) are those born between 1981 and 1996. The Guardian views 1997 as the end date for this generation, and LIMRA uses 1980 to 2000 as the bracketing years. Internet-based business intelligence provider Statista uses 1980 as the start date but does not yet give an end date, and other research firms use start dates as early as 1977 and end dates as late as 2002.

The one constant with millennials right now is that their basic market characteristics pertaining to life insurance—affluence, attitudes and financial needs—are changing rapidly. This is most likely due to aging: The youngest millennials have, for the most part, graduated from college and entered adulthood (ages 22–23), and the oldest, who are nearing age 40, are reaching their prime career years. This earmarks them as having the potential to be a highly significant market for life insurance.

Do Millennials Need Life Insurance?

The simple answer to this question is: yes. Unusually high levels of economic and social disruption over the past 20 years, stemming from technological advances, globalization and political unrest, are subjecting millennials to higher levels of financial insecurity than any prior generation.

A sizable wealth gap currently exists between this generation and previous ones and is likely to continue to grow. The Federal Reserve Bank of St. Louis reported that in 2016, family wealth for those born in 1980 was 34 percent below what earlier generations held at the same age. Youth unemployment has been high for more than a decade, and research from the Resolution Foundation in the United Kingdom found that incomes of millennials who are employed are approximately 20 percent less than those of Generation X at the same age.3

The two recessions since 2000, coupled with the soaring cost and need for higher education, have saddled millennials with student loans with high face value (approximately $33,000 per individual) and high interest (4.8 percent to 7.4. percent).4 Millennials also have high and rising levels of credit card debt—approximately 25 percent of their total debt currently.

Millennials are less likely than other age groups to know how much life insurance they need, let alone what type to buy, and are likely to assume the cost is far more than the actual cost.

Millennials are less likely than other age groups to know how much life insurance they need, let alone what type to buy, and are likely to assume the cost is far more than the actual cost.Already it is projected that by 2020—just a year from now—millennials, who will comprise 22 percent of the U.S. population, will be responsible for as much as 30 percent of retail expenditure.5

As a result, many millennials have lagged behind prior generations in entering the life stages of early adulthood. Instead of establishing independence, buying homes and starting families, approximately 40 percent are living with parents or other relatives into their late 20s and sometimes beyond6—the highest level since the years between the Great Depression and World War II.

Are Millennials Buying Life Insurance?

The simple, yet surprising, answer here is: yes—and according to LIMRA, they are buying it at higher rates than expected. LIMRA’s 2016 life insurance ownership study,7 which encompasses data from 1960 to 2016, found 70 percent of millennial households owned some form of life insurance—the largest percentage of any age group. In addition, LIMRA’s Facts About Life 2018 report found more adults under 45 owned life insurance in 2016 than in 2010, while ownership by those over age 45 dropped during the same time period.

Interestingly, millennials, unlike prior generations, are more likely to have a financial plan,8 and they actually want to buy life insurance. Their financial stability has been hard-won, and they are eager to protect what they have built. However, they are also the age group least likely to have been approached to buy life insurance in the past 12 months, according to LIMRA. And yet, despite the millennials’ purported preference for online research and purchasing, 74 percent would still prefer to talk to a financial adviser, either on the phone or in person, when it comes time to buy life coverage. Older millennials especially are more likely to look to professional financial advice. Even if they begin the process online, millennials are most likely to end it with a financial professional.

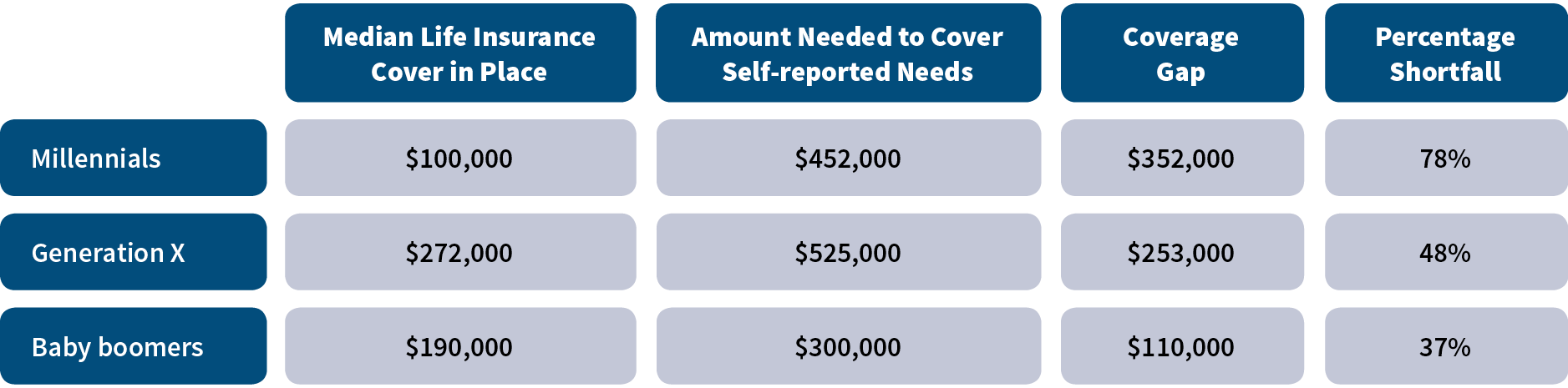

Although they are buying life insurance, the amount they buy and own, whether on an individual or group basis, is insufficient and declining, leaving them today’s most underinsured generation. The 2018 New York Life Insurance Company life insurance gap9 survey found the life insurance coverage gap for U.S. millennials, at 78 percent, is far higher than that of Generation X and baby boomers (see Figure 1). Currently, only 10 percent have enough life coverage for all of their needs, which can include mortgages, retirement or a child’s college education. The rest view their financial challenges, such as high student loan debt, saving for a home and high mortgage payments, as reasons to believe they cannot not afford sufficient life insurance.

Figure 1: Generational Life Insurance Coverage Gaps

Source: The 2018 New York Life Insurance Company Life Insurance Gap Survey

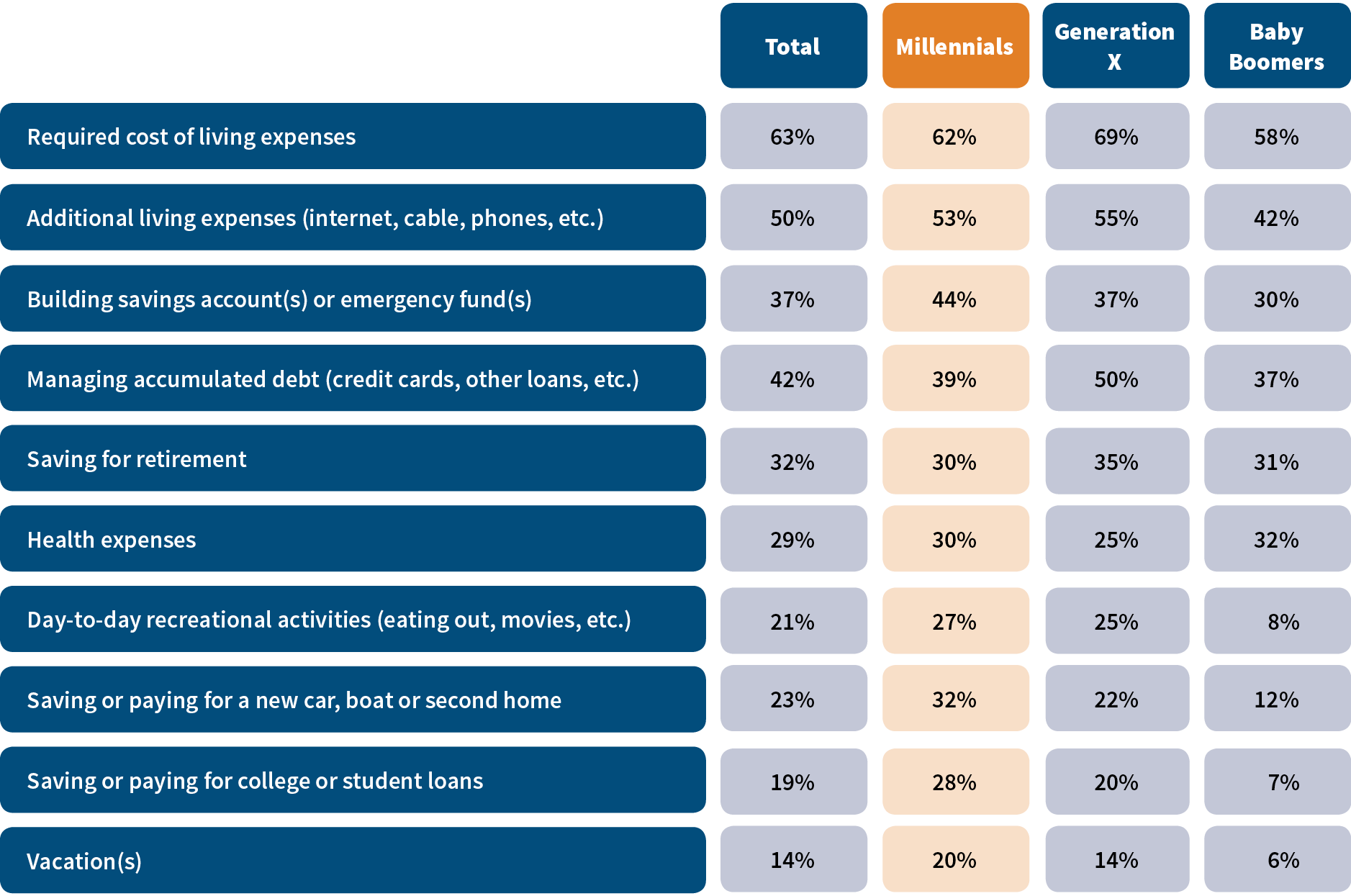

What is causing this level of underinsurance? According to LIMRA’s Facts About Life 2018 report,10 millennials are less likely than other age groups to know how much they need, let alone what type to buy, and are likely to assume the cost is far more—by a factor of five—than the actual cost.11 Figure 2 provides a more robust list of reasons why millennials don’t buy life insurance.

Figure 2: Why Millennials Don’t Buy Life Insurance

Source: LIMRA’s and Life Happens’ Insurance Barometer Study

Looking Toward the Future

Clearly, millennials see the value of life insurance, and unlike prior generations, see substantial value in obtaining long-term care insurance. This is most likely driven by the fact that many not only saw their parents become members of the “Sandwich Generation,” caring for elderly family members while still raising children, but are now entering this generation themselves.

Marketing insurance successfully to the millennial generation is evolving into a proposition quite different from reaching past generations. The well-recognized preference for gathering information via user-generated content sets millennials substantially apart. According to the digital marketing company Bazaarvoice, millennials are much more likely to be interested in products or services recommended via social media, even if the content is by strangers. This is diametrically opposed to baby boomers, who are more likely to look to friends and family for recommendations.12

Insurers must also be ready to serve the business they attract, in tech-savvy ways that will suit these customers. Frankly, a snazzy mobile app, while attractive, is not going to be enough. If that app is backed by a clunky legacy system that forces the questioner to wait 24 to 48 hours for a response or, even worse, an agent call, millennial applicants are likely to flee to companies that can provide the near-instantaneous response they’ve come to anticipate and expect.13

This is going to require, at the very least, insurers to speed up their end-to-end digitization efforts. Although companies have been working for years to move application processes away from paper, it has not been fast enough. The need to balance the human and the digital aspects of the process will be essential throughout this change. Although millennials are the most tech-savvy adult generation today, there are still nondigital needs, such as access to humans when they have questions, which companies would do well to satisfy.

The characteristics of the millennial generation, much more so than other generations, are not static. The timeline of development of this market likely will reflect that of past generations, where interest in and desire for life insurance protection will grow as they age. As millennials age and their needs evolve, their life insurance needs will undergo substantial change. Life insurers would do well to keep their attention on millennials, so that they can continuously align their product and service offerings.

References:

- 1. Fry, Richard, Ruth Igielnik, and Eileen Patten. How Millennials Today Compare With Their Grandparents 50 Years Ago. Pew Research Center, March 16, 2018 (accessed June 7, 2019). ↩

- 2. Fry, Richard. Millennials Are the Largest Generation in the U.S. Labor Force. Pew Research Center, April 11, 2018 (accessed June 7, 2019. ↩

- 3. D’Arcy, Conor, and Laura Gardiner. The Generation of Wealth: Asset Accumulation Across and Within Cohorts. Resolution Foundation, June 20, 2017 (accessed June 7, 2019). ↩

- 4.Northwestern Mutual. 2018 Planning & Progress Study—Advisors: Key to Financial Clarity (accessed June 7, 2019).

↩ - 5. Statista Research Department. Millennials: Annual Expenditure of U.S. Consumers in 2013 and 2020 (in Trillion U.S. Dollars). Statista.com, June 1, 2013 (accessed June 7, 2019). ↩

- 6. Picchi, Aimee. Young Adults Living With Their Parents Hits a 75-year High. CBSNews.com, December 21, 2016 (accessed June 7, 2019). ↩

- 7. LIMRA. Opportunity Knocks: The U.S. Life Insurance Market 2016. LIMRA.com (accessed June 7, 2019). ↩

- 8. Guardian Life Insurance Company of America. Millennials and Money: Understanding What Drives Financial Confidence. July 2018 (accessed June 7, 2019). ↩

- 9. New York Life Insurance Company. New Study Says Millennials Most “at Risk” Generation When It Comes to Life Insurance. NewYorkLife.com, November 13, 2018 (accessed June 7, 2019). ↩

- 10. LIMRA. Facts About Life 2018. LIMRA.com, September 2018 (accessed June 7, 2019). ↩

- 11. Leyes, Maggie. Key Findings for the 2018 Insurance Barometer Study. Life Happens, April 10, 2018 (accessed June 7, 2019). ↩

- 12. Bazaarvoice. Talking to Strangers: Millennials Trust People Over Brands. January 2012 (accessed June 7, 2019). ↩

- 13. Oracle. Digitizing Insurance From the Inside Out: The Back-end Solution to Winning Millennials (accessed June 7, 2019). ↩

Copyright © 2019 by the Society of Actuaries, Chicago, Illinois.