Digitize or Die!

Technology has changed the insurance landscape for good

December 2019/January 2020Photo: istock.com/sitthiphong

The development of technology is usually beyond human expectations. Years ago, people never imagined that a simple device (cell phone) plus a single software (application) with one sign-in could be the gateway to so many different products or services. For example, super apps in China (WeChat and Alipay) have bundled versatile functions, including instant messaging, social media, electronic payments and taxi reservations.

The advancement is so subversive that people may see this as the fourth industrial revolution in human history. Just like the steam engine is the symbol of the first industrial revolution, electricity symbolizes the second and the computer marks the third, digitalization (fusion of the internet, data and automation) is leading the charge of the fourth industrial revolution. Digitalization is ingrained in our daily lives, and the financial services industry is on the brink of a major revolution when digitalization enters a new phase.

Emerging InsurTech Trends

The implementation of new and innovative technology transforms the way in which insurers do business. KPMG’s Global FinTech 100 features the companies that are truly digitizing and creating new products and services in the financial field. In the 2018 Global FinTech 100, there are a total of 12 insurance innovators from North America, Asia and Europe. The sectoral breakdown shows that insurance lags behind payment (34 companies), lending (21 companies) and wealth (14 companies). But, surprisingly, insurance is ahead of neo-banks (10 companies). It is pleasing to see that the insurance industry is knocking hard on the door of the new digitized world.

In 2019, another in-depth research study KPMG conducted on the insurance industry revealed 10 key trends of InsurTech based on experiences across multiple regions. The current and emerging trends are expected to reshape insurance companies globally over the next couple of years. These trends include the notions that:

- Customer satisfaction will be a more important key performance indicator (KPI) than operational efficiency.

- The incumbent insurers will likely learn from the new highly automated insurance platforms and adopt their technology in underwriting, pricing, claims and so on.

- Claim settlement is expected to become one of the most important elements of customer engagement. It is now more about the user experience and the speed of the settlement.

- Health ecosystems are essential for the future success of those operating in the life insurance sector. Without access to the relevant data sets, insurers could not manage risks and engage with customers effectively.

- It is necessary to apply digitalization to the business model, which requires a culture change and compatibility with the market segment.

- Data is the lifeblood of the new order, and the price of data is going up.

- Artificial intelligence (AI) and machine learning likely will be the biggest drivers of efficiency. To this point, AI and machine learning have been massively applied in the automation of processes.

- The changes in automobile insurance coverage, from insuring individuals to insuring vehicles, will continue. It is possible that auto insurance could be split, with individuals holding a general third-party liability coverage and vehicles “holding” their own damage coverage.

- Big data and new technology may force the oldest professionals, like actuaries and underwriters, to take new roles where their specific skill sets could be redeployed to meet emerging needs.

- Organization transformation is crucial to the success of the insurers that are willing to digitize their business. It includes the recruitment of digital talents, the dynamic structure of a digital model, redefinition of processes and systems, vibrant ways to interact with clients and so on.

Disruptive Insurance is Driven by Digital Technologies

Using big data and intelligent models to improve productivity has taken root in people’s minds. More insurance players are actively engaged in the development, application and improvement of intelligent technology.

In 2018, AIG launched a cross-border insurance policy using blockchain’s digital ledger. Blockchain enables data sharing across a network of individual computers, and it helps solve the biggest challenge insurers face by eliminating silos of information. The technology improves the transparency and efficiency of the transaction.

AI is commonly used in robotic process automation (RPA). RPA has been shown to perfectly match the needs of a chat box platform (CBP). Using the technology of natural language processing/understanding (NLP), RPA can handle very complicated queries from clients. It is estimated that around 90 percent of repeatable, standardized work with clear rules could be processed by RPA.

Additionally, the internet of things (IoT) has been vastly applied in the auto insurance sector. European insurance giant Generali is also investing in data-driven fraud detection to fight against claim fraud.

With the application of AI and cloud computing, Ping An Life launched a “Smart Customer Service” to process more than 96 percent of new applications without any manual interference. On the other hand, Ping An P&C applied big data and machine learning in the process of handling the vehicle claims. With high accuracy output from object recognition, Ping An now closes more than 98 percent of claims within one day.

Insurance is deemed a traditional financial service. Value is the key measure to evaluate how well an organization is doing. Disruptive technology forces insurers to rethink:

- What additional value is provided to the client.

- How data and technology can garner more client insights.

- How we can build better connections with clients.

- What the differentiator of products will be.

- How any ecosystem would make work more efficient and effective.

- How to transform the practice of insurance ultimately.

Changing Customers and Changing Needs

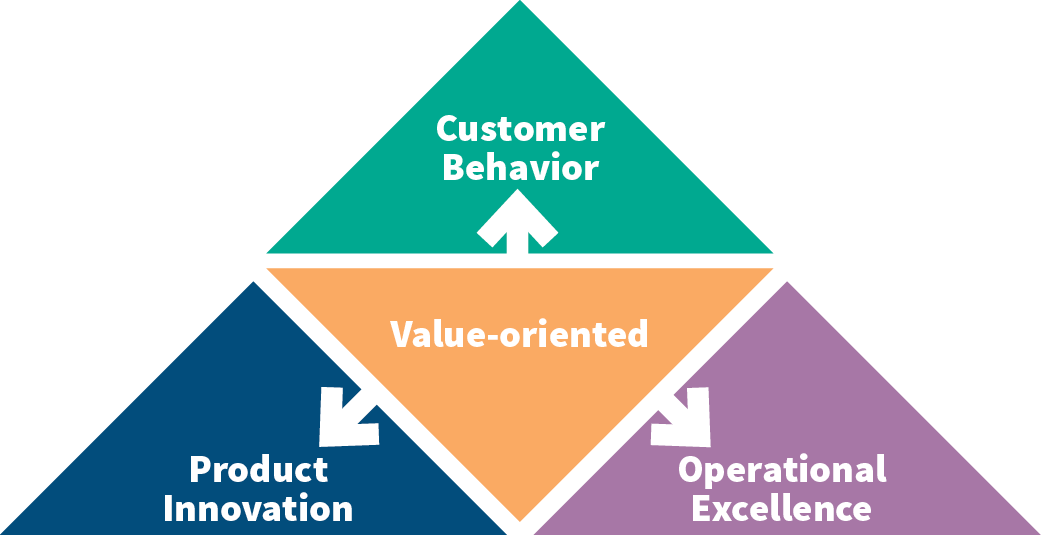

The world is changing fast, and so is the customer (see Figure 1). When you realize from the population pyramid that millennials are set to become the largest living generation, you must admit they will overtake older consumers as the biggest spenders. They are the revolutionary force affecting the market today. That being said, insurers need to figure out who they are:

- There are 2.5 billion millennials globally.

- They comprise one-third of the world’s total population.

- Their generation’s size is 1.5 times larger than Generation X.

- More than 90 million millennials reside in North America, and 400 million reside in China.

Figure 1: Opportunities From Disruptive Technology

Besides those demographic characteristics, what kind of behaviors do millennials demonstrate?

Millennials Are Digitally Savvy and Socially Active

- More than 50 percent check their phones at least once every 10 minutes.

- They shop online more frequently than previous generations.

- They actively comment via social media.

- They are easily influenced by online celebrities.

Millennials Advocate Sustainability and Equality

- They prefer to work for brands that share their personal values.

- They purchase sustainable goods and services.

- They support fairness and diversity.

Millennials Have a Distinctive Lifestyle

- They prefer to spend on experiences over assets.

- They adore a sharing concept like Airbnb and Uber.

- They love mobility and working in pioneering jobs (like startups).

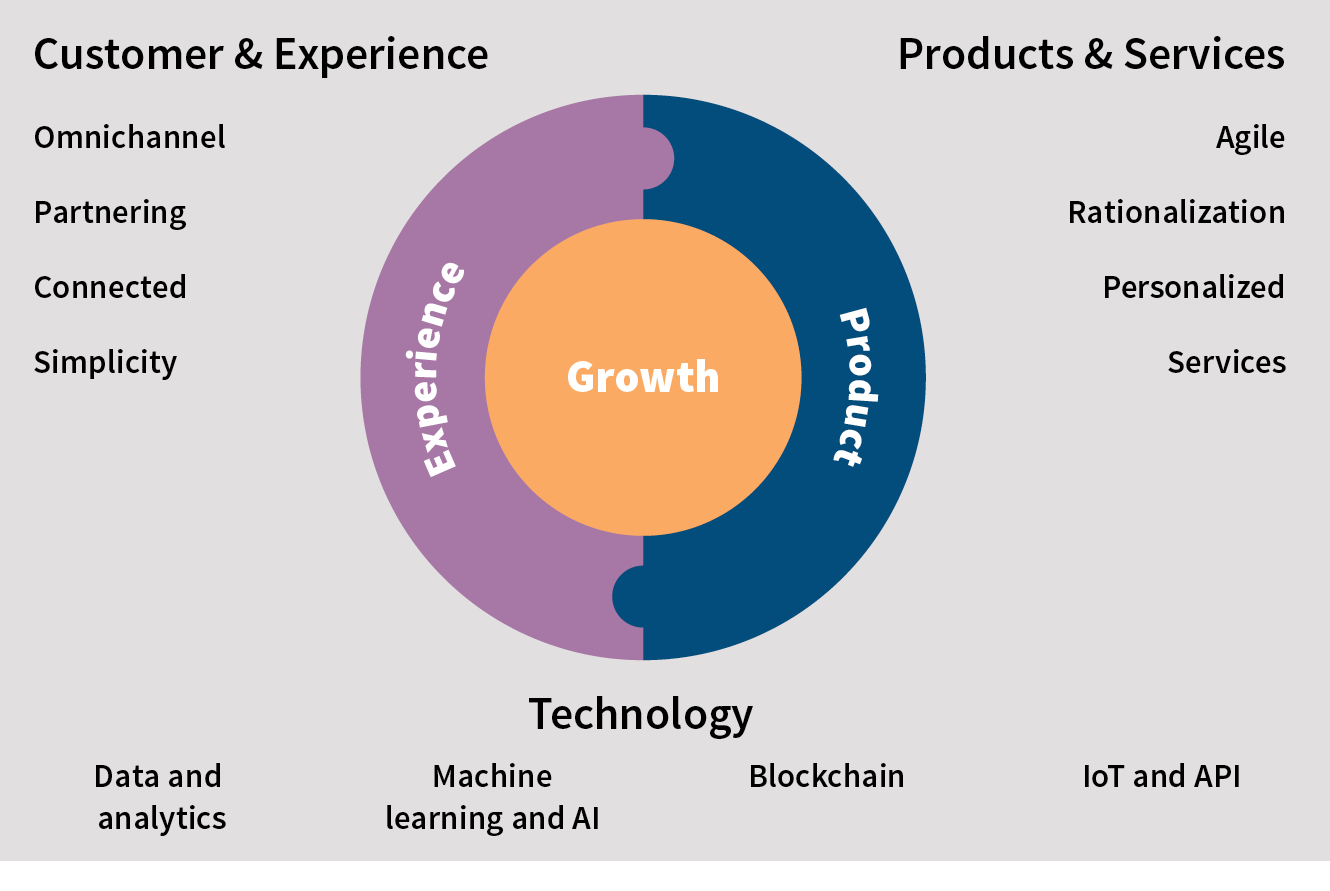

Indeed, insurers could leverage these facts to secure growth by meeting millennials’ expectations and needs. There are three key areas for insurance players to invest in (see Figure 2).

Figure 2: Key Areas for Insurers to Invest In

Customer and Experience

- Launch an omnichannel content strategy to offer a seamless experience both online and offline.

- Partner with other service providers, like WhatsApp and Facebook, to interact with customers.

- Connect customers with various devices like wearables, sensors and voice robots.

- Simplify communication by providing precise and timely updates.

Products and Services

- Provide agile products that recognize and react to life events and changes of circumstance.

- Rationalize the basis for underwriting and pricing, using both external and internal data sets.

- Personalize products and services for the right customer at the right time.

- Embed value-added services to transform products into solutions.

Technology

- Sharpen data analytics skills to process both structured and nonstructured data.

- Leverage machine learning and AI to streamline the operational process.

- Explore blockchain to track medical history and authorize claims instantly.

- Boost the growth of usage-based insurance thanks to IoT; provide precise pricing basis and strengthen risk mitigation measures.

Real Business Examples

Oscar Health

Oscar Health is a U.S. company that provides health insurance for both individuals and employers. The company is applying big data and machine learning to reinvent preventive health care management and claims processing in an effort to reduce the cost of health care.

Most successful digital insurers adopt a different organizational structure to speed up the claim sprocess, shorten the turnaround time and maximize efficiency.

Most successful digital insurers adopt a different organizational structure to speed up the claim sprocess, shorten the turnaround time and maximize efficiency.In the transition of health insurance, the charge basis has shifted from being results-oriented to focusing on the prevention of diseases. Health insurers should consider encouraging customers to demonstrate healthy behavior and charge fees accordingly.

As an InsurTech company, Oscar innovatively has introduced intelligent devices to provide health management programs for customers. Oscar also offers wearable devices to monitor supplementary exercise and overall health. Customers are rewarded with an Amazon voucher if they meet healthy standards.

Lemonade

Lemonade is a U.S. company that offers renters and home insurance policies for homes, apartments and condos. Lemonade created a new business model based on behavioral economics and technology.

The company uses behavioral economics research to displace fraud and conflict while removing motivation for minor claims and keeping in check the inclination to defraud an insurer. It uses AI in the form of chatbots and machine learning to provide insurance policies and handle claims, replacing brokers and eliminating paperwork. When a customer applies for insurance, the company’s software pulls data and information about a particular home or neighborhood from a variety of sources. Policyholders file claims through the company’s chatbot, A.I. Jim, who reviews the claim, cross-checks it with the policy, runs 18 different fraud algorithms and determines whether to approve the claim.

Besides technology applications, Lemonade differentiates its business model from traditional companies with its focus on doing good. It keeps a flat 20 percent of a customer’s premium to cover expenses and uses the remaining 80 percent to pay claims and purchase reinsurance. Unclaimed premiums, called “giveback,” are donated to designated charities.

ZhongAn

ZhongAn is the first online P&C company in China. It applies technologies such as big data, cloud computing, blockchain, AI and IoT to achieve product customization, dynamic pricing, scenario-based sales and automated claims settlement. ZhongAn is also the first listed InsurTech company in China and has attracted billions of dollars from investors.

ZhongAn’s strategy is “Insurance + Technology.” Besides incorporating technology development into the insurance value chain, it also is commercializing technology’s strengths in insurance markets.

In November 2016, ZhongAn announced it founded a subsidiary, ZhongAn Technology, which would focus on technology solutions and boost the informatization of the insurance industry. Last September, ZhongAn Technology reached a deal to establish a cloud-based end-to-end operating system for Japanese P&C company Sompo.

Digital vs. Traditional Insurance

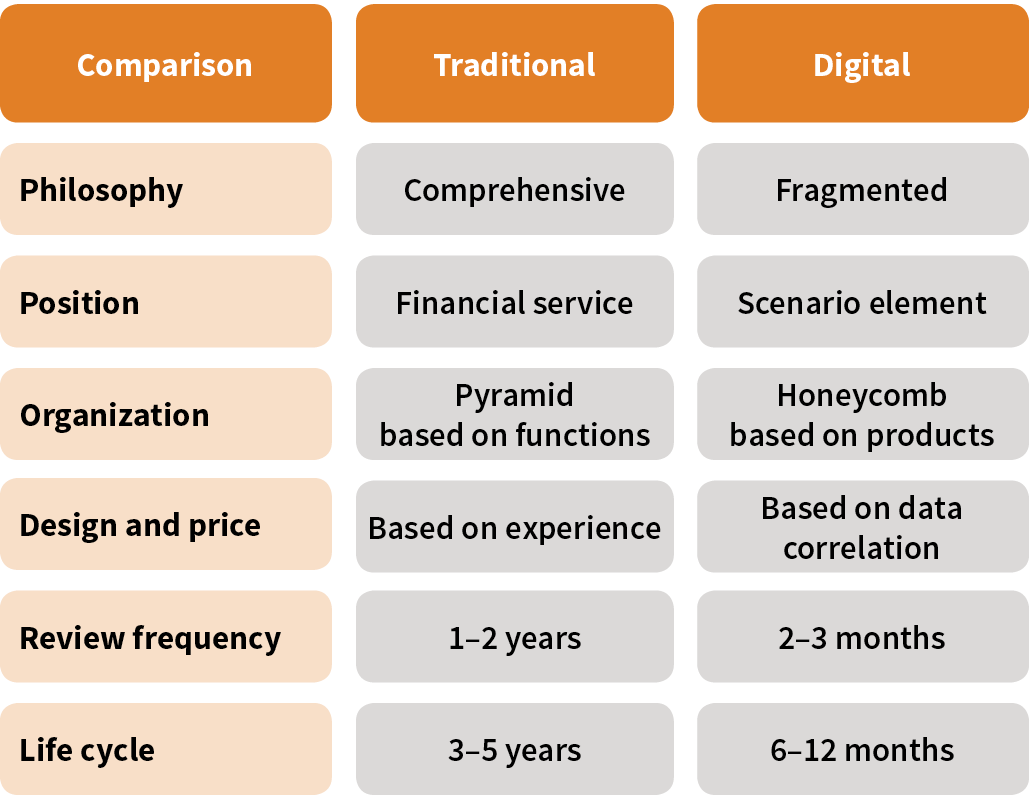

Digital insurance differs from traditional insurance in many aspects (see Figure 3). Besides the application of new technologies, digital insurance also adopts a totally different manner in which to run the business.

Figure 3: Key Insurance Features Comparison

Traditional insurance provides comprehensive coverage, aiming to provide benefits as fully as possible in a bundled policy. Typically, it is a combination of a basic plan and various riders like accident, critical illness and so on. Traditional insurance typically is high-sum assured and low frequency, and has a long coverage period. In contrast, digital insurance is always designed in the form of low-sum assured, high frequency and over a short period of time. Besides comprehensive coverage, digital insurance also can provide fragmented coverage.

Insurance is a financial service to meet clients’ needs. However, digital insurance is embedded into various scenarios to serve the specific needs of these scenarios—it does not independently exist. For example, travel insurance is bundled with a tour package in a travel app, or accident insurance is offered on the website when you book a tennis court.

Most successful digital insurers adopt a different organizational structure to speed up the claims process, shorten the turnaround time and maximize efficiency. Compared to the traditional pyramid structure based on function, digital operators make the business line independent. Each business line is focused on products that make other supporting functions into even more products, making sure the product could be launched or upgraded responsively according to market circumstances.

It is worth noting that digital insurance products need to be revisited more frequently, for the terms and conditions (T&C) and price. The cycle could be as short as a couple of months. A few players admit much of the fragmented coverage, especially for new risk exposures, is actually priced based on trial and error, different from the traditional “rule of large numbers” pricing strategy. Digital insurance relies much more on the relationships of many nonstructured data sets. One realistic way to price this type of insurance is to have a hypothesis (T&C and prices) and then test it with the real experience, refine, retest and so on.

A Case Study of a Digital Insurance Product

One privately owned Chinese insurance company called Funde Sino Life launched a product three years ago that has received a lot of digital awards. The product, “Baby’s Piggy Bank,” is a common education savings plan for university expenses. In the eyes of actuaries, the benefit is simple: It is a single premium policy that will refund four times cash when the individual turns ages 18, 19, 20 and 21. But why was it so popular and welcomed by clients?

The product has a very clear target client segment: young parents with small children. The key pain points of these young parents include:

Like the financial industry, insurance is transforming with the emergence of disruptive technology, evolving customer expectations and stringent regulatory requirements.

Like the financial industry, insurance is transforming with the emergence of disruptive technology, evolving customer expectations and stringent regulatory requirements.- They are not disciplined with their spending in daily life.

- They don’t like a long and regular savings plan (they spend money on experiences).

- They have a low sense of financial responsibility.

To address those concerns, the Baby’s Piggy Bank product was designed as a single premium, but it allowed for additional funds (of any amount) to be contributed at any time. The company created different scenarios for parents to “top up.” The key is to link the top up with memorable moments of growth and maturity, such as:

- During Chinese New Year, children say good wishes to seniors. In return, seniors will give “red pocket” to kids. This pocket money could be used to top up.

- Say a child gets a high score on a final exam. Instead of giving the child money as a reward, parents can top up instead.

Those scenarios make the top-up similar to daily spending—just like buying a coffee or a magazine, it is not a big deal. And every time they top up, clients are invited to mark down the feeling, reason or any wishes in the form of text, voice recording or video blog (vlog).

On top of that, Funde Sino Life developed fancy tools and a modern interface. Young parents love to use the “storyline” to recall the important moments by reloading the text, voice memo or vlog from the cloud.

Last but not least, the company takes advantage of social media to share the storyline with grandparents, other relatives and friends. By sharing this information, others feel like they are accompanying the kids growing up, even though they may not live nearby or be a part of their daily lives.

Like the financial industry, insurance is transforming with the emergence of disruptive technology, evolving customer expectations and stringent regulatory requirements. Without digitalization, insurance players would not be able to compete with other service providers. Although the traditional insurance model still contributes the majority of industry business, digital insurance has grown significantly in the past few years due to the widespread use of cell phones, e-payments, facial recognition technology and so on.

There is no doubt digital insurance will overhaul traditional insurance and dominate the industry in the near future, providing a better customer experience, more precise pricing, tailored services and 24/7 accessibility. Digitize or die! This is not even a question for the future. It is happening now.

Copyright © 2019 by the Society of Actuaries, Chicago, Illinois.