Firearm Risk: An Insurance Perspective

Actuaries can apply their skills to help quantify firearm-related risk

June/July 2018Disclaimer: The Society of Actuaries makes no endorsement, representation or guarantee with regard to any content, and disclaims any liability in connection with the use or misuse of any information provided in this series of articles. Statements of fact and opinions expressed herein are solely those of the authors and are not those of the Society of Actuaries or the respective authors’ employers.

In the 2017–2021 Society of Actuaries (SOA) Strategic Plan, the SOA promises its stakeholders that actuaries will “provide trusted and objective actuarial research, analysis and insight on important societal issues.”1 Firearm deaths and injuries are a significant problem in the United States and an important societal issue with actuarial and insurance aspects. Indeed, the American Medical Association recently called firearm violence “a public health crisis” and called for a comprehensive public health response and solution.2

Gun violence in America exacts a significant toll on our society in both human and economic terms. The economic cost of firearms directly affects the financial outcomes of insurers and taxpayers. Actuaries are well positioned to study the mortality and morbidity related to firearms, yet there is little on the topic in actuarial and insurance literature.

In this article, we provide a brief overview to introduce actuaries to the scope of firearm deaths and injuries, and we examine the extent to which actuaries and insurance professionals have studied or addressed the issue. We compare firearm risk to risks that are often considered in the underwriting process for life and homeowners insurance. We find that the death rate for firearms is material, largely not considered in insurance underwriting, and larger than at least one factor that is considered in insurance underwriting. We outline open research questions and encourage actuaries to apply their skills and talents to quantifying firearm-related risk.

We deliberately do not take a stand on policy issues related to firearms. Rather, we focus on the associated insurance risks, share known data and call for further research.

GUN DEATHS AND INJURIES IN THE UNITED STATES: FREQUENCY AND COST

We summarize the frequency of fatal and nonfatal gunshot wounds in a series of tables and graphs. The data for Figures 1–4 were extracted from the Centers for Disease Control and Prevention (CDC) Web-based Injury Statistics Query and Reporting System (WISQARS).3 In Figure 1, we show the annual average number of fatal and nonfatal gunshot wounds (GSW) in the United States during the period 2010–2015. The graph in Figure 2 shows the year-by-year data. In both figures, we include the number of auto fatalities for comparison. Firearm fatalities are the third leading cause of injury-related death, just behind motor vehicle fatalities.4 Indeed, in recent years, the difference between the two has been less than 0.5 percent, and firearm fatalities have now exceeded automobile fatalities in 21 states.5,6

| Figure 1: Annual Average Number of Fatal and Nonfatal Gunshot Wounds, 2010–2015 | ||||

|---|---|---|---|---|

| Gunshot Wounds (GSW) | ||||

| Auto Fatalities | Fatal GSW | Nonfatal GSW | Total GSW | |

| Annual Average 2010–2015 |

34,351 | 33,511 | 79,846 | 113,357 |

Figure 2: Annual Number of Fatal and Nonfatal Gunshot Wounds, 2010–2015>

Hover Over Image for Specific Data

In Figures 3 and 4, we show fatal and nonfatal GSW by intent for 2015. We note that suicides account for 61 percent of fatal GSW. This is stable over the six-year period: 61 to 64 percent of fatal GSW were attributable to suicide. In both figures, legal intervention (deaths or injuries “inflicted by police or other law enforcement agents, including military on duty, in the course of arresting or attempting to arrest lawbreakers, suppressing disturbances, maintaining order and performing other legal actions”) is grouped with homicide or assault. Such incidents comprise only a small fraction, approximately 1 percent, of fatal and nonfatal GSW in 2015 (484 fatalities and 912 nonfatal GSW).

Figure 3: Fatal Gunshot Wounds by Intent, 2015

Hover Over Image for Specific Data

Figure 4: Nonfatal Gunshot Wounds by Intent, 2015

Hover Over Image for Specific Data

Estimates of the cost of gun violence vary. In recent studies, Spitzer et al. found that between 2006 and 2014, the average annual cost of initial inpatient hospitalizations for GSW was $734.6 million.7 Gani et al. estimated the average emergency department and inpatient charges for the same period at $2.8 billion per year.8 The first figure is based on hospital costs while the second is based on charges; the cost-to-charge adjustment was not applied in Gani et al. For more data on cost, we refer the interested reader to Salemi et al.,9 Lee et al.,10 Livingston et al.,11 Cook and Ludwig,12 and Peek-Asa et al.13 We emphasize that these studies capture only an initial snapshot of the cost of treating GSW; they exclude follow-up care such as procedures and treatments to address complications, rehabilitation, physical or occupational therapy, mental health care and so on. These snapshots fail to capture the potential “long-tailed” nature of claims related to GSW.

ARE ACTUARIES AND INSURERS CONSIDERING FIREARM RISK?

In this section, we describe the extent to which actuaries and insurers are studying or quantifying firearm risk. We found only one article in an actuarial journal. However, there is evidence that some actuaries and insurance companies are recognizing firearm-related risk through their product offerings, pricing and underwriting decisions in at least a limited way. We have summarized these findings:

- Lemaire used multiple decrement techniques to compute the reduction in life expectancy and the increase in life insurance premiums in the United States due to firearm violence.14 To the best of our knowledge, this is the only paper in the actuarial scholarly literature related to firearm risk.

- As states began passing laws to allow school staff members to carry firearms, some insurance companies responded by terminating liability or workers’ compensation coverage, or by imposing premium increases per armed staff member.15

- At least three companies offer Workplace Violence Expense Insurance to cover expenses associated with incidents of workplace violence.16,17,18 Moreover, Workplace Violence and Active Shooter Response are active areas of risk management.19

- Some companies offer gun liability insurance. Indeed, the National Rifle Association (NRA) endorses a line of personal firearms liability insurance as well as self-defense insurance, which provides coverage in the event that a policyholder uses his or her gun in an act of self-defense.20,21

- Bills were introduced in four states (Hawaii, New Hampshire, New York and California) to mandate liability insurance for gun owners.22 On the other hand, a Florida law passed in 2014 prohibits insurance companies from using firearm ownership as a factor in insurance underwriting.23 We did not find evidence that actuaries had analyzed or weighed in on these legislative measures.

DO FIREARMS INTRODUCE RISK?

There is extensive literature on this topic, including individual-level studies, ecological studies, survey papers and meta-analyses. Multiple studies have concluded that a firearm in the home is a risk factor for suicide, domestic violence homicide and accidental shootings, and that higher levels of gun prevalence are positively associated with higher homicide rates. We refer readers to the papers by Hemenway,24 Hepburn and Hemenway,25 Miller et al.26 and Stroebe;27 the meta-analysis by Anglemeyer et al.,28 and the references contained therein; as well as the recent article in Scientific American.29

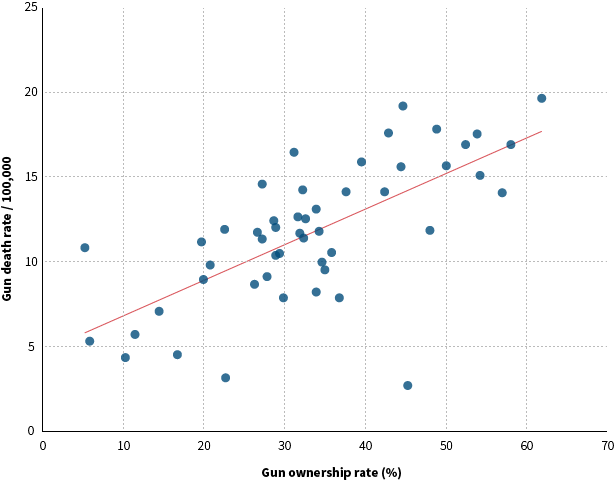

Again, there is an extensive body of literature that addresses this question, but one can visualize the association between the firearm death rate and gun prevalence in Figure 5, which is based on publicly available data.30,31 This relationship is approximate, as estimates and measures of gun ownership vary.

Figure 5: Firearm Death Rate Versus Firearm Ownership Rate by State, 2013

Sources: Xu, J., S. L. Murphy, K. D. Kochanek, and B. A. Bastian. 2016. “Deaths: Final Data for 2013.” National Vital Statistics Reports 64 (2). http://www.cdc.gov/nchs/data/nvsr/nvsr64/nvsr64_02.pdf.

Kalesan, B., M. D. Villarreal, K. M. Keyes, and S. Galea. 2016. “Gun Ownership and Social Gun Culture.” Injury Prevention 22 (3): 216–220. http://dx.doi.org/10.1136/injuryprev-2015-041586.

We, along with the authors cited previously in this article, emphasize that none of the studies prove causation, but rather a statistical association. In their literature review on firearm availability and homicide, Hepburn and Hemenway wrote, “None of the studies prove causation, but the available evidence is consistent with the hypothesis that increased gun prevalence increases the gun death rate.”32

IS FIREARM RISK COMPARABLE TO OTHER INSURANCE UNDERWRITING FACTORS?

In this section, we compare firearm risk to other factors that are used in the underwriting of life insurance and homeowners insurance. We note that we are considering only risk and the financial impact of covered risks, not the social and political forces that influence the selection of underwriting criteria.

For life insurance, risky avocations such as private aviation, scuba diving and rock climbing might be considered in the underwriting process, though firearm ownership generally is not. Using publicly available data, Tavernier and Vadiveloo computed a death rate per million “participants” in various risky avocations and compared that to a death rate per gun owner.33 The calculations are detailed in Tavernier and Vadiveloo’s paper titled “Firearms as an Underwriting Characteristic;” however, since this source is an unpublished student thesis, we walk through some of the calculations and cite their original sources as well. The results are summarized in Figure 6.

| Figure 6: Fatality Rates for Firearms Versus Scuba Diving | ||

|---|---|---|

| Risk | Deaths per Million Participants | Life Insurance Underwriting Factor |

| Scuba diving | 164 | Yes |

| Firearm in the home | 240–450 | No |

Source: The authors’ own calculations and data from Tavernier, R., and J. Vadiveloo. 2017. “Firearms as an Underwriting Characteristic.” Undergraduate Student Thesis. Department of Mathematics, University of Connecticut.

For scuba diving, the estimated death rate is given as 16.4 per 100,000 scuba divers.34

For firearms, we estimate a death rate attributable to firearm ownership. More specifically, for the numerator, we must estimate the number of deaths that are attributable to firearm ownership. For the denominator, we must estimate the number of gun owners or gun-owning households.

Of course, not all gun deaths result from the fact that an individual chose to engage in the possibly-risky activity of firearm ownership. If a woman accidentally kills herself while cleaning her gun, one can argue that her death was attributable to her choice of risky avocation. However, if one is the victim of a random gun murder, his gun ownership status could be independent of his cause of death. Thus, the correct choice for the numerator is unclear. For that reason, we use a range of 18,000 to 33,000. At the maximum, our numerator includes all firearm deaths. At the minimum, we include only suicides.35 However, since we are thinking specifically in the context of insurance, we reduce the number of suicides from 20,000 to 18,000 to reflect the fact that some suicides would occur during the suicide exclusion period. Based on Tables 1 and 3 of Tseng’s study,36 Tavernier and Vadiveloo proposed a reduction of 10 percent.37 Of course, not all firearm victims are insured—nor are all scuba participants. But this analysis is still useful as a measure of relative risk.

In addition to the variation in the numerator, there is considerable variation in the denominator, as estimates of the number of gun owners vary. The challenges of quantifying gun ownership, availability, prevalence and use are detailed in Hepburn and Hemenway’s paper,38 as well as Chapter 3 of the National Research Council’s review.39 We choose denominators ranging from 40 million to 75 million. At the low end, we use the General Social Survey’s (GSS) estimate of a 32 percent gun ownership rate multiplied by the 126 million households in the United States.40,41 At the high end, other sources suggest the total number of gun owners is as high as 75 million.42

This variability produces a wide range for our estimated death rate attributable to firearm ownership. If we include only the adjusted number of suicides (18,000) in the numerator, our estimate ranges from 240 to 450 gun deaths per million gun owners. If the numerator included accidental shootings and domestic violence homicide, for example, the estimated death rates would be higher. If we include all gun deaths (33,000) in the numerator, the range of estimates increases to 440 to 825 deaths per million gun owners. However, as we remarked previously, some gun deaths are completely independent of one’s gun ownership status.

Despite the wide range in our estimated death rate attributable to gun ownership, it is worth noting that, even at the low end, the death rate attributable to firearms of 240 deaths per million gun owners is 46 percent higher than the death rate attributable to scuba diving. The latter is used in life insurance underwriting, while the former is not.

Furthermore, while using death rates “per participant” might be an appropriate measure for assigning an insurance rating class once participation has been confirmed, the overall death rate per million of a population might be more relevant when deciding which activities to ask about on an insurance application. Given that the scuba participation rate is much lower than the gun ownership rate, a decision to ask about scuba participation and not gun ownership seems difficult to justify.

For homeowners insurance, risky features in the home such as swimming pools, trampolines and aggressive breed dogs are generally considered in the underwriting process, while firearm ownership is not.43,44 It is natural to ask whether the risk of a firearm in the home is comparable to the risk of these other household features.

Estimates of the number of trampoline-related injuries range from 100,000 per year45 to 295,000 per year.46 Some of these injuries might result in a homeowners claim. We did not find a reliable estimate of the number of household trampolines; thus, we did not calculate a loss rate.

As we pointed out previously, there are about 113,000 fatal and nonfatal GSW per year. Not all firearm-related losses would result in a homeowners claim, as intentional and illegal acts would be excluded. However, some suicides, homicides, assaults, unintentional shootings and even mass shootings could result in a homeowners claim against the gun owner’s policy. In addition, firearm theft could result in a homeowners claim. The Department of Justice (DOJ) estimates that approximately 232,000 guns were stolen per year during the six-year period from 2005–2010,47 while Hemenway et al. estimate 250,000 gun theft incidents per year, with about 380,000 guns stolen.48

In computing a homeowners loss rate due to firearms, the correct choice for the numerator is unclear. But beyond examining claim frequency for household risks, one should also examine claim severity. Homeowners claims related to firearms could include high-dollar liability settlements. For example, the mass shootings in Columbine, Colorado, and Newtown, Connecticut, resulted in homeowners settlements.49,50 But even more “routine” gun accidents could lead to significant settlements.

In the next section under “Claims Analysis,” we recommend a systematic study of the frequency and severity of firearm-related claims for homeowners and other lines of business.

OPEN RESEARCH QUESTIONS

There is a clear need for unbiased and objective research on the economic impact of firearms. Webster et al. point out: “Gunfire from assaults, suicides and unintentional shootings exacts an enormous burden on public health globally. The available science, however, is limited to answer many important questions necessary for mounting successful efforts to reduce gun violence. Certain data are lacking, and there are numerous analytical challenges to deriving unbiased estimates of policy impacts. Significant investments in research over the long term are warranted to answer questions central to successful prevention of gun violence.”51 Similarly, in their 300-page critical review of the literature on firearms and violence, the National Research Council of the National Academy of Sciences observes, “One theme that runs throughout our report is the relative absence of credible data central to addressing even the most basic questions about firearms and violence.”52

Actuaries can provide high-quality, objective, relevant, quantitative research that can be used by our stakeholders as input for recommendations and decisions on this key societal issue. Toward that end, we propose three important avenues for future research.

Claims Analysis

The cost of gun violence directly affects the financial outcomes of life, health, disability, workers’ compensation, commercial and personal liability, and homeowners insurers, as well as American taxpayers. Actuaries should examine the frequency and severity of firearm-related claims across lines of insurance business in order to analyze insurers’ exposure to firearm risk.

Data availability and coding of firearm-related claims present significant issues. Moreover, health claims related to nonfatal GSW might be long-tailed, and claims related to follow-up procedures and treatments might not be linked to the original treatment episode. The proposed analysis is challenging. However, the Insurance Information Institute has meticulously tracked the frequency and severity of dog bite liability claims over the last 12 years.53 If insurers can track the data for dog bites, surely they can make progress on tracking firearm-related claims.

Total Health Care Cost of Treating Gunshot Wounds

Earlier in this article, we presented several different estimates of, and references about, the costs of treating GSW. Many researchers have quantified the cost of treatment in the emergency department as well as the initial inpatient hospitalization, but, as researchers point out, these costs are just the tip of the iceberg.54 The studies we cited exclude treatment costs such as physical and occupational therapy, follow-up treatment and procedures for complications, mental health care, nursing care and so on. Actuaries should follow the claims of gunshot survivors longitudinally to quantify the total health care cost of treating GSW.

Mortality Study

Hepburn and Hemenway remark, “Most striking is the paucity of individual-level studies … For example, there are no studies that follow a large cohort of individuals with known characteristics, comparing homicide victimization rates of those with a gun in the home, and those without.”55

Wintemute et al. published a related study using California handgun purchase data. In particular, they studied a cohort of 238,292 people who had purchased a handgun in California in 1991 and examined the mortality experience of the group through the end of 1996. They computed standardized mortality ratios and found that the purchase of a handgun was associated with a substantial increase in the risk of suicide by firearm, suicide by any method and female homicide.56

Actuaries should examine whether a mortality differential exists between members of gun-owning households and the general and insured population. More specifically, actuaries should examine cohorts of gun-owning households in select states, compute mortality rates by age and sex, and compare them to a standard table for the state or region.

A CALL TO ACTION FOR ACTUARIES

Actuarial input on the public health crisis of gun violence is consistent with the history and mission of our profession. The Surgeon General’s reports on smoking and health were controversial; however, this did not deter actuaries from studying the issue.57When the AIDS crisis arose in the 1980s, the SOA established a task force to study the impact of AIDS on the insurance industry. The task force produced a 300-page report.58 Among the many recommendations in the report, the task force recommended that AIDS-related claims be tracked, just as we are recommending that firearm-related claims be tracked across lines of business. Additionally, actuaries are currently studying other important and timely issues such as obesity and climate change.59,60

Beginning with the Dickey Amendment of 1996, government entities have been restricted in their ability to fund research related to firearms. Stark and Shah explain, “Although the legislation does not ban gun-related research outright, it has been described as casting a pall over the research community.” Indeed, researchers estimate that the field receives just 1.6 percent of the funding one would expect, given its impact on mortality.61 This makes the contributions of actuaries more urgent.

Actuaries have unique skills in measuring and managing risk. We are experts in mortality analysis, skilled in data analytics and model building, and we can analyze the problem objectively. As a profession, we must employ our skills and talents to help address the economic, mortality and morbidity impact of gun violence.

References:

- 1. Society of Actuaries. “The 2017–2021 Strategic Plan Development Process.” 2017–2021 Strategic Plan. Accessed June 25, 2018. https://www.soa.org/strategic-planning/default/. ↩

- 2. American Medical Association. 2016. “AMA Calls Gun Violence ‘A Public Health Crisis.’” June 14. Accessed April 13, 2018. https://www.ama-assn.org/ama-calls-gun-violence-public-health-crisis. ↩

- 3. Centers for Disease Control and Prevention, National Center for Injury Prevention and Control. 2018. “Welcome to WISQARS.” Injury Prevention & Control. May 3. Accessed February 15, 2018. www.cdc.gov/injury/wisqars. ↩

- 4. Xu, J., S. L. Murphy, K. D. Kochanek, and B. A. Bastian. 2016. “Deaths: Final Data for 2013.” National Vital Statistics Reports 64 (2). http://www.cdc.gov/nchs/data/nvsr/nvsr64/nvsr64_02.pdf. ↩

- 5. Supra note 3. ↩

- 6. Stewart, M. 2016. “Gun Deaths Are Now Outpacing Traffic Deaths in 21 States, and Counting.” HuffPost. January 15. http://www.huffingtonpost.com/entry/guns-deaths-car-deaths_us_56991b31e4b0ce4964242c47. ↩

- 7. Spitzer, S. A., K. L. Staudenmayer, L. Tennakoon, D. A. Spain, and T. G. Weiser. 2017. “Costs and Financial Burden of Initial Hospitalizations for Firearm Injuries in the United States, 2006–2014.” American Journal of Public Health 107 (5): 770–774. https://ajph.aphapublications.org/doi/10.2105/AJPH.2017.303684. ↩

- 8. Gani, F., J. V. Sakran, and J. K. Canner. 2017. “Emergency Department Visits for Firearm-related Injuries in the United States, 2006–14.” Health Affairs 36 (10): 1729–1738. https://www.healthaffairs.org/doi/10.1377/hlthaff.2017.0625. ↩

- 9. Salemi, J. L., V. Jindal, R. E. Wilson, M. F. Mogos, M. H. Aliyu, and H. M. Salihu. 2015. “Hospitalizations and Healthcare Costs Associated With Serious, Non-lethal Firearm-related Violence and Injuries in the United States, 1998–2011.” Family Medicine and Community Health 3 (2): 8–19. http://www.ingentaconnect.com/content/cscript/fmch/2015/00000003/00000002/art00003. ↩

- 10. Lee, J., S. A. Quraishi, S. Bhatnagar, R. D. Zafonte, and P. T. Masiakos. “The Economic Cost of Firearm-related Injuries in the United States From 2006 to 2010.” Surgery 155 (5): 894–898. https://www.surgjournal.com/article/S0039-6060(14)00060-9/fulltext. ↩

- 11. Livingston, D. H., R. F. Lavery, M. C. Lopreiato, D. F. Lavery, and M. R. Passannante. 2014. “Unrelenting Violence: An Analysis of 6,322 Gunshot Wound Patients at a Level I Trauma Center.” The Journal of Trauma and Acute Care Surgery 76 (1): 2–11. https://journals.lww.com/jtrauma/pages/articleviewer.aspx?year=2014&issue=01000&article=00002&type=abstract. ↩

- 12. Cook, P.J., and J. Ludwig. 2006. “The Social Costs of Gun Ownership.” Journal of Public Economics 90 (1): 379–391. https://www.sciencedirect.com/science/article/abs/pii/S0047272705000411. ↩

- 13. Peek-Asa, C., B. Butcher, and J. E. Cavanaugh. 2017. “Cost of Hospitalization for Firearm Injuries by Firearm Type, Intent and Payer in the United States.” Injury Epidemiology 4 (1). https://injepijournal.springeropen.com/articles/10.1186/s40621-017-0120-0. ↩

- 14. Lemaire, J. 2005. “The Cost of Firearm Deaths in the United States: Reduced Life Expectancies and Increased Insurance Costs.” The Journal of Risk and Insurance 72 (3): 359–374. https://onlinelibrary.wiley.com/doi/abs/10.1111/j.1539-6975.2005.00128.x. ↩

- 15. Frankel, T. C. 2018. “One Roadblock to Arming Teachers: Insurance Companies.” The Washington Post. May 26. https://www.washingtonpost.com/business/economy/one-roadblock-to-arming-teachers-insurance-companies/2018/05/26/59d6c704-5f7e-11e8-8c93-8cf33c21da8d_story.html?noredirect=on&utm_term=.ea0941514380. ↩

- 16. Chubb Group of Insurance Companies. 2013. “ForeFront Portfolio 3.0: Workplace Violence Expense Insurance.” September. Accessed April 27, 2018. http://www.chubb.com/businesses/csi/chubb13750.pdf. ↩

- 17. XL Group. 2016. “XL Catlin Unveils Workplace Violence Insurance Coverage for U.S. Businesses.” February 3. Accessed April 27, 2018. http://xlgroup.com/press/xl-catlin-unveils-workplace-violence-insurance-coverage-for-us-businesses. ↩

- 18. Great American Insurance Group. 2013. “Workplace Violence Insurance: Serious Issues, Important Coverage.” Accessed April 13, 2018. https://www.greatamericaninsurancegroup.com/docs/default-source/executive-liability/usa/2352-eld-workplace-violence-insurance-sell-sheet.pdf?sfvrsn=4. ↩

- 19. Metzner, R. 2012. “Preventing Workplace Violence.” Risk Management Monitor. November 30. http://www.riskmanagementmonitor.com/2012-a-year-of-workplace-violence. ↩

- 20. National Rifle Association. “Personal Firearms Liability Insurance.” Accessed April 14, 2018. https://mynrainsurance.com/insurance-products/liability-personal-firearms. ↩

- 21. Lockton Affinity. NRA Carry Guard. Accessed April 14, 2018. https://lockton.nracarryguard.com/. ↩

- 22. Gore, L. 2016. “Mandatory Gun Insurance Before Lawmakers in 4 States.” AL.com. February 9. http://www.al.com/news/index.ssf/2016/02/mandatory_gun_insurance_before.html. ↩

- 23. Vote Smart. “SB 424—Prohibits Insurance Increases for Gun Owners—Florida Key Vote.” Accessed August 16, 2017. http://votesmart.org/bill/17865/50390#.V7NTLj4rLEU. ↩

- 24. Hemenway, D. 2011. “Risks and Benefits of a Gun in the Home.” American Journal of Lifestyle Medicine 5 (6): 502–511. http://journals.sagepub.com/doi/abs/10.1177/1559827610396294. ↩

- 25. Hepburn, L. M., and D. Hemenway. 2004. “Firearm Availability and Homicide: A Review of the Literature.” Aggression and Violent Behavior 9 (4): 417–440. https://www.ncjrs.gov/App/publications/Abstract.aspx?id=206421. ↩

- 26. Miller, M., D. Hemenway, and D. Azrael. 2007. “State-level Homicide Victimization Rates in the U.S. in Relation to Survey Measures of Household Firearm Ownership, 2001–2003.” Social Science & Medicine 64 (3): 656–664. https://www.sciencedirect.com/science/article/pii/S0277953606004898?via%3Dihub. ↩

- 27. Stroebe, W. 2013. “Firearm Possession and Violent Death: A Critical Review.” Aggression and Violent Behavior 18 (6): 709–721. https://www.sciencedirect.com/science/article/pii/S1359178913000797. ↩

- 28. Anglemyer, A., T. Horvath, and G. Rutherford. 2014. “The Accessibility of Firearms and Risk for Suicide and Homicide Victimization Among Household Members: A Systematic Review and Meta-analysis.” Annals of Internal Medicine 160 (2): 101–110. http://annals.org/aim/fullarticle/1814426/accessibility-firearms-risk-suicide-homicide-victimization-among-household-members-systematic. ↩

- 29. Moyer, M. W. 2017. “More Guns Do Not Stop More Crimes, Evidence Shows.” Scientific American. October 1. https://www.scientificamerican.com/article/more-guns-do-not-stop-more-crimes-evidence-shows/. ↩

- 30. Supra note 4. ↩

- 31. Kalesan, B., M. D. Villarreal, K. M. Keyes, and S. Galea. 2016. “Gun Ownership and Social Gun Culture.” Injury Prevention 22 (3): 216–220. http://dx.doi.org/10.1136/injuryprev-2015-041586. ↩

- 32. Supra note 25. ↩

- 33. Tavernier, R., and J. Vadiveloo. 2017. “Firearms as an Underwriting Characteristic.” Undergraduate Student Thesis. Department of Mathematics, University of Connecticut. ↩

- 34. Vann, R.D., and Lang, M.A. (eds). 2011. Recreational Diving Fatalities. Proceedings of the Divers Alert Network 2010 April 8–10 Workshop. Durham, N.C.: Divers Alert Network. https://www.diversalertnetwork.org/files/Fatalities_Proceedings.pdf. ↩

- 35. Supra note 3. ↩

- 36. Tseng, S. H. 2004. “The Effect of Life Insurance Policy Provisions on Suicide Rates.” December 15. Accessed April 28, 2018. emptormaven.com/img/lifetseng.pdf. ↩

- 37. Supra note 33. ↩

- 38. Supra note 25. ↩

- 39. National Research Council. 2005. Firearms and Violence: A Critical Review. Washington, D. C.: The National Academies Press. https://doi.org/10.17226/10881. ↩

- 40. Smith, T. W., and J. Son. 2015. “Trends in Gun Ownership in the United States, 1972–2014.” NORC at the University of Chicago. March. Accessed April 13, 2018. http://www.norc.org/PDFs/GSS%20Reports/GSS_Trends%20in%20Gun%20Ownership_US_1972-2014.pdf. ↩

- 41. United States Census Bureau. 2017. “America’s Families and Living Arrangements: 2017.” Accessed April 13, 2018. https://www.census.gov/data/tables/2017/demo/families/cps-2017.html. ↩

- 42. Beckett, L. 2016. “Gun Inequality: U.S. Study Charts Rise of Hardcore Super Owners.” The Guardian. September 19. https://www.theguardian.com/us-news/2016/sep/19/us-gun-ownership-survey. ↩

- 43. Hill, Catey. 2012. “11 Riskiest Dog Breeds for Homeowners and Renters.” Forbes. May 30. https://www.forbes.com/sites/cateyhill/2012/05/30/11-riskiest-dog-breeds-for-homeowners-and-renters/#2df04abb36d9. ↩

- 44. Esurance. “Trampolines and Homeowners Insurance: Are You Covered?” Accessed June 8, 2018. https://www.esurance.com/info/homeowners/trampolines-and-homeowners-insurance. ↩

- 45. Loder, R. T., W. Schultz, and M. Sabatino. 2014. “Fractures From Trampolines: Results From a National Database, 2002 to 2011.” Journal of Pediatric Orthopaedics 34 (7): 683–690. https://insights.ovid.com/crossref?an=01241398-201410000-00005. ↩

- 46. American Academy of Orthopaedic Surgeons. 2017. “Orthopaedic Surgeons Warn Parents and Young Children About the Dangers of Trampolines.” July 19. Accessed April 13, 2018. http://newsroom.aaos.org/patient-resources/prevent-injuries-america/trampoline-safety.htm. ↩

- 47. Bureau of Justice Statistics. 2012. “About 1.4 Million Guns Stolen During Household Burglaries and Other Property Crimes From 2005 Through 2010.” Office of Justice Programs. November 8. Accessed April 13, 2018. https://www.bjs.gov/content/pub/press/fshbopc0510pr.cfm. ↩

- 48. Hemenway, D., D. Azrael, and M. Miller. 2017. “Whose Guns Are Stolen? The Epidemiology of Gun Theft Victims.” Injury Epidemiology 4 (1). https://injepijournal.springeropen.com/articles/10.1186/s40621-017-0109-8. ↩

- 49. Mitchell, R. W. 2001. “Columbine Settlement Rattles Insurer Groups.” National Underwriter 105 (19): 18. ↩

- 50. Altimari, D. 2015. “Sandy Hook Families Settle Lawsuits Against Lanza Estate for $1.5M.” Hartford Courant. August 6. Accessed April 13, 2018. http://www.courant.com/news/connecticut/hc-sandy-hook-lawsuit-settled-20150803-story.html. ↩

- 51. Webster, D. W., M. Cerdá, G. J. Wintemute, and P. J. Cook. 2016. “Epidemiologic Evidence to Guide the Understanding and Prevention of Gun Violence.” Epidemiologic Reviews 38 (1): 1–4. https://academic.oup.com/epirev/article/38/1/1/2754874. ↩

- 52. Supra note 39. ↩

- 53. Insurance Information Institute. 2017. “Spotlight on: Dog Bite Liability.” April 3. https://www.iii.org/issue-update/dog-bite-liability. ↩

- 54. Bansal, D. G. 2017. “Initial Hospital Costs for Gunshot Wounds Just ‘Tip of the Iceberg.’” Stanford Medicine News Center. March 21. Accessed April 14, 2018. http://med.stanford.edu/news/all-news/2017/03/initial-hospital-costs-from-gunshot-wounds-total-6-billion-over-nine-years.html. ↩

- 55. Supra note 25. ↩

- 56. Wintemute, G. J., C. A. Parham, J. J. Beaumont, M. Wright, and C. Drake. 1999. “Mortality Among Recent Purchasers of Handguns.” The New England Journal of Medicine 341 (21): 1583–1589. https://www.nejm.org/doi/full/10.1056/NEJM199911183412106. ↩

- 57. Cowell, M. J., and B. L. Hirst. 1980. “Mortality Differences Between Smokers and Nonsmokers.” Transactions of the Society of Actuaries 32: 185–213. https://www.soa.org/Library/Research/Transactions-Of-Society-Of-Actuaries/1980/January/tsa80v328.aspx. ↩

- 58. Society of Actuaries AIDS Task Force. 1988. “The Impact of AIDS on Life and Health Insurance Companies: A Guide for Practicing Actuaries.” Transactions of the Society of Actuaries 40 (2): 839–1159. https://www.soa.org/library/tsa/1980-89/TSA88V40PT25.pdf. ↩

- 59. Behan, D. F., and S.H. Cox. 2010. “Obesity and Its Relation to Mortality and Morbidity Costs.” Society of Actuaries. December. Accessed April 14, 2018. https://www.soa.org/research-reports/2011/research-obesity-relation-mortality/. ↩

- 60. Actuaries Climate Index. Accessed April 14, 2018. http://actuariesclimateindex.org/home/. ↩

- 61. Stark, D. E., and N. H. Shah. 2017. “Funding and Publication of Research on Gun Violence and Other Leading Causes of Death.” Journal of the American Medical Association 317 (1): 84–85. https://jamanetwork.com/journals/jama/fullarticle/2595514. ↩