Force of Nature

Why and how to include climate change in the risk management framework

June/July 2019The boards of directors for many corporations received an alarming and surprising note in their quarterly management update reports: California’s largest utility and one of the United States’ largest investor-owned electric utilities, Pacific Gas and Electric (PG&E), was filing for bankruptcy. Many companies have financial exposures to PG&E through investments, accounts receivable or secondary exposure, and the risk analysis would include credit analysis and scenario testing to measure potential exposures. For such a large and stable organization to declare bankruptcy would shock many. However, a January 2019 headline in The Washington Post summarized the story well: “Pacific Gas and Electric is a company that was just bankrupted by climate change. It won’t be the last.”

Risk management related to climate change can broadly be broken down into two categories:

- Disclosure

- Managing financial impacts from climate change

Disclosure is a powerful tool to evaluate how a corporation assesses, prices and manages climate-related risks. Most companies are focusing on disclosure now, as it is the key to address investor and customer awareness, and demand for more information related to the impacts of climate change.

While the full financial risks from climate change may crystallize over longer time horizons, they are becoming ever more apparent. Global insured losses from natural disaster events in 2017 were the highest ever recorded.1 The financial impact from climate change is not unique to the property and casualty (P&C) insurance industry—it potentially can affect all financial institutions on the asset side.

Insurance companies, pension funds, banks, asset management and other financial institutions are all involved with a wide range of financing and investment activities. These activities span across many sectors of the economy, including those that are carbon intensive, making these investment assets susceptible to climate-related risks. The physical impacts of climate change pose a direct risk to the insurance company or pension fund’s own operations. Climate change also poses indirect risk to the insurance company or pension fund’s assets as we transition to a low-carbon economy, which can lead to a combination of higher credit risk from potential asset impairment/write down (e.g., reduced repayment capacity or credit downgrade) and higher market risk (e.g., depreciation of company or security valuations or reduced value of collateral). Assets in real estate, infrastructure, agricultural and brown energy businesses are particularly at risk. Potential financial impacts could also stem from reputational risk as a result of negative publicity as well as regulatory fines.

To maintain financial health and protect the interests of policyholders and shareholders, companies must assess their exposure and maintain a high degree of resilience to climate-related risks.

This article focuses on insurance companies and pension funds, although many of the concepts also apply to financial institutions in general. It does not intend to address specific insurance risks as a result of climate-related events stemming from P&C insurance coverage or pandemic risks. The discussion focuses on the general concepts of how climate change can impact insurance companies and pension funds, in particular on the asset side.

Climate Change Background

Climate change refers to changes in weather severity, weather patterns, heating/cooling of the planet, migration of species and vector-borne illnesses. Sustainability risk is another term generally used in a broader sense that can also include societal aspects such as reducing poverty, increasing diversity and equality, and so on. See Figure 1 for more details.

Figure 1: Climate Change Versus Sustainability Risk and Everything in Between

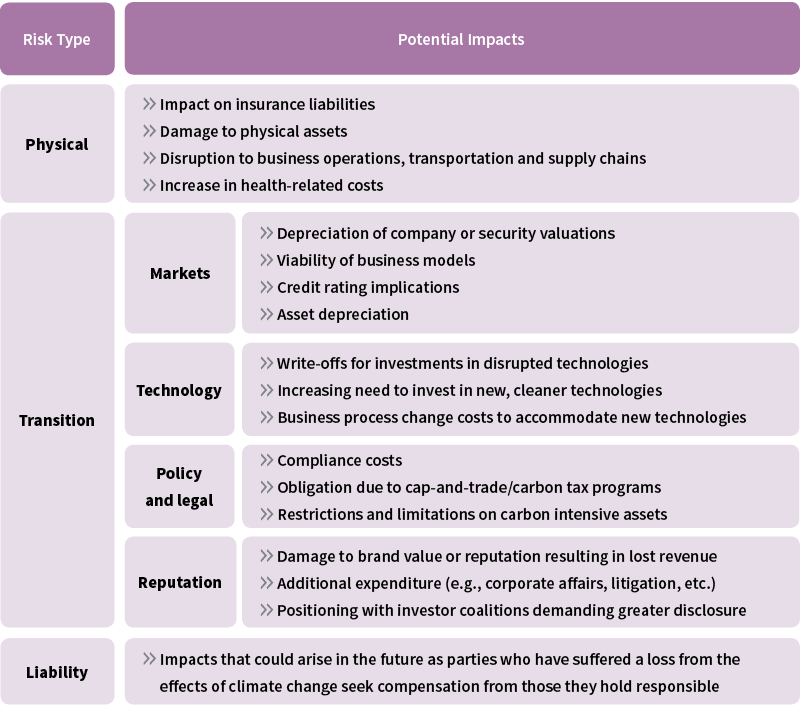

Financial risks from climate change arise through two primary channels or “risk factors”: physical and transition (see Figure 2). These factors manifest, for example, as increasing underwriting, reserving, credit or market risk for firms.

Figure 2: Details on Climate Change Risk Types

Physical risks from climate change can be related to specific weather events (such as heat waves, floods, wildfires and storms) and longer-term shifts in climate (such as changes in precipitation and extreme weather variability, rising sea levels and rising mean temperatures).

Physical risk is generally better understood compared to transition risk. Transition risks can arise from the process of adjustment toward a low-carbon economy. This adjustment is influenced by a range of factors, including:

- Climate-related developments in policy and regulation

- The emergence of disruptive technology or business models

- Shifting sentiment and societal preferences

- Evolving evidence, frameworks and legal interpretations

This could prompt a reassessment of the value of a large range of assets and create credit exposures for banks and other lenders as costs and opportunities become apparent.

Climate change also has a third risk that is not a focus of this article: liability. Liability risk2 is related to the important question: “If future generations suffer from severe climate change, who will they hold responsible?”

Climate-related Disclosure

Investor, regulatory and stakeholder expectations continue to evolve around climate change risk management. For climate change risk, disclosure is the key. Although carbon emission and climate-related disclosures began in early 2000 among some corporations, they were initially considered a “nice-to-have.” The focus when the disclosure of these risks started was to mitigate potential climate-related reputational risk.

One of the major milestones for climate change disclosure occurred in December 2015, when the Financial Stability Board (FSB) established the Task Force on Climate-related Financial Disclosures (TCFD) to develop voluntary, consistent climate-related financial risk disclosures for companies to use when providing information to investors, lenders, insurers and other stakeholders. The TCFD recommendations released in June 2017 focused on enhancing market transparency and enabling the efficient allocation of capital in the transition to a low-carbon economy as envisioned by the Paris Climate Agreement. More than 580 organizations are supporting the TCFD as of February 2019, with new supporters being added on a continuous basis.

Mandatory greenhouse gas (GHG) reporting, also known as mandatory carbon reporting, is the law in 40 countries across the world, including the United Kingdom, many EU member states, Canada, the United States, Mexico, Australia, Japan and South Africa (as of 2018). In the United Kingdom, publicly listed companies are required to account for their GHG emissions as part of their annual financial reporting, while EU GHG reporting is included within nonfinancial reporting. However, the GHG reporting qualification varies across jurisdictions.

Examples of the global landscape of climate and sustainability reporting and disclosure are shown in Figure 3, and the list is expanding fast.

Figure 3: Stakeholder Expectations and Requirements for Climate and Sustainability Reporting and Disclosure

Regulatory Requirements to Manage Financial Impacts From Climate Change

The requirements of managing climate-related risks are evolving rapidly, with increasing expectations from regulators that insurance companies have a strategy for the management of the financial risks associated with climate change.

In the United States, the California insurance commissioner released the results of a new analysis of the climate risk exposure faced by investments held by the insurance industry. The California Department of Insurance is the first financial regulator to undertake an analysis of both climate-related physical risks and transition risks faced by insurers’ assets.

In the United Kingdom, the Prudential Regulatory Authority recently released a consultation paper on climate change risk on four main areas: governance, risk management, scenario analysis and disclosure.

In Canada, the Canadian Securities Administrators (CSA) is developing guidance and considering new disclosure requirements relating to climate-related risks, and the Office of the Superintendent of Financial Institutions (OSFI) expects insurers to develop a strategy for managing climate change risk.

In summary, with increasing focus from stakeholders and regulators on formalizing requirements for disclosures and the measurement of climate change, the insurance industry and pension funds should review their current practices and consider adopting a more holistic approach, incorporating climate-related risk into their risk management frameworks.

Determining Level of Exposure

The velocity of change and potential exposure magnitude should be considered in addition to each company’s specific system of risk management in addressing climate-related risk. The scientific community continues to point to growing evidence of the likelihood and severity of significant warming of the planet. The Actuaries Climate Index—sponsored by the Society of Actuaries (SOA), Canadian Institute of Actuaries (CIA), Casualty Actuarial Society (CAS) and the American Academy of Actuaries (the Academy)—is an indicator of the frequency of extreme weather and the extent of sea level change in the United States and Canada. It shows the five-year moving average of climate extremes and sea level across the United States and Canada reached a new high with data released for winter 2017–2018. Increasing values in the index point to increased occurrences of extreme climate events.

Climate change risk is no longer something on the horizon—it is arriving. Failure to properly plan for and react to climate change could lead to more incidents similar to the PG&E event. There is a real urgency to address climate-related risk within a company’s risk framework.

To effectively manage climate change risk, a company needs to establish a holistic view of how climate-related events may have impacts across the enterprise (e.g., by business segment, product line, investment portfolio, geography, local regulatory requirements, risk type, etc.) and identify plausible mitigation actions. This also facilitates the development of appropriate climate change stress scenarios for scenario analysis that can be used to assess a company’s resilience and vulnerabilities to potential climate change events.

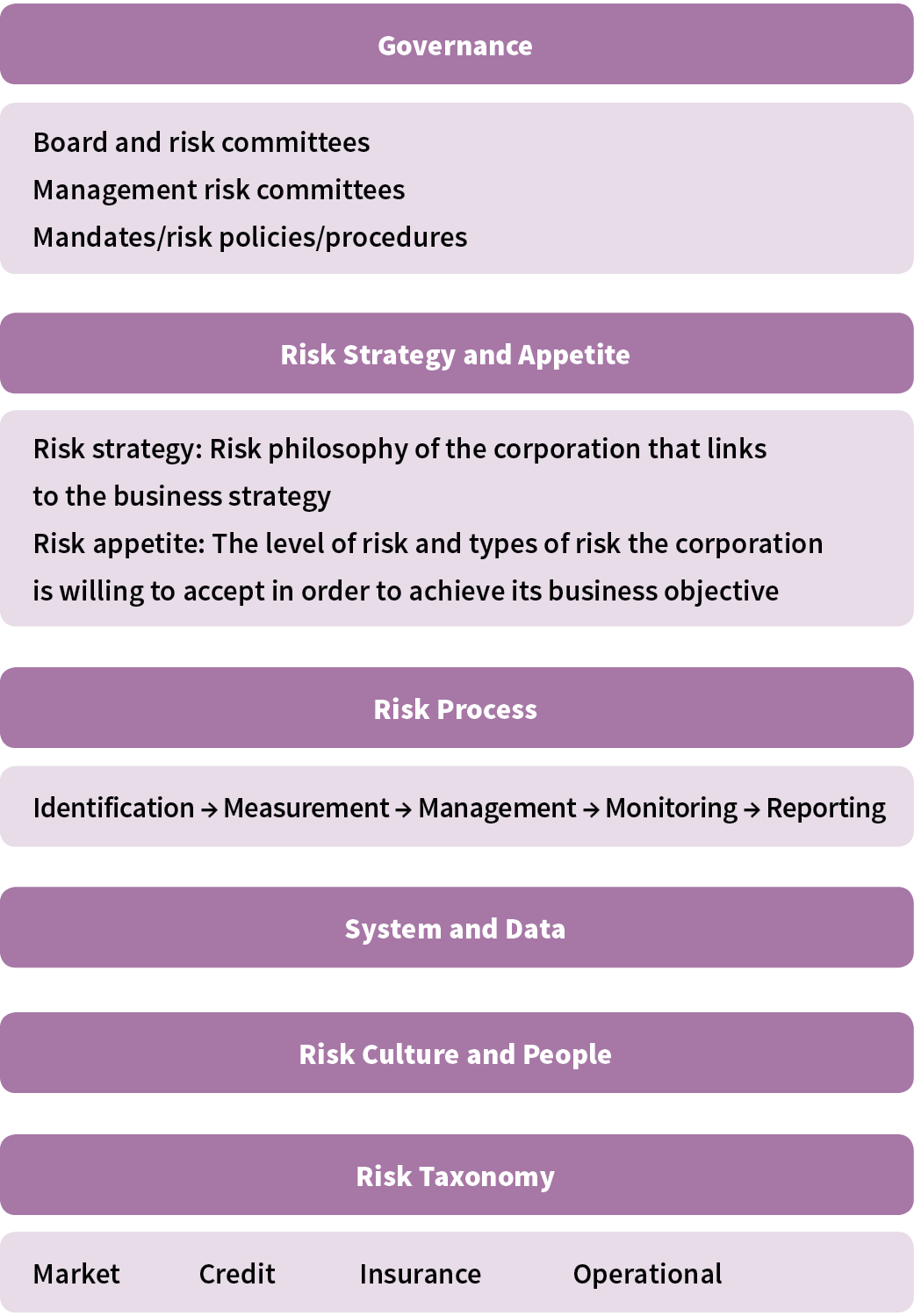

Effective management of climate change risks requires integration across all elements in the risk management framework, tailored to an individual company’s system of risk management (see Figure 4).

Figure 4: Example of a Risk Management Framework

Integrating Climate Change Into a Risk Management Framework

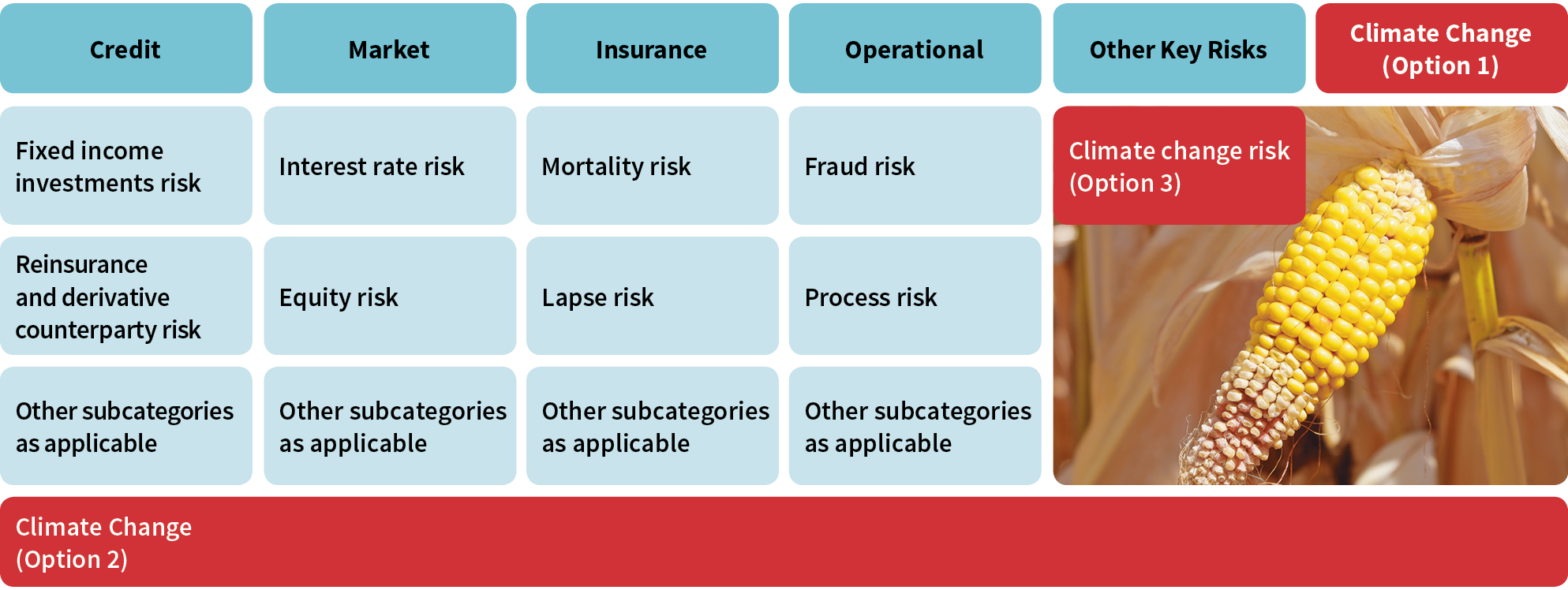

Climate change can be integrated into a risk management framework in three ways. These potential routes mainly focus on climate change, but they could be extended for the broader sustainability risk:

- Option 1. Recognize climate change risk is a key risk similar to insurance, market and credit risks.

- Option 2. Recognize climate change affects financial risks as well as nonfinancial risks such as operational risk.

- Option 3. Recognize climate change could fit into a company’s risk management framework as a new sub-risk category under an existing key risk category.

See Figure 5 for a visual representation of these three options.

Figure 5: Three Options to Integrate Climate Change Into a Company’s Risk Universe

Option 1: Climate Change Risk as a Stand-alone and Separate Key Risk

For companies with a relatively mature risk management framework, this is a fairly straightforward approach to leverage the existing infrastructure already in place for financial and other key risks. It involves establishing appropriate policies and standards, as well as risk appetite and limits associated with climate change risk. One of the biggest benefits of this approach is that there will be clear governance as well as roles and responsibilities associated with the management of climate change risk.

On the other hand, climate change itself is less likely to cause direct financial losses for insurance companies or pension funds. Rather, it is more likely to be experienced through interactions with other key risks. This could create challenges in establishing and implementing a specific risk identification related to climate change and an identification, measurement, management, monitoring and reporting (IMMMR) process. It also may not be the best approach for identifying potential impacts to the other risk types within the existing risk processes.

Option 2: Climate Change Risk Embedded Within Existing Risks

This option addresses and embeds climate change risk within the existing risk processes, reflecting the close interaction among climate risk and existing key risk types (e.g., credit, market, insurance, operational and reputational risk). Under this option, a company can establish credit limits associated with any carbon-intensive industries or minimize investing assets in real estate located in areas exposed to rising sea levels for a given asset portfolio. The monitoring and reporting of such limits also can become part of the existing risk processes.

However, this approach could potentially mean a very large number of existing processes or procedures will need to be updated or enhanced to reflect the inclusion of climate-related risk. The governance and monitoring of the climate-related risks also could become fragmented, and it could become challenging to maintain consistency between the risk limits and the overall risk appetite and strategy around climate change risk.

Option 3: Climate Change Risk Embedded Within an Existing Risk Type

For companies with a relatively lower material or a narrower potential exposure to climate-related risks, it might be sufficient and more efficient to address the risk by creating a new subcategory under existing key risks. Strategic risks, insurance risks and operational risks could be some of the potential options. This is probably the least “onerous” option compared to the other two options. However, there could be the potential limitation of the comprehensiveness and lack of clarity on the definition of the risk itself, as well as the effectiveness of the underlying risk processes.

Final Considerations—Efficiency and Optimization

Financial institutions are undergoing major disruption. Insurance business models have been relatively insulated, but the pace of change is accelerating and not expected to slow down. Advanced technology, data and digital capabilities are growing exponentially, driving lower costs and enhancing customer experiences. But at the same time, nonfinancial risks stemming from the pace of change, use of emerging technology, agile business practices and increasing reliance on suppliers are also growing. The overall universe of emerging risks is expanding (e.g., cyber, technology, supplier, fraud), and regulatory requirements continue to grow around conduct risk, privacy legislation, customer-focused outcomes and so on.

These risks have similar characteristics to climate change risk and bring similar challenges to a corporation. In developing its risk management framework for climate-related risk, each corporation also should consider how it can effectively incorporate new risks, evolving risks and new regulatory requirements in a broader sense. The adopted approach should be a balance of offering offensive capability while ensuring increased alignment with the business’ strategy to aid in better decision-making and create more value.

References:

- 1. Bevere, Lucia, Marla Schwartz Pourrabbani, and Rajeev Sharan. Sigma 1/2018: Natural Catastrophes and Man-made Disasters in 2017: A Year of Record-breaking Losses. Swiss Re Institute, April 11, 2018, (accessed April 5, 2019). ↩

- 2. An example of liability risk is when investors back a business that goes on to suffer a loss due to climate-related events. There may then be a question as to whether the business had provided enough information about its exposure to these climate-related financial risks. If investors feel this information had not been provided, they might make a claim against the business. Liability cases could also include people who have suffered from physical events, such as flooding, making claims against companies they argue are, at least in part, responsible. ↩

Copyright © 2019 by the Society of Actuaries, Chicago, Illinois.