HDHL Medical Insurance in China: Part 1

Deep insights into one of the most popular and essential products in the commercial medical insurance market

August 2021The hottest topics in the commercial medical insurance market in China right now are high-deductible, high-limit medical reimbursement insurance plans (HDHL, or 百万医疗 in Chinese) and region-customized social health insurance (SHI) supplemental medical insurance plans (known as Hui Min Bao).

One HDHL medical insurance product launched in 2016 rapidly ignited the entire insurance industry’s excitement for medical products with high deductibles, high annual limits and cheap premium rates. Rough estimates for this HDHL medical product indicate there were approximately 140 million policies issued within five years. Although a similar medical product (Taikang Life Ru Yi Zun Xiang medical product) entered the market in 2010, it did not generate much attention or gain recognition from insurance companies. During that period of time, the public was slowly starting to grasp what insurance was, and the major insurance product lines were focused on savings products.

So, the singular medical product from Taikang Life in 2010 that simply reimbursed hospital costs was not noticed. But the HDHL plan made a strong comeback to the market in 2016 when both agency and internet channels were growing rapidly as regulators emphasized that insurance products should focus on the protection attribute. Since then, HDHL plans have become one of the most popular and essential products in the market.

In 2020, the region-customized SHI supplemental medical insurance plans known as Hui Min Bao were also entering the market through close collaboration with local governments. Hui Min Bao were considered either as a continuation of HDHL plans or as supplemental coverage for the Critical Illness Insurance Scheme (CII) under the SHI coverage system. The market has not yet reached a final agreement on what role Hui Min Bao will ultimately play in the commercial medical insurance market, but, essentially, the HDHL plans aim to solve the basic poverty problem that results from expensive medical bills while the goal of Hui Min Bao is to strengthen medical coverage beyond the current basic SHI coverage. These two types of medical products also both fulfill the core institutional principle from the latest health care reform of constructing a multitiered medical coverage system.

Figure 1 demonstrates the different coverage levels and priorities among the basic SHI program and government supplementary programs (e.g., CII, Hui Min Bao and HDHL plans, which are also known as mid-end medex insurance in China). The current basic coverage from SHI and CII is not sufficient to cover the majority of high medical costs, which is also the main reason for long-lasting poverty due to high out-of-pocket costs after basic coverage runs out. Although Hui Min Bao can improve the overall medical coverage level to a certain extent, patients will still suffer when the total costs are high due to the high out-of-pocket percentage they will owe. Conversely, while the HDHL plans barely contribute anything in the low-cost range, they could provide 100 percent coverage on the high-cost side.

Figure 1: Insurance Coverage by Program

Data source: The base data combined SHI data from several cities and some group medical coverage from employee benefits packages and used the average benefit coverage from each program for simple modeling and demonstration purposes.

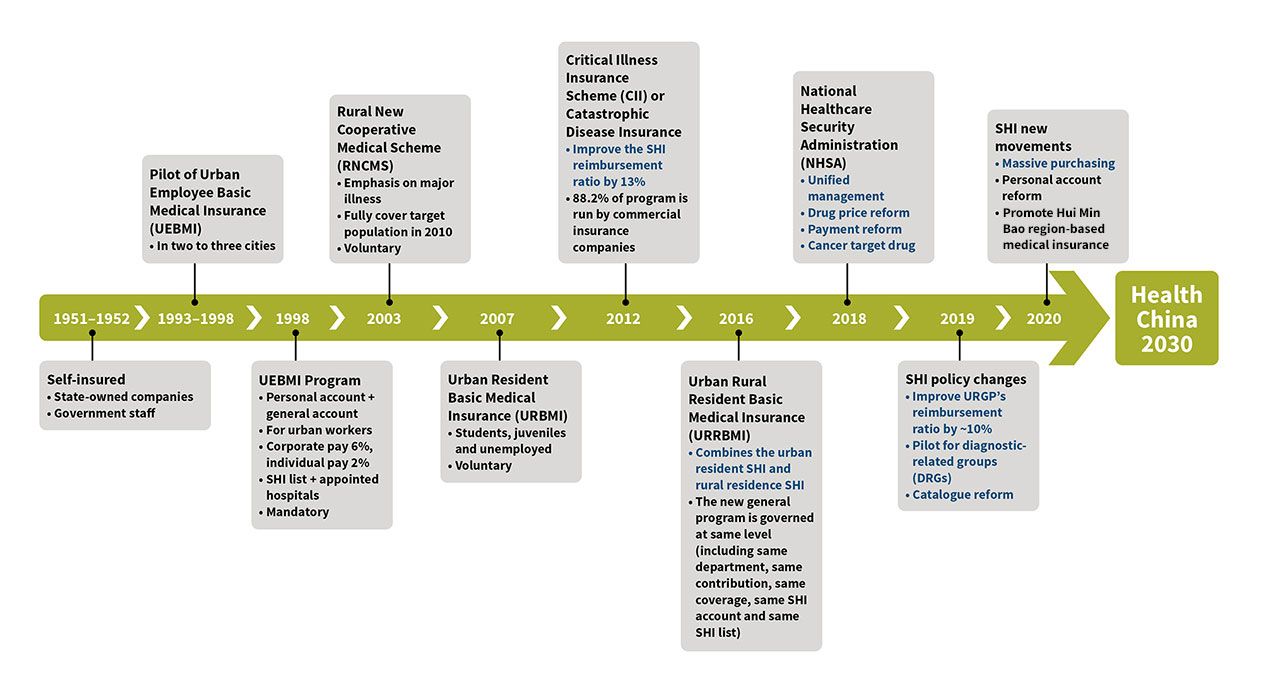

The Chinese government was busy promoting health care reform while the commercial medical insurance market was booming. The most crucial reform was the SHI revamp, particularly since the formation of the National Healthcare Security Administration (NHSA) in 2018. Any SHI reform action always attracts attention from other industries, which in turn gives the insurance industry more confidence to focus on medical coverage. See Figure 2 for an overview of the evolution of SHI programs in China.

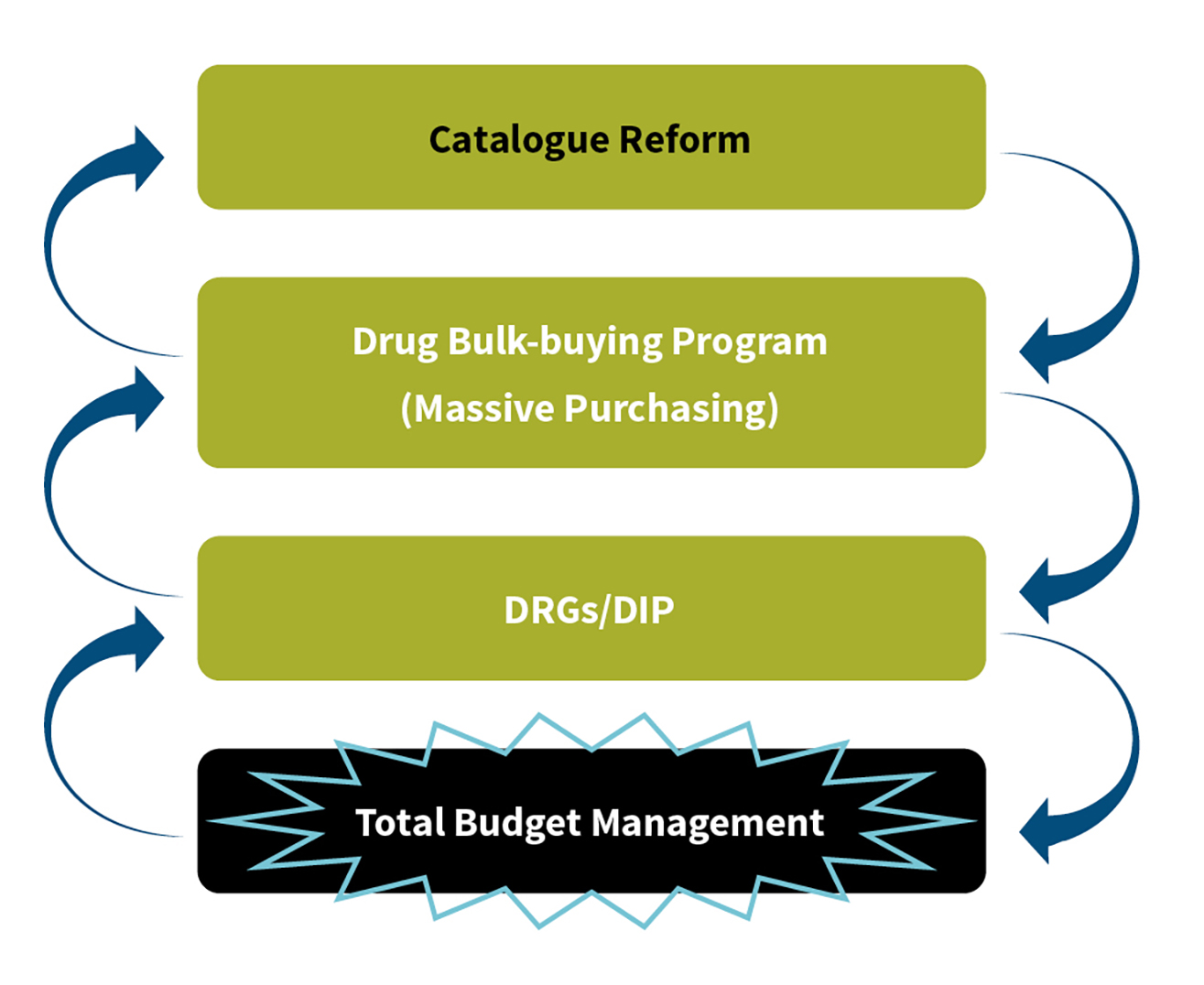

The health care reform that had the greatest impact on commercial medical insurance was the SHI payment reform, which included SHI catalogue reform, massive purchasing, diagnosis-related groups (DRGs)/diagnosis intervention packet (DIP) and total budget management. These four major programs are closely connected and dependent upon one another (see Figure 3). In February 2020, the State Council released the “Opinions of the CPC Central Committee and the State Council on Deepening the Reform of Medical Insurance System,” which aims to centralize the SHI catalogue management power to NHSA instead of local governments. This action will not only help control the SHI fund outflow, but it also will set the foundation for the massive purchasing program the NHSA has promoted in recent years.

The central government typically constructed a set of standard catalogue guidelines for local governments, so they could customize their local catalogues based on their own SHI funding balance and medicine availability. Among the medicines listed in the local catalogue, there were some so-called “magic drugs” that used a large amount of SHI funding and were less effective than expected, which eventually resulted in huge amounts of SHI funding waste. The recent massive purchasing program helped solve this magic drug waste problem. Meanwhile, the negotiations NHSA initiated with pharmaceutical companies showed that the government’s bargaining power had largely improved while the wholesale price for both drugs and material/supplies dramatically dropped (with price reductions of more than 90 percent in some cases). These results will release patients from payment pressure and ease the SHI funding pressure.

The launch of catalogue management and the massive purchasing program have created a feasible environment and foundation for initiating the DRGs program. The fundamental principle for DRGs is to formulate a stable and statistically significant system by disease category and establish the medical cost control targets. If the SHI catalogue greatly differs among hospitals, the implementation of DRGs would be challenging.

The most successful payment reform program is the total budget management program. Each hospital follows its annual total budget to manage the total SHI reimbursement threshold and effectively stabilize the SHI funding outflow. Although some unnecessary medical behaviors still occurred under the total budget management program, this program is considered the last line of defense for SHI payment, while the other three programs should be treated as refined management programs that can indirectly save a portion of the claim amount for HDHL plans.

Overview of HDHL in China

Health insurance in China mainly consists of critical illness insurance and medical insurance. Commercial health insurance gross premium has grown more than 30 percent annually in recent years, and its role in commercial life insurance1 also has grown substantially. In 2020, the overall premium of commercial health insurance in China was more than 817.3 billion CNY—about 25 percent of commercial life insurance. According to the official outlook, it will achieve 2 trillion CNY in 2025 (see Figure 4).

Figure 4: Market Overview for Commercial Health Insurance in China

Data source: Data from China Banking and Insurance Regulatory Commission (CBIRC)

In the Chinese market, critical illness insurance is 60 percent of commercial health insurance premiums, and medical insurance premiums are 35 percent. In recent years, HDHL has become the most significant part of commercial medical insurance growth. In China, HDHL represents a kind of medical reimbursement plan, usually covering inpatient hospitalization, outpatient surgery, outpatient visits before and after inpatient hospitalization, and special outpatient procedures (e.g., cancer treatment, renal dialysis and preventing rejection after organ transplant). Industry data reveals that HDHL premium achieved 50 percent growth in 2020—and in some companies, HDHL premium doubled in 2020. To a certain extent, COVID-19 played a great role in the rapid premium growth last year, much as SARS did in 2003.

Premium volume for HDHL in 2019 was 12 percent of the premium volume of the commercial medical insurance market, and some estimates say it grew to 16 percent in 2020. Life insurance companies are the largest market participants in HDHL, contributing 47 percent of premium volume, whereas health insurance companies contribute 28 percent and property and casualty (P&C) insurance companies contribute the remaining 25 percent (see Figure 5).

Figure 5: Mid-end Medex Market Share in 2020

Hover Over Image for Specific Data

Data source: Industry research

Industry Experience of HDHL

Analysis of HDHL Persistency

The majority of HDHL contracts are short term and sold by the agency channel, internet platform channel and the P&C company’s own channel. In practice, some HDHL contracts are bundled, and the rest are sold as stand-alone contracts. Some companies with an internet platform channel have developed an HDHL contract with monthly payments where the first policy month is “free” as a promotion. Under this scheme, the persistency ratio differs greatly from other customer acquisition methods. As an old cliché puts it: Easy come, easy go.

Generally, customer acquisition via the agency channel is complicated, especially when it is a bundle sale. It takes more effort since the products with high premiums should be purchased together. Conversely, customer acquisition through the internet platform is a piece of cake—especially when the premium in the first policy month is 0 or 3 CNY. This kind of design makes the product much more attractive.

As seen in Figure 6, the product with a high customer acquisition cost shows a high persistency ratio. For example, the persistency ratio is 95 percent for the agency channel and products sold through bundles. Removing the bundle sale component drops the persistency ratio to 85 percent. When moving to the internet platform channel, the ratio drops to 70 percent. In the extreme occasion when the premium in the first policy month is 0 or 3 CNY, the persistency ratio is no more than 40 percent.

Figure 6: HDHL Persistency Ratio

Data source: Experience analysis of several HDHLs in the Chinese market

Another takeaway from Figure 6 is that as the persistency ratio changes with the age band, it shows a similar M-shaped curve for all channels. One of the reasons for this is that the HDHL premium rate curve is a U shape. The premium rate increase starting at age 15 has a negative effect on the insured in this age band. Other reasons are due to the product acceptance difference and the price sensitivity difference between insureds in different age bands. Take the internet platform channel product as an example: The majority of customers are attracted to less expensive premiums over their protection needs when purchasing HDHL insurance. If after one year they realize they have not made any claims, they are not likely to renew the policy the following year. Also, there is steep product competition on the internet platform, so customers are easily attracted to more advanced and less expensive products, which results in early product lapse.

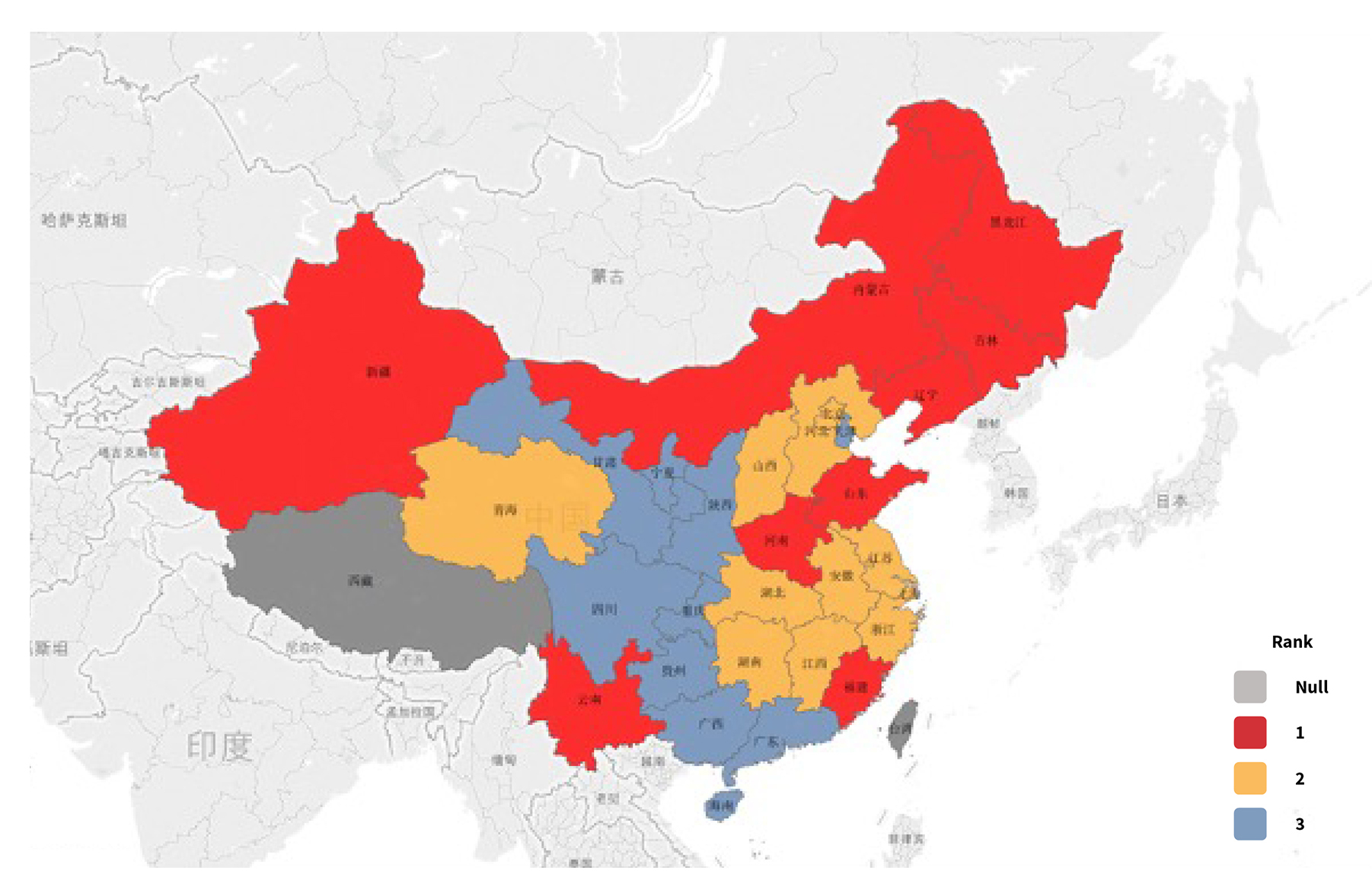

Risk Map of HDHL

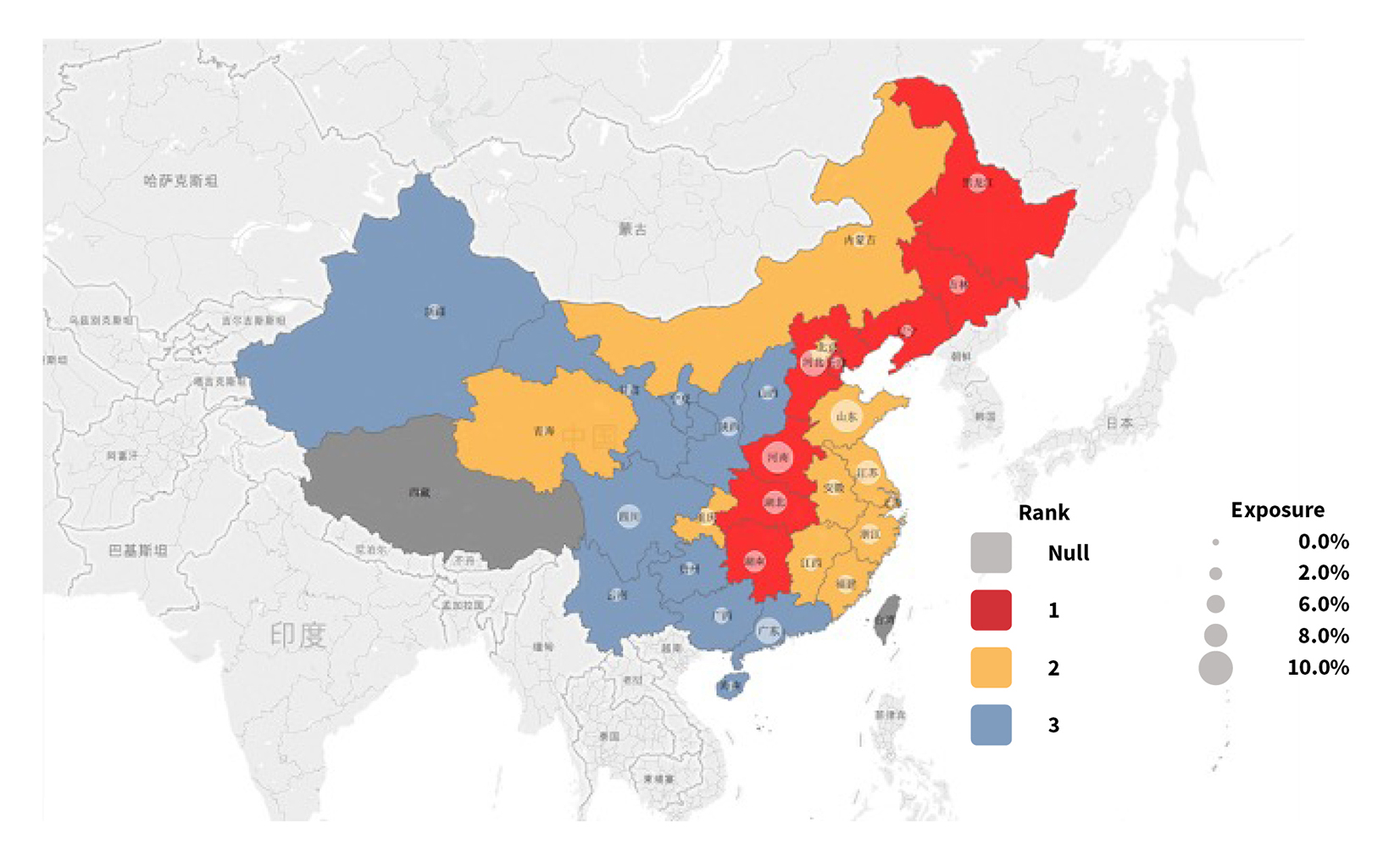

Risk in HDHL varies across different geographic regions per industry data and statistics. As shown in Figure 7, northeast China and central China are areas of high HDHL risk, southeast coastal China has medium HDHL risk and northwest island China has low HDHL risk.

Data source: Experience analysis of several HDHLs in the Chinese market

HDHL primarily takes the tail risk of medical expenses, which means HDHL claims proportion of total medical expenses increases as total medical expenses increase. Based on this fact, possible reasons to explain the pattern shown in the Figure 7 risk map are differences in average age, social health insurance program (SHIP) coverage, disease spectrum and local or non-local medical treatments.

Difference in Average Age

Most HDHL products are confronted with premium deficiency as people age. As the average age of insureds increases, the loss ratio goes up by observing HDHL actual experience among different companies. In practice, HDHL’s age portfolio appears to be slightly different among different sales schemes in the agency channel, but this kind of age difference is too limited to explain the regional risk discrepancy.

Difference in SHIP Coverage

The top-level design of SHIP in China is pay-as-you-go, which means SHIP expenditures depend on the amount of premium income that comes in. SHIP income in an economically developed region is higher than in a developing region, and expenditures in developed regions are lower due to the fact that the population is young. Thus, the SHIP foundation in developed regions has a surplus of income and the capability to afford wider coverage as a result. Based on this fact, HDHL claim costs should be much lower in an economically developed region since HDHL is a supplement to SHIP, and its premium rate is the same across China.

Take the northeast region in Figure 7 as an example: Its economy is still under development compared to the southeast coastal region, and its population is older. Therefore, the SHIP foundation in the northeast region has a lower income but higher expenditures when compared to the southeast coastal region, resulting in relatively limited SHIP coverage.

Figure 8 summarizes the inpatient medical expense amount per visit and SHIP reimbursement ratio by risk region between urban worker SHIP and rural resident SHIP. The highest inpatient cost per visit does not occur in a high-risk region, but rather in a medium-risk region since the inpatient cost per visit is also positively correlated to the region’s economic development level. Inpatient cost per visit in a medium-risk region is highest because of the advanced economic development and coastal area location. However, considering its relatively average SHIP coverage, the coastal region becomes the medium-risk region in the HDHL risk map. Looking back to the northeast region (also the high-risk region), even though inpatient cost per visit is not overly high, it is still considered the high-risk region in the HDHL risk map due to the low SHIP coverage.

Figure 8: Coverage Comparison Between Two SHIPs

| Risk Region | Urban Worker SHIP | Rural Resident SHIP | ||

| Reimbursement Ratio % | Inpatient Medical Expense per Visit | Reimbursement Ratio % | Inpatient Medical Expense per Visit | |

| High | 70.30% | 10,200 | 56.20% | 7,113 |

| Middle | 73.60% | 12,095 | 57.80% | 9,222 |

| Low | 73.60% | 10,035 | 55.50% | 6,687 |

| Average | 72.70% | 10,809 | 54.50% | 7,696 |

Data source: National Healthcare Security Administration (NHSA) public data

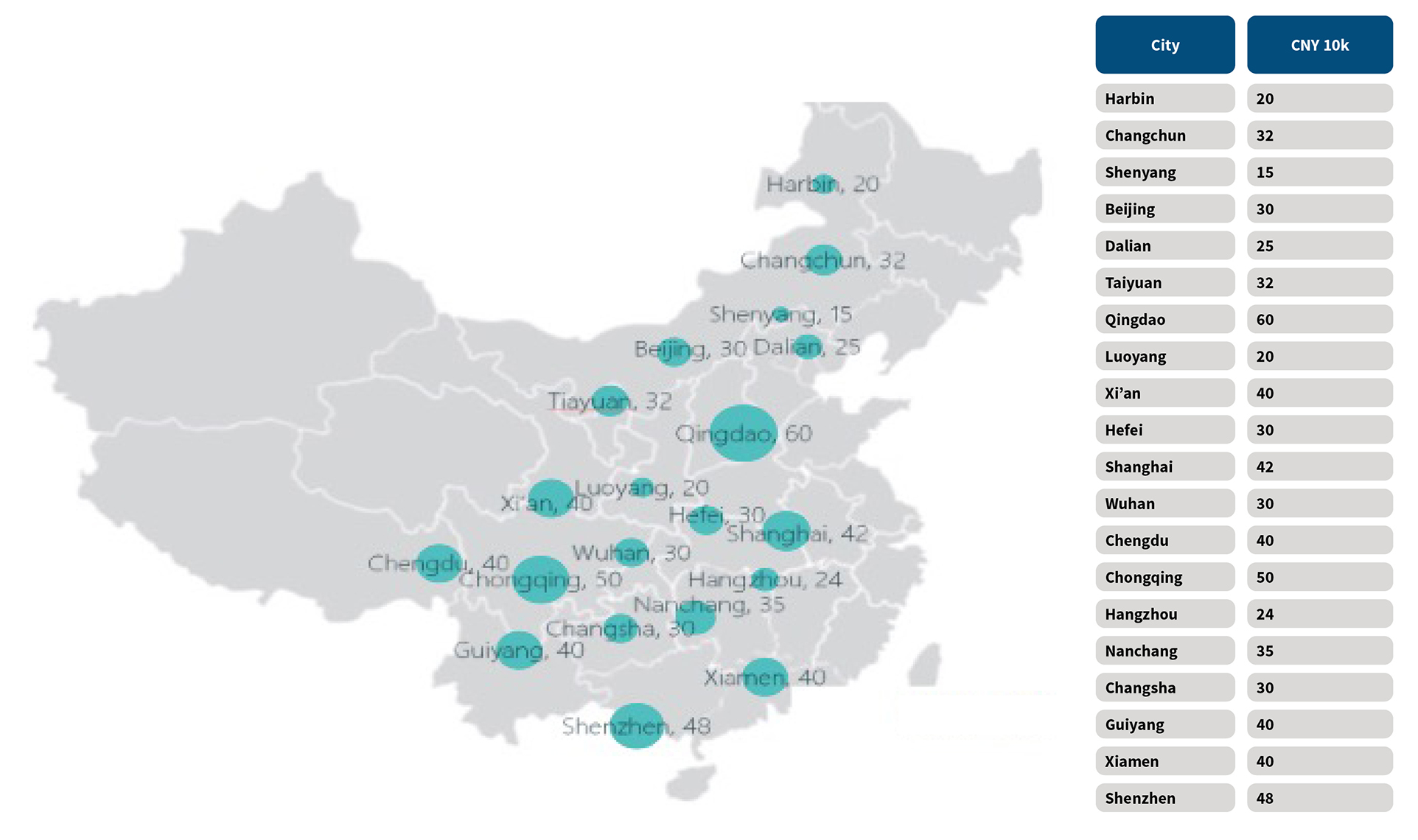

There is no significant difference in the reimbursement ratio among the different risk regions. Considering the tail risk HDHL covers, limiting the SHIP reimbursement amount is likely to be a key factor in determining the level of HDHL risk in a region. The regional annual cap of SHIP inpatient reimbursement is listed in Figure 9. The larger the circle, the higher the cap. The cap of SHIP reimbursement appears to be low in the high-risk region, proving the fact that the SHIP reimbursement has an impact on HDHL risk.

Figure 9: Annual Limits of Urban Worker SHIP for Inpatient Treatment in Key Cities, 2017

Data source: Regional National Healthcare Security Administration (NHSA) public data

Difference in Disease Spectrum

Due to the large size of the country, disease prevalence varies by region. When considering one HDHL product’s premium rate applied to a different region, the disease spectrum’s regional difference is noteworthy since it has a great influence on the regional loss ratio. Statistically, critical illness is about 30 percent of HDHL claim cause, and that percentage is even greater in some extreme products. From the disease spectrum map shown in Figure 10, its distribution is nearly the same as the HDHL risk map—this explains the HDHL risk regional distribution to some degree.

Data source: Experience analysis of several critical illness products in the Chinese market

Difference in Local or Non-local Medical Treatments

SHIP in China encourages individuals to get their medical treatment locally, and the SHIP reimbursement ratio for non-local medical treatments is reduced between 5 percent and 10 percent compared to local treatments. Additionally, the medical expense for non-local medical treatments is normally 60 percent higher than local treatment. Thus, non-local medical treatments have a negative effect on the HDHL loss ratio.

The first driving factor for receiving non-local medical treatment is that the best medical resources are centralized in big cities, such as Beijing. Big cities’ siphonic effect on medical treatments is observed, which means patients in small cities around these big cities—especially patients diagnosed with a critical disease—tend to receive superior but non-local medical treatments in surrounding big cities.

The second driving factor is medical accessibility. The incidence of non-local medical treatments has a positive relation with convenient transportation. For example, patients living in Tianjin, a 30-minute high-speed train ride from Beijing, are more likely to get medical treatment in Beijing. Conversely, patients living in the northwest and southwest regions usually choose to get treatment at the local hospital due to relatively inconvenient transportation.

Conclusion

This article explored the hottest health reform topics related to the commercial medical insurance market in China and provided a market overview for HDHL plans and risk factor analysis based on sales strategy and geographic locations. Part 2 of this article will focus on risk factors such as disease spectrum, patient behavior analysis and COVID-19’s impact on the medical insurance industry.

Acknowledgments

Special thanks to those who contributed their knowledge and expertise in the preparation of this article:

- Chloe Wang, FSA

- Pricing actuaries Xin Chang, ASA; Xiaoyu Ding; Yingfei Ma, ASA; Xue Sheng and Teng Zhang

- Members from the Experience Analysis and Marketing teams from the SCOR Beijing Branch

Statements of fact and opinions expressed herein are those of the individual authors and are not necessarily those of the Society of Actuaries or the respective authors’ employers.

References:

- 1. Life insurance in China has a broad definition, consisting of not only life insurance as defined in the United States, but also health insurance and pension. ↩

Copyright © 2021 by the Society of Actuaries, Chicago, Illinois.