Navigating the Future

Assessing the sidecar option

August 2024Just like the motorcycle appendage rarely seen on the open road, sidecars in the life insurance industry can turn heads when announced. Sidecars, which are special purpose vehicles (SPVs) that transfer risks to capital markets in life insurance securitization, are a type of reinsurance that allow investors to take on insurance risk for a return. They can help life insurers share their risk with investors who give capital to the sidecar and receive part of the profits from the insurance risk.

A sidecar could be viewed as just another form of reinsurance. But sidecars have unique features, starting with leveraging outside capital and expertise through an affiliated reinsurer.

In our experience, a sidecar strategy can offer many accretive attributes, such as promoting growth and fostering mutually beneficial partnerships. However, sidecars can present challenges and lead to too many hands on the steering wheel, perhaps all pulling in different directions. To achieve alignment across all stakeholders, we believe it is crucial to thoughtfully design each aspect of the sidecar to ensure it operates effectively. The associated resource allocation requires strong organizational commitment to the strategy; otherwise, getting through the fundraising stage may be insurmountable.

While time will tell if the wave of sidecar announcements peaked in 2023 with five major launches (see Table 1), our expectation is that a number of life insurers will explore the use of sidecars in the coming years. This article discusses important considerations and options for life insurers contemplating the use of a sidecar. In particular, the asset-intensive market offers a number of established, unaffiliated reinsurers that can deliver complete solutions at attractive terms. Assessing the trade-offs between a sidecar and traditional reinsurance can help determine the best-equipped vehicle for the journey ahead.

The New Car on the Road

Since their emergence after the 2005 hurricane season, more than 2001 property and casualty sidecars have been introduced. Recently, the sidecar option has started to attract considerable attention from life and annuity (re)insurers as well. Traditionally, sidecars have functioned as mechanisms for sharing risk, leveraging third-party capital to enhance an insurance company’s financial indicators. More recently, a number of life insurers, frequently having some degree of private equity involvement or capacities in asset origination and management, have set up their own sidecars.

Table 1: Recent Sidecar Announcements

| Year | Lead Company | Asset Manager | Sidecar |

| 2024 | NLG | 26 North | 26N Re2 |

| 2023 | RGA | RGA | Ruby Re3 |

| 2023 | Prudential | PGIM and Warburg Pincus | Prismic Re4 |

| 2023 | Athene | Apollo | ACRA 25 |

| 2023 | Global Atlantic | KKR | Ivy Re 26 |

| 2023 | Kuvare | Davidson Kempner | Kindly Re7 |

| 2022 | American Equity LIC | American Equity Investment Life Holding Company | AEL Bermuda Re8 |

| 2022 | Massachusetts Mutual | Barings | Martello Re9 |

| 2021 | Security Benefit | Eldridge | SkyRidge Re10 |

| 2020 | Global Atlantic | KKR | Ivy Re11 |

| 2019 | Athene | Apollo | ACRA12 |

Many recent sidecar strategies have concentrated on mitigating risk while increasing assets under management (AUM) to maintain fee income for the sponsor and its partner asset manager. However, a range of other sidecar benefits have surfaced, including:

- Securing additional capital to stimulate growth

- Accessing more advantageous offshore capital and tax benefits

- Lowering balance sheet and earnings volatility

- Collaborating with a specialized asset management firm

Typically, an asset manager desiring a mandate for the sidecar’s assets will acquire a small stake in the sidecar to reinforce alignment of interests. The economics for an asset manager can be quite compelling—a 20% stake in a vehicle with an asset leverage of 20 could see AUM of 100x the actual sidecar investment.

Beyond access to this AUM, the potential for high, stable returns over a defined period can attract various types of sidecar investors. Of course, this is subject to intense scrutiny of the business plan and liquidity options, and ongoing oversight that may include seats on the governing board of the sidecar.

Designing the Sidecar: Key Considerations

Setting up a sidecar shares many similarities with establishing an insurance company. The process often can span 18 months or longer, requiring high organizational conviction to gain traction. The choices made in designing the sidecar may have significant and interconnected impacts on its success.

In our experience, careful evaluation of the following strategic questions is essential:

- What types of risks will it address? The sidecar can provide reinsurance for existing or new business across various products at different levels of quota shares.

- What is the fundamental investment strategy? The sidecar might employ alternative investment strategies that can enhance portfolio yield.

- How will the pricing of risk transfer be determined? The economics of the sidecar, including target returns, products and fee structure, will deeply affect both the cedant and investors.

- Where will it be domiciled? Often, choosing to domicile offshore underpins the sidecar’s economics, boosting capital and tax efficiency.13

- What will the reinsurance structure look like? Options like trusts, over-collateralization or onshore assets can mitigate counterparty risk, though each option requires distinct management considerations.

- How will it be managed? Governance activities, including management control and voting rights, play a crucial role in ensuring the vehicle’s long-term success.

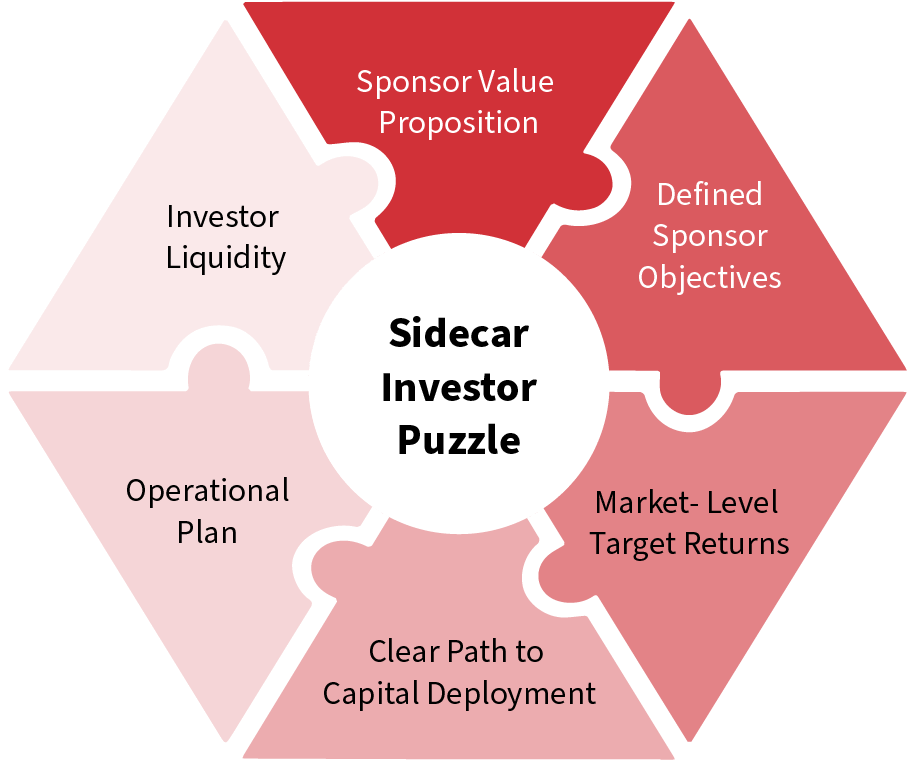

Connecting the sponsor’s vision and objectives to the sidecar investor’s objectives magnifies the difficulty of assembling the sidecar, as shown in Figure 1.

Figure 1: Key Pieces to the Sidecar Investor Puzzle

All stakeholders have notable influence over the viability of the sidecar and may have different motivations for their participation. For example, motivations may include the following:

- Sponsoring company objective: Optimize the economic value through fees and ceding commissions while freeing up capital.

- Investor objectives: Invest capital efficiently, earn a high-risk premium over a limited investment time frame and, for some investors, secure substantial fees from additional services, such as asset management.

- Regulator (local, offshore, tax) objectives: Ensure the sidecar adheres to all relevant regulations and that the structure does not undermine the intended legal framework, thereby avoiding risks to policyholders and the system.

With precedents in place and an increasing interest in the sidecar space based on our experience, these stakeholders will be keen to influence sidecar design. It is our belief that additional stakeholders, including employees, policyholders, advisers and the parent company, also undoubtedly will want to have input into the sidecar design. The individual goals of all stakeholders should be considered as part of the design and decision-making process.

Moreover, sponsors should be conscious of current macroeconomic conditions, which drastically differ from the environment of the past few years that contributed to the popularity of sidecars. Capital markets in the United States arguably face tighter funding conditions, higher return requirements and greater uncertainty. Given the typical timeline of establishing such vehicles, financial conditions may change markedly between the initiation and execution of the sidecar.

Moving from design to production to make the sidecar a reality appears to us the most challenging part of the process, which can take as long as two years (see Figure 2). The right design is certainly a major part of being ready to deploy the capital and operate the vehicle.

Figure 2: Sidecar Timeline: Design to Production

Source: RGA experience

Evaluating the Trade-offs: Sidecars and Traditional Reinsurance Models

A sidecar can be considered just a variation of traditional reinsurance models, such as a full risk-transfer treaty with an unaffiliated, established reinsurer. The traditional reinsurance market is expansive and well-established, with key players providing competitive solutions that may offer similar advantages and options as those found in sidecars. While sidecars and traditional reinsurance can address comparable risks using similar structures, the required effort, economic factors, execution risks and expertise for each can vary significantly.

Setup and Management

When it comes to setup and management, launching a sidecar is a major undertaking, typically requiring at least 18 months from strategy to execution, in our experience. In addition to ongoing management efforts, it may be difficult to change course as conditions and needs evolve. Traditional third-party reinsurance, we’ve experienced, involves a well-defined process for finding a reinsurance counterparty, and it generally can be done in three to six months.

Economics

In terms of economics, a sidecar may generate high investor interest, but it also creates pressure to maximize returns for outside investors. The economic analysis should consider the role of fees and counterparty credit risk, which may offset pricing leverage. Traditional third-party reinsurance relies on established players with generally leading capabilities, and risk appetite may translate into favorable economics for the cedant. In our opinion, both sidecars and traditional third-party insurance likely could achieve similar structural advantages and risk coverage, so the implementation details likely will drive the relative economic advantages.

Expertise

As for expertise, potential sidecar investors may have complementary capabilities on the liability, asset or structuring side. The sidecar may be conducive to such arrangements because there is mutual interest in performance, but considering the impact on fees and control likely would be important. Traditional third-party reinsurance potentially could leverage the expertise of the reinsurer for the treaty’s design and fulfillment. Experienced reinsurers may further enhance partnerships by taking a lead role in ongoing product design and management, sharing an interest in maintaining the policyholder base with the ceding company.

Execution Risk

While there are examples of successful sidecar launches, based on our observations, execution risk tends to persist across the sidecar life cycle, stemming from a range of areas, such as stakeholder alignment, investor exit options and regulatory oversight. Execution risk is typically lower with traditional third-party reinsurance, given the shorter execution time frame, bilateral (in lieu of multilateral) negotiations and certainty of coverage.

Buyer’s Guide

A sidecar could be a beneficial addition to the comprehensive reinsurance and capital management strategy of a company that:

- Possesses a substantial balance sheet

- Has a sophisticated capital management team and strong relationships in capital markets

- Can allocate several senior leaders from their full-time jobs to the sidecar initiative for a minimum of 18 months

- Is prepared to give investors an asset management mandate to meet targets for specific asset classes and can conduct due diligence

- Has a seed block that algins with the liability profile of the sidecar

- Is ready to commit to a long-term strategy of ceding liability flows

Conversely, pursuing a tailored reinsurance solution might be preferrable for a company that:

- Needs to free up capital in the short term

- Prioritizes high flexibility in managing capital and risk retention

- Values the reliability and counterparty strength of a diversified, experienced reinsurance company

- Wishes to leverage the specialized knowledge of an asset-intensive reinsurer to improve the economics in a defined arrangement

- Prefers not to maintain liabilities on the balance sheet for the 18+ months that often are required to establish a sidecar

- Seeks specific product expertise and the flexibility to modify product focus to address distribution needs, evolving buyer preferences and market conditions

In Summary

We believe sidecars have the potential to provide substantial value under the right circumstances. We recommend carefully assessing the associated costs (time, resources, capital) and challenges to execution prior to pursuing.

We believe early prioritization of objectives is essential in the development of the third-party capital strategy. This will inform the assessment of the notable trade-offs in pursuing the sidecar vs. other alternatives, such as traditional asset-intensive reinsurance.

Statements of fact and opinions expressed herein are those of the individual authors and are not necessarily those of the Society of Actuaries or the respective authors’ employers.

References:

- 1. What Is a Reinsurance Sidecar? Artemis (accessed July 11, 2024). ↩

- 2. 26North Reinsurance Holdings. 26North Re Closes $4.9B Reinsurance Transaction With National Life Group’s Life Insurance Company of the Southwest. PR Newswire, May 7, 2024 (accessed July 11, 2024). ↩

- 3. Reinsurance Group of America, Incorporated. Reinsurance Group of America, Incorporated Launches Ruby Reinsurance Company. December 6, 2023 (accessed July 11, 2024). ↩

- 4. Prudential Financial, Inc. and Warburg Pincus. Prudential Financial, Inc. and Warburg Pincus Announce Launch of Prismic Life Re. September 7, 2023 (accessed July 11, 2024). ↩

- 5. Gallin, Luke. Apollo/Athene’s ACRA 2 Sidecar Commitments Reach $2bn at First Close. Artemis, February 9, 2023 (accessed July 11, 2024). ↩

- 6. Evans, Steve. Global Atlantic Raises Over $2.4bn for Second Reinsurance Sidecar Ivy II. Artemis, July 10, 2023 (accessed July 11, 2024). ↩

- 7. Evans, Steve. Kuvare Sets up $400m Life & Annuity Reinsurance “Sidecar” Kindley Re. Artemis, January 12, 2023 (accessed July 11, 2024). ↩

- 8. Evans, Steve. American Equity Plans Sidecars for Third-party Annuity Reinsurance Capital. Artemis, March 9, 2022 (accessed July 11, 2024). ↩

- 9. Martello Re Limited. New Reinsurer “Martello Re” Launches With Backing of MassMutual, Centerbridge Partners and Brown Brothers Harriman. January 11, 2022 (accessed July 11, 2024). ↩

- 10. Security Benefit Life Insurance Company and Subsidiaries. Consolidated Financial Statements. April 26, 2022 (accessed July 11, 2024). ↩

- 11. Evans, Steve. Global Atlantic Launches Ivy, a $1bn Sidecar-like Life & Annuity Co-investment Vehicle. Artemis, April 8, 2020 (accessed July 11, 2024). ↩

- 12. Evans, Steve, Apollo/Athene’s ACRA Sidecar Raise Hits $3.2bn of Commitments. Artemis, February 18, 2020, (accessed July 11, 2024). ↩

- 13. Sun, Yiru (Eve), and Ghislain Ghyoot. Cayman Reinsurance Market and Opportunities. Reinsurance News, December 2023. ↩

Copyright © 2024 by the Society of Actuaries, Chicago, Illinois.