Ready to Make a Move

A brief history of the U.S. health care system and a look at its future trajectory

August/September 2019Proponents of a centralized national health care system compare U.S. health care spending to other countries to support their view. Indeed, health care in the United States costs twice the average of other wealthy countries.1 However, the realities of U.S. health care are complicated and systemic. Moving to a single payer system is unlikely to achieve cost parity with other countries without first addressing the underlying forces that drove us to our present state.

This article offers highlights along the journey to our present-day health care system and concludes with a hopeful view of the road ahead.

A Brief History

The United Kingdom has a national health care system that began with the National Insurance Act of 1911, which introduced compulsory health insurance and physician capitation. At about that same time, Theodore Roosevelt and his supporters also campaigned for state-run compulsory health insurance in the United States.

However, the idea was met with strong opposition in the United States. Health care practitioners worried compulsory insurance would erode their incomes and independence.2 The American Medical Association (AMA) labeled the idea socialized medicine, and socialism was viewed by many at that time as anti-American.

The idea of a state-run health care system surfaced again in 1933, as part of the New Deal legislation. But publicly funded health care was dropped from the New Deal because of the AMA’s continued strong opposition.3 This opposition was largely responsible for pushing the United States toward private health insurance.

Enter Private Health Insurance

Three private sector initiatives laid the foundation for what would become a thriving health insurance industry. Hospitals and physician groups began selling insurance programs to cover hospital and physician-related expenses. These programs would later become the first Blue Cross and Blue Shield programs.4 These were largely health care financing mechanisms with virtually no direct influence on health care decision-making.

Henry J. Kaiser employed a different approach, using health care providers on-site to meet the needs of his construction site, shipyard and steel mill workers. These programs evolved into today’s Kaiser Permanente.5

Wage and price controls during World War II prevented employers from competing for employees by offering higher wages. Health insurance and benefits became an alternative way to compete for talent. Employers gained tax advantages for providing health care benefits in 1943 and enhanced tax benefits in 1954, further supporting an emerging health insurance marketplace.6

Several insurance companies entered this growing space. Over time, health care decision-making authority started to shift from treating physicians to insurance companies as managed care programs emerged and began to evolve. Early managed care components included hospital precertification, utilization review, case management and provider networks [preferred provider organization (PPO) networks].

Impact of Managed Care

For many years, most physicians delivered care out of their private, independent offices, and they had nearly total control over medical decision-making. Most hospitals were passive participants in health care delivery, essentially providing a place for physicians to do their work.7

By the 1970s, this was starting to change. Spurred by the passage of the Health Maintenance Organization Act of 1973, a new kind of insurer—health maintenance organizations (HMOs)—began to grow rapidly, covering 29 million people across 662 HMO plans by June 1987.8 HMO plans generally featured much narrower provider networks and transferred more of the medical decision-making and authority to the insurer.

HMO plans were attractive among healthier people who were not concerned about the narrower HMO networks, because HMOs generally offered rich benefits and lower premiums. As a result, anti-selection became an important factor in financial performance, because HMO plans often attracted the lowest-cost risks, leaving other insurers to cover people with more costly health conditions.

Over time, the distinction between PPO plans and HMO plans became blurry. Some HMO plans started offering benefit plans with deductibles and coinsurance that looked more like PPO plans, and PPO plans adopted many of the managed care features espoused by HMOs. Larger insurers began acquiring smaller insurers and HMO plans, blurring the distinction even further. These larger insurers were amassing negotiation power over health care providers.

While most hospitals were passive throughout most of the 1900s, there were notable exceptions such as Johns Hopkins, Cleveland Clinic and Mayo Clinic. Organizations like these developed group physician practices long before it was fashionable, and they are responsible for many of the health care innovations we’ve come to rely on.

As insurers began to consolidate, more hospitals and physician groups combined as well. While providers sometimes consolidated to gain efficiencies, provider desire to negotiate better deals with insurance companies fueled much of the consolidation activity.9 And with this consolidation, physicians gave up even more individual autonomy.

Major Legislative Actions

From 1965 to today, legislation has played and continues to play a critical role in shaping our health care system. From Johnson to Reagan to Clinton to Obama, significant laws regulating health care coverage and access have been signed during the past 50 years.

Medicare (1965) was established to provide national health insurance for eligible people over age 65, and Medicaid (1965) was created to provide medical insurance for people who qualify by virtue of low income. Subsequent legislation has expanded both programs.10

The Consolidated Omnibus Budget Reconciliation Act (COBRA) (1985) has provided employees the ability to continue employer-based health insurance coverage after terminating employment for a period of time.11 COBRA has been unpopular with employers because it effectively increases employer cost and risk exposure.

The Health Insurance Portability and Accountability Act (HIPAA) (1996) has served two important functions. The first has been to effectively eliminate health insurance waiting periods when a qualified individual changes jobs. Second, HIPAA has provided privacy and security protection relating to health care data generated by health plans and health care providers. While these objectives are important, HIPAA has increased the administrative burden and cost for employers, insurance companies and health care providers.

The Patient Protection and Affordable Care Act (PPACA) (2010) significantly changed the rules employers must follow to provide health insurance to employees.12 One goal of the PPACA was coverage expansion. The year before major PPACA coverage provisions went into effect, 44.4 million nonelderly persons lacked coverage. Three years later, the number of uninsured people had dropped to 26.7 million, but that number rose to 27.4 million in 2017.13

Current Health Insurance Distribution

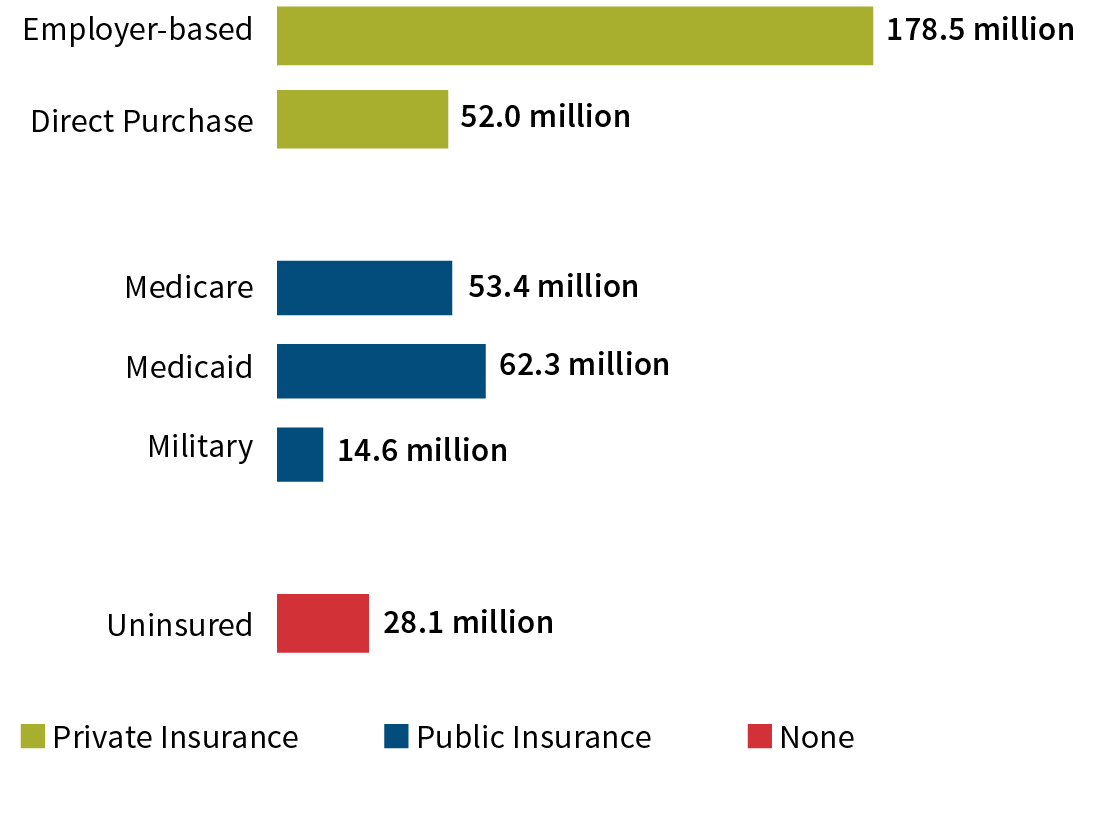

In the early 1900s, most people were uninsured because health care costs were relatively low and the need for health insurance was only beginning to emerge. Today, some form of insurance covers the vast majority of people in the United States. As shown by Figure 1, employer-based insurance is the most common source, covering more individuals than the entire public insurance sector.14

Figure 1: Number of Individuals With Health Insurance Coverage in 2016 by Source*

*Some individuals may be represented in more than one category.

Source: Developed with data from the U.S. Census Bureau (see reference 14)

Medical Advancement/Chronic Disease

Much of our health care cost acceleration has been blamed on advancements in medical science, including diagnostics, surgical procedures and other treatments, and pharmaceuticals. These advancements improve quality of life and save lives. And patients want them.

For example, from 2006 to 2015, the mortality rate associated with coronary artery disease decreased 32.4 percent from 186.6 to 126.2 deaths per 100,000 adults. Over that same period, the mortality rate associated with stroke declined 20.5 percent.15

Even so, heart disease continues to be the leading cause of death for both men and women. About half of the U.S. population has at least one of the three key risk factors for heart disease: high blood pressure, high LDL cholesterol and smoking.16 According to the Centers for Disease Control and Prevention (CDC), 80 percent of premature heart disease and strokes are preventable.17 But most cardiovascular medical advances have focused on treatment rather than prevention.

The death rate from all cancers fell by 26 percent between 1991 and 2015. The breast cancer death rate fell by 39 percent from 1989 to 2015, driven primarily by improvements in early detection. The death rate from colorectal cancer fell by 52 percent from 1970 to 2015, driven by increased screening and advances in cancer treatment.18

We also enjoy many other medical advances that are too numerous to list. Thanks to these advances, many of yesterday’s terminal illnesses are now survivable as chronic disease. But this reduced mortality doesn’t always translate into reduced health care cost and improved quality of life. Following a major stroke, many patients face long-term debilitation.

Chronic disease is a huge health care cost driver, and we seem to be losing the battle against it and its related costs, especially those driven by obesity. As of 2015, two-thirds of U.S. adults are either overweight or obese. Several studies demonstrate that being overweight or obese increases the risk of death from cardiovascular disease, diabetes, cancer or accidental death. Certain cancers, surgical complications and mental health issues also are associated with being overweight and obese.19

The AMA recognized obesity as a complex chronic disease for the first time in 2013.20 Prior to that, health care providers were seldom paid for treating obesity—treating it was not viewed as the responsibility of the health care delivery system. And although the PPACA made insurance coverage for obesity care the law, obesity care in the traditional health care setting is still rare.

Health Care Cost Trends

In 1965, total U.S. health care expenditure was 5.6 percent of the gross domestic product (GDP). Spending increased by 11.9 percent from 1966 to 1973 as a result of rapid coverage expansion and increased utilization. From 1974 to 1982, price inflation drove an average annual increase of almost 14 percent. By the end of 1982, both private and public health care expenditure accounted for 10 percent of GDP.21

Since 1982, public and private efforts to reform health care led to trends rising and falling, but generally staying below 10 percent of GDP. In a 2018 report by Willis Towers Watson, the overall health care trend in the United States decreased year over year from 8.7 percent to 7.9 percent.22 U.S. health care expenditures reached 17.9 percent of GDP by 2017.23

The health care trend affecting employer spending is less than the nation’s total. Willis Towers Watson reported the average health care cost increase before benefit design changes was 5.0 percent in 2017, and it was expected to be 5.3 percent and 5.5 percent in 2018 and 2019, respectively.24

Potential Hope for the Future

A health care model incentivizing treatment of the sick rather than keeping people healthy has led to high rates of chronic conditions such as heart disease, cancer and diabetes, which are our nation’s leading cost drivers. Often a byproduct of lifestyle, most chronic disease burden is preventable.

According to the CDC, 90 percent of our nation’s health care spend is on people with chronic and mental health conditions.25 The U.S. health care delivery system is known for a high standard of care when treating chronic disease, yet most of this treatment is avoidable by changing lifestyle and behaviors.

But why is now different than past efforts? There are appealing forces that hold promise for managing chronic disease and reducing its burden on the U.S. economy.

Accountable Care Organizations

The PPACA authorized the Centers for Medicare and Medicaid Services (CMS) to define parameters that help health care providers establish accountable care organizations (ACOs) to ensure patients get the right care at the right time and avoid unnecessary and duplicative care. ACOs enable doctors, hospitals and other providers to coordinate high-quality care.

CMS provides incentives for effective care coordination through a Medicare Shared Savings Program. Providers who perform well are rewarded, and providers who fall short receive reduced reimbursements under this program.26 These incentives reward health care providers for addressing the underlying risk factors and care gaps associated with chronic disease.

Many ACOs provide the same coordinated care for non-Medicare patients, and they seem poised to realize benefits from economic efficiencies and intelligent coordination available through integrated provider systems and large group practices. ACOs enable and require new levels of health care innovation to achieve success.

Primary Care Incentive Programs

Private insurers deployed incentive programs designed to change how providers are paid for primary care. Past reimbursement strongly incentivized more care and tests to earn more income. New incentive models aim to tie provider income to closing gaps in care and achieving desired outcomes.

These programs hold promise for enabling primary care physicians to help people get and stay healthy. Patient engagement will drive success for both ACOs and Primary Care Incentive Programs (PCIPs). The old paradigm encouraged patients to seek care only when they were sick. This paradigm, too, must change and may be the most difficult task of all.

On-site and Near-site Health Care

The National Association of Worksite Health Clinics reported one-third of employers with 5,000 or more employees provide an on-site or near-site employer-sponsored personal health care clinic, and an additional 11 percent are considering a clinic for 2019. Among smaller employers (500 to 5,000 employees), 16 percent currently offer an employer-sponsored clinic, and another 8 percent are considering one for 2019.27

On-site health care programs can remove the barriers of time, distance and cost that keep patients from receiving the care they need, when they need it. Programs focused on health improvement can change how employees and their dependents consume services and can encourage more effective patient engagement.

Well-designed incentive programs, effective communication strategies and risk-based patient outreach are powerful tools for engaging employees and their family members in understanding and managing chronic disease risks and conditions. For example, the company for which I work, Healthstat Inc., uses predictive modeling based on current claims data and patient biometrics to identify high-risk patients, drive patient outreach and inform the patient-provider relationship with knowledge and insight at the point of care. This point-of-care insight supports risk mitigation through behavior change and helps close gaps in care.

For specialty care outside the scope of the clinic, providers connect patients to a qualified community-based specialist who can provide information and support, ensuring the patient receives the care to manage their condition and regain full health. On-site clinics also provide follow-up care after a specialist visit, which can reduce readmissions and complications from recovery.

Conclusion

The United States spends nearly twice the average of other wealthy countries on health care per person. Despite critical opinions regarding commensurate quality, I believe our nation’s health care providers are delivering the highest quality care when we are sick. But as a nation, we need to do more to avoid sickness to begin with.

Many forces and events influenced our state of health care today. As we turn our attention toward managing chronic disease through ACOs, new primary care incentive models, and effective on-site and near-site health care, we have an opportunity to change our nation’s trajectory, with an aim of helping our country’s population to be as healthy as it can possibly be.

References:

- 1. Sawyer, Bradley, and Cynthia Cox. How Does Health Spending in the U.S. Compare to Other Countries? Kaiser Family Foundation, December 7, 2018 (accessed April 12, 2019). ↩

- 2. Hoffman, Beatrix. 2003. Health Care Reform and Social Movements in the United States. American Journal of Public Health 93, no. 1:75–85. ↩

- 3. Ibid. ↩

- 4. An Industry Pioneer—Leading the Way in Health Insurance, BlueCross BlueShield (accessed April 12, 2019). ↩

- 5. Kaiser Permanente Thrive Exposed. History of the Kaiser Permanente Medical Care Program (accessed April 12, 2019). ↩

- 6. Blumberg, Alex, and Adam Davidson. Accidents of History Created U.S. Health System. National Public Radio, October 22, 2009 (accessed April 12, 2019). ↩

- 7. Dranove, David. 2002. The Economic Evolution of American Health Care: From Marcus Wellby to Managed Care. Princeton, New Jersey: Princeton University Press. ↩

- 8. Gruber, Lynn R., Maureen Shadle, and Cynthia L. Polich. 1988. From Movement to Industry: The Growth of HMOs. Health Affairs 7, no. 3:197–208. ↩

- 9. Supra note 7. ↩

- 10. Centers for Medicare & Medicaid Services. History. CMS.gov, August 5, 2019 (accessed April 12, 2019). ↩

- 11. U.S. Department of Labor. Health Plans & Benefits: Continuation of Health Coverage—COBRA. U.S. Department of Labor (accessed April 12, 2019). ↩

- 12. U.S. Centers for Medicare & Medicaid Services. Patient Protection and Affordable Care Act. HealthCare.gov (accessed April 12, 2019). ↩

- 13. Garfield, Rachel, Kendal Orgera, and Anthony Damico. The Uninsured and the ACA: A Primer—Key Facts About Health Insurance and the Uninsured Amidst Changes to the Affordable Care Act. Henry J. Kaiser Family Foundation, January 25, 2019 (accessed April 12, 2019.) ↩

- 14. Barnett, Jessica C., and Edward R. Berchick. Health Insurance Coverage in the United States: 2016. United States Census Bureau, September 12, 2017 (accessed April 12, 2019). ↩

- 15. Behavioral Risk Factor Surveillance System. Leading Indicators for Chronic Diseases and Risk Factors. Centers for Disease Control and Prevention (accessed April 26, 2019). ↩

- 16. Centers for Disease Control and Prevention. Heart Disease Facts. CDC.gov, November 28, 2017 (accessed May 21, 2019). ↩

- 17. Centers for Disease Control and Prevention. Preventing 1 Million Heart Attacks and Strokes. CDC.gov, September 6, 2018 (accessed May 21, 2019). ↩

- 18. Simon, Stacy. Facts & Figures 2018: Rate of Deaths From Cancer Continues Decline. American Cancer Society, January 4, 2018 (accessed April 26, 2019). ↩

- 19. Hruby, Adela, and Frank B. Hu. 2015. The Epidemiology of Obesity: A Big Picture. Pharmacoeconomics 33, no. 7:673–689. ↩

- 20. Kyle, Theodore K., Emily J. Dhurandhar, and David B. Allison. 2016. Regarding Obesity as a Disease: Evolving Policies and Their Implications. Endocrinology and Metabolism Clinics of North America 45, no. 3:511–520. ↩

- 21. Catlin, Aaron C., and Cathy A. Cowan. History of Health Spending in the United States, 1960–2013. Centers for Medicare & Medicaid Services, November 19, 2015 (accessed April 12, 2019). ↩

- 22.Willis Towers Watson. 2019 Global Medical Trends Survey Report. Willis Towers Watson, November 2, 2018 (accessed April 12, 2019). ↩

- 23. Centers for Medicare & Medicaid Services. National Health Expenditure Data: Historical. CMS.gov, December 11, 2018 (accessed April 12, 2019). ↩

- 24. Willis Towers Watson. 2018. Willis Towers Watson 23rd Annual Best Practices in Health Care Employer Survey. Willis Towers Watson (accessed April 12, 2019). ↩

- 25. Ibid. ↩

- 26. Centers for Medicare & Medicaid Services. Accountable Care Organizations (ACOs). CMS.gov, March 8, 2019 (accessed April 12, 2019). ↩

- 27. Mercer. 2018. Worksite Medical Clinics—2018 Survey Report. National Association of Worksite Health Centers (accessed April 12, 2019). ↩

Copyright © 2019 by the Society of Actuaries, Chicago, Illinois.