Successes of the ACA

A reduced uninsured rate, increased benefits coverage and more plan options for low-income individuals are among the ACA’s triumphs

March 2020Photo: iStock.com/olm26250

It has been 10 years since the Patient Protection and Affordable Care Act (PPACA or the ACA) was enacted in March 2010. As a result of the ACA, the nature in which Americans receive health insurance coverage has changed substantially. Since enactment, there have been modifications to the ACA and other proposals designed to materially alter the law. Nevertheless, many components of the ACA remain in place today and have been considered important successes.

Review of the ACA

The Affordable Care Act (ACA) was a landmark statute with three main goals in mind:

- Make health care more affordable and available.

- Expand the Medicaid program to cover more people.

- Support innovative health care models to lower costs.

To meet the ACA’s goals, the designers of the legislation …

This article focuses on the ACA’s successes as it begins its voyage into its second decade of existence. More specifically, we will:

- Highlight a few unexpected results from regulatory or policy changes.

- Review original, yet sometimes forgotten, components of the law that still hold strong.

COMPONENTS WITH LEGISLATIVE OR REGULATORY CHANGES

Since 2010, there have been several legislative, regulatory and administrative changes to the ACA. Examples include cost-sharing reductions (CSRs), which were designed to help cover out-of-pocket expenses for low-income individuals, are no longer funded by the federal government; the individual mandate penalty no longer applies; and “skinny” plans (i.e., plans with leaner coverage) are allowed to be sold. We’ll begin with a brief discussion of metal tiers and skinny plans. The discussion will then turn to the impact of CSRs and individual mandate policy changes.1

Metal Tiers/Skinny Plans

The ACA helped consumers understand their health care coverage by categorizing the coverage level of health plans that would be sold on an exchange. The four tiers of coverage were codified by a metal— bronze, silver, gold and platinum. Each metal tier was defined by the average amount of the medical costs covered by a health insurer within each tier—that is, the benefit richness of the plan.2 Bronze plans represent the lowest level of benefit richness (60 percent of benefits covered by an insurer) while platinum plans represent the greatest benefit richness for the insured (90 percent of benefits covered by an insurer). All metal plans must include the 10 Essential Health Benefits (EHBs)3 and a cap on the amount of health care costs an insured can incur annually (also known as an out-of-pocket maximum).

Choosing a plan on the exchange is easier once the “richness” or value of the four metals is understood. If a young healthy individual wants a low premium and coverage to protect from serious injury or illness, they will likely gravitate toward a bronze plan. On the other hand, an individual who needs frequent care and is willing to pay a higher premium will look to gold and platinum plans.

Recently, the Trump administration relaxed the rules around metal tiers and has begun allowing carriers to sell skinny plans, or plans that offer less coverage and potentially increase a member’s cost-sharing.4 The true impact of skinny plans is not yet known, and it will need to be discussed in the future once the impact of these types of plans can be assessed.

Cost-sharing Reduction Subsidies, Premium Subsidies and Silver Loading

There are two primary types of federal financial assistance through the ACA to mitigate the financial burden for low-income consumers. The first is advance premium tax credits (APTCs) and the other is CSRs, as referenced earlier.

APTCs lower the monthly premiums for individuals who have incomes below 400 percent of the federal poverty line (FPL),5 while CSRs reduce health care costs associated with deductibles, coinsurance, copays and maximum out-of-pocket amounts for individuals with incomes up to 250 percent of the FPL.6 In other words, APTCs decrease an individual’s monthly payment for obtaining health coverage, while CSRs reduce an individual’s own cost for utilizing the health coverage.

To obtain the extra level of support for out-of-pocket costs, an individual must purchase a silver plan. In a typical silver plan, an insurance company pays for 70 percent of expected health care costs, while the individual is responsible for the other 30 percent. CSRs increase the 70 percent average paid by the insurer up to 94 percent, depending on the individual’s income level. To compensate insurers for the excess cost of providing CSRs, federal payments are made directly to insurers.

In 2016, a lower federal court agreed with House Republicans that Congress never appropriated funds for CSRs and ordered that direct reimbursements for CSRs to insurers end.7 During the next year, Congress was able to pass a spending bill that would fund CSRs—but not permanently—leaving the fate of CSRs in the hands of the executive branch. The decision to end funding for CSRs came in October 2017, meaning insurers would not receive any direct remuneration for CSRs from the federal government. However, based on the language of the ACA, insurers were still required to cover the excess health care costs for eligible individuals.

At the time of CSR de-funding, it was expected that many insurers would exit the individual ACA market due to the lack of adequate funding. While carriers did exit the individual market, a mass exodus did not occur because of alternative funding approaches used by health insurance issuers and state insurance departments to mitigate the effect.8 The Kaiser Family Foundation estimates (in Figure 1) the average number of carriers per state in the individual market dropped from 4.3 in 2017 to 3.5 in 2018, though this number has risen each year since.9

Figure 1: Average Number of Exchange Insurers by State: 2014–2020

Hover Over Image for Specific Data

In 38 states, insurers added back the cost of CSRs into silver plan premiums based on guidance from state insurance departments.10 This practice, which has been allowed by the current administration through 2020, is known as “silver loading.”11 Due to the added costs, premiums for silver plans in 2018 were much larger than premiums in previous years—in some states, they were as much as 30 to 40 percent higher.12 The nationwide market average benchmark increased 34 percent from 2017 to 2018.13 Recall that the premium subsidies described previously, or APTCs, are linked to the actual silver premium levels. As silver premiums increase, the APTCs also increase.

If an eligible consumer qualifies for APTCs to use with a silver plan, they also could choose to apply the tax credit toward a bronze, gold or platinum plan, an additional benefit since these premiums would not have been affected by silver loading. For example, in some states, consumers were able to select a $0 premium bronze plan in 2018 due to the silver loading. A study from the Kaiser Family Foundation showed 4.2 million individuals in the United States were eligible for a free bronze plan in 2019.14 Additionally, consumers who preferred richer benefit plans were able to purchase less expensive gold and platinum plans than in previous years. That is, silver loading created a free coverage option for more individuals who could not afford insurance otherwise, and greater premium savings for the richer gold and platinum plans.15

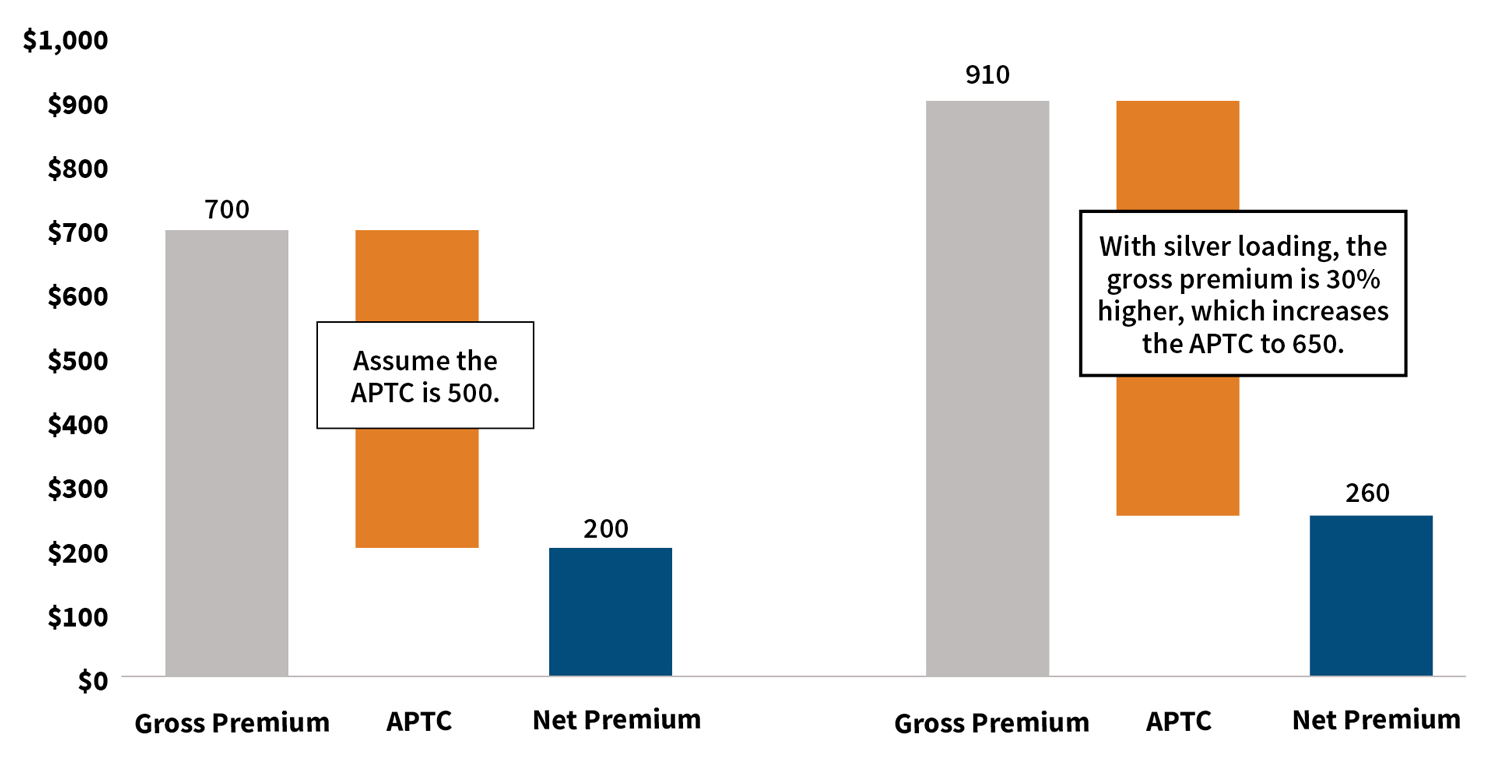

We will illustrate silver loading and the scenario in which a free bronze plan could be available, starting with Figure 2. In a scenario where CSRs are funded, assume the gross premium is $700 and the APTC is $500 for a silver plan. A member would be expected to pay $200 net premium for this silver plan. When CSRs are defunded, carriers load the cost of CSRs into silver plans (say by 30 percent), making the gross premium $910, which increases the APTC from $500 to $650. A member would now pay $260 in net premium for this same silver plan, or $60 more.

Figure 2: Illustration of Advance Premium Tax Credits Due to Silver Loading

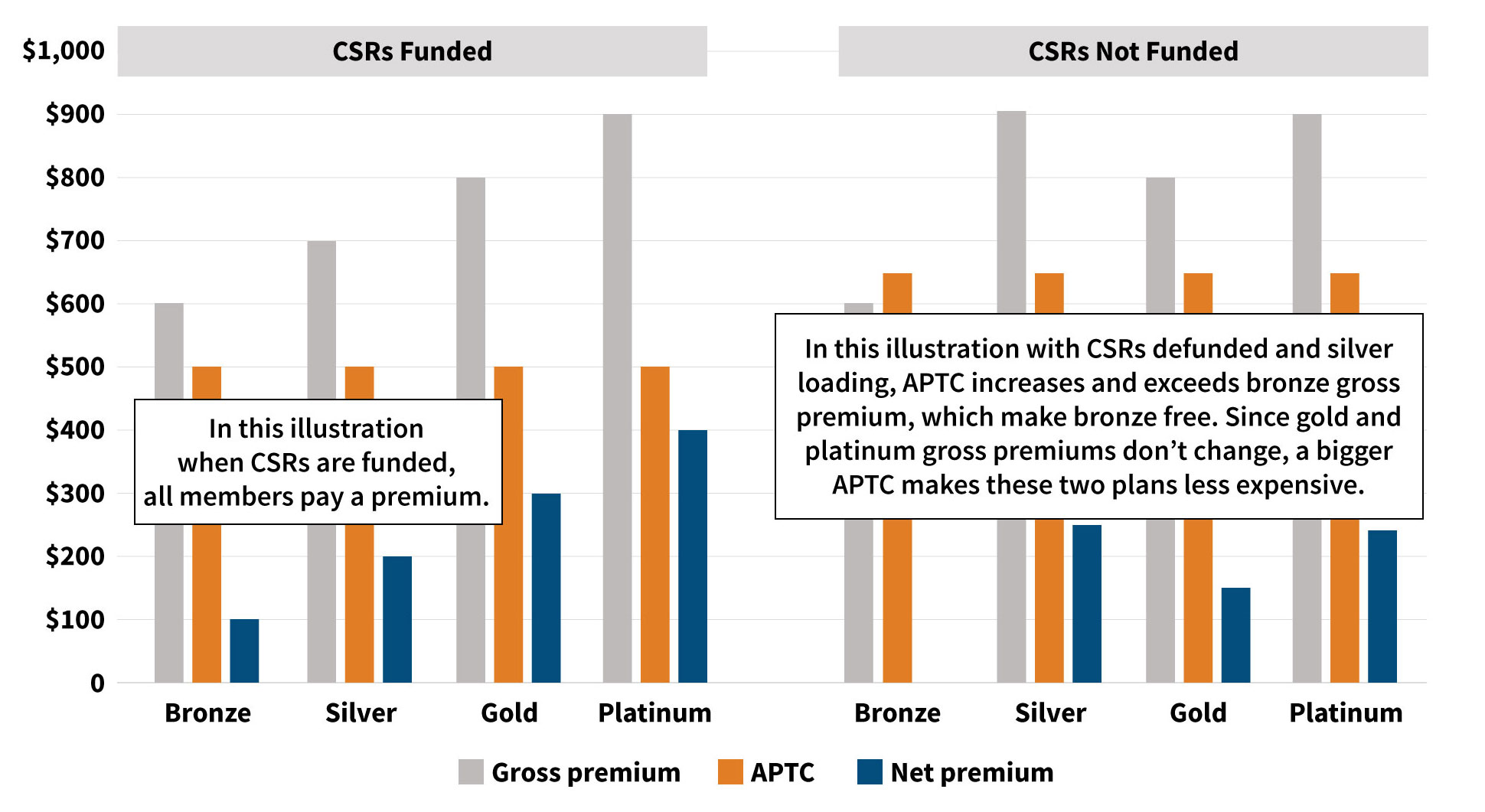

Continuing on with the same illustration in Figure 3, assume the gross premiums are $600, $700, $800 and $900 for bronze, silver, gold and platinum plans, respectively. When CSRs are funded, the APTC is $500. This means the net premiums will be $100, $200, $300 and $400 for each metal tier.

However, when CSRs are defunded and only silver plans bear the cost of CSRs, the APTC increases to $650, while the gross premiums for bronze, gold and platinum do not change. The bronze plan’s gross premium is less than the APTC, making them free to the member, while a gold or platinum plan is less expensive (e.g., gold plan net premium was $200 when CSRs are funded and $150 when CSRs are defunded).

Figure 3: Illustration of Net Premiums Change Due to Silver Loading

While APTCs have received much less legislative attention than CSRs, they are beneficial to all enrollees who qualify for premium subsidies, not just enrollees of silver plans like CSRs. Individuals who qualified for premium subsidies received larger subsidies due to silver loading no matter what metal plan they chose, as shown in Figure 3.

As a result of silver loading, APTCs outlays from the federal government increased significantly (the Congressional Budget Office estimated that defunding CSRs increased federal spending by $6 billion)16 and on-exchange enrollment for both subsidized and unsubsidized plans increased from 9.7 million to 9.9 million from 2017 to 2018. Throughout the entire 2018 open enrollment period, enrollees, including off-exchange, declined by only 1.5 percent from 13.3 million to 13.1 million.17

Individual Mandate

The individual mandate was a requirement that all individuals have a minimum level of health care coverage.18 The salient argument behind including the mandate was to increase enrollment in the health insurance market—especially for healthy individuals to help spread the risk of high-dollar, sicker members amongst a greater pool of individuals. To enforce the mandate, the ACA included a penalty on tax returns.

Nevertheless, the individual mandate penalty was repealed at the beginning of 2019. The decision to repeal was expected to cause far-reaching and irrevocable harm to the ACA. Unexpectedly, a 2019 analysis from the Kaiser Family Foundation showed that overall enrollment in the individual market fell by only 5 percent in the first quarter of 2019, as shown in Figure 4.19 The decline in enrollment was primarily driven by the unsubsidized off-exchange markets, with increasing premiums being the major concern among enrollees, rather than the repeal of the penalty for not having health insurance. Unsubsidized enrollees bear the full cost of the premium increases every year, as they do not receive federal assistance through APTCs or CSRs, and they indicate a possible relationship and reason for the small decline.20

It appears the individual mandate was not a strong motivating factor for individuals to obtain health insurance.21 Lower premiums, combined with availability of health plans on exchanges or Medicaid expansion, also offset the decline in market enrollment.22 McKinsey’s health insurance consumer survey indicates 90 percent of individuals will remain insured despite removal of the individual mandate unless premiums became unaffordable.23

Figure 4: 2015–2019 Q1 Individual Market Enrollment

Hover Over Image for Specific Data

It should be noted that the individual mandate continues to exist in some states, including Massachusetts, New Jersey and Washington, D.C.24

Summary of Regulatory Changes

Despite these regulatory changes, the subsidized market (individuals who fall between 100 percent and 400 percent of the FPL) has seen enrollment increase and has paid lower net premiums25 from 2017 to 2019, as shown in Figure 5. In other words, the subsidized population has largely been sheltered from regulatory changes affecting their ability to obtain health coverage. Therefore, it is the unsubsidized population that has been significantly impacted by these changes.

Figure 5: Comparison of Nationwide Average Premiums and Enrollment for Subsidized ACA Market

Hover Over Image for Specific Data

ORIGINAL ACA COMPONENTS

Many components of the ACA have received immense media coverage the last few years, including the aforementioned CSRs and the individual mandate. However, there are additional components of the ACA that may have been forgotten or overshadowed. Many stakeholders believe these forgotten and overshadowed ACA elements were positive components of the law.

Coverage on a Parent’s Plan Until Age 26

The ACA allowed young adults to remain on a parent’s health insurance until age 26.26 Prior to the ACA, health insurers would typically disallow coverage for individuals from their parents’ plans once they turned 19 or 20, unless they were enrolled in school full-time.27 As a result, young adults had the highest uninsured rate of any age group and the lowest rate of access to employer-based insurance prior to the passage of ACA.28

The former policy provision could create financial burdens for young adults, as many at that age are still students or unemployed.29 The National Center for Education Statistics estimates 40 percent of 18 to 24-year-old adults are enrolled in school,30 and the unemployment rate for this same age group is double that of older adults (ages 25 to 54) according to Bureau of Labor Statistics (see Figure 6).31 Further, the Centers for Medicare & Medicaid Services (CMS) states nearly half of uninsured young adults have problems paying medical bills.32

Figure 6: 2019 Monthly Unemployment Rate by Age Group

Hover Over Image for Specific Data

Since the implementation of ACA, young adults are remaining on their parents’ health insurance plans, even after they join the workforce. The ADP 2016 Health Benefits Report revealed that since 2011, the eligibility of young adults for employer coverage has increased by 9 percent from 77 percent to 86 percent; however, of those who were eligible, only 44 percent chose their employers’ plan. This is down from 57 percent in 2011,33 and can likely be attributed to the option of remaining on their parents’ plans.

Despite concerns that young adults would not sign up for health insurance, the overwhelming majority (83 percent) of Americans aged 18 to 25 are covered under a health insurance plan. This equates to roughly 4.5 million young adults who would not otherwise be covered, and that is mainly attributed to parents having the option of keeping their children younger than age 26 on their health plan.34 The uninsured rate for young adults ages 18 to 25 has dropped from 32 percent in 2010 to 15 percent in 2015 (as shown in Figure 7),35 and was more recently at 14 percent in 2017 and 2018.36

Figure 7: Uninsured Rates for Adults Ages 18 to 25

Hover Over Image for Specific Data

EHBs, Including Preventive Care

The ACA required health plans to sell products that cover 10 EHBs.37 This provision applied to all private plans sold, including group and individual products. The EHBs are:

- Ambulatory patient services

- Emergency services

- Hospitalization

- Maternity and newborn care

- Mental health and substance use disorder services

- Prescription drugs

- Rehabilitative and habilitative services and devices

- Laboratory services

- Preventive and wellness services and chronic disease management

- Pediatric services, including oral and vision care

Prior to the ACA, many plans sold to nongroups (i.e., individual plans) did not offer coverage for all 10 benefits due to the high cost of some of the benefit categories. For example, mental health benefits were only offered in 61 percent of health plans in the United States,38 and maternity and newborn care were only offered in 12 percent of individual health plans in 2013.39 Now, since they are EHBs, health insurers are required to cover mental health, maternity and preventive care.

Another EHB, preventative care, includes important benefits such as vaccines, immunization, and screenings. Under the ACA, insurers provide these at no cost to the member.40 The four leading causes of death are preventable chronic diseases. According to the Centers for Disease Control and Prevention (CDC), chronic diseases and mental health account for more than 90 percent of the nation’s $3.5 trillion in annual health care costs.41 In another example, the Surgeon General’s National Prevention Strategy draws attention to the pervasiveness of hypertension in the United States, and reducing the prevalence through preventative measures by 5 percent would lead to a national savings of roughly $25 billion a year.42

Prior to the ACA, 20 percent of women and 16 percent of men reported putting off or postponing preventative services due to cost, as shown in Figure 8.43 Additionally, an analysis in 2009 found that only six out of 47 states surveyed provided coverage for preventative services to traditional adult Medicaid beneficiaries for all 42 preventive services examined, and only 16 states provided coverage of preventative services recommended by the Advisory Committee on Immunization Practices (ACIP) without copays or deductibles.44 Today, carriers provide preventative care at no cost to members.

Figure 8: People Who Put Off Preventive Services Due to Cost

Hover Over Image for Specific Data

Preexisting Conditions Eliminated

Another instrumental part of the ACA is coverage of preexisting conditions. In other words, insurers cannot deny coverage to, or even upcharge (except for use of tobacco products), an individual purchasing coverage based on a health condition.45

Medical illnesses or injuries that exist before the start of a health plan are considered to be preexisting conditions. The U.S. Department of Health and Human Services estimated that 50 million to 129 million nonelderly individuals have some type of preexisting condition.46 Before the ACA, insurers could limit or deny coverage to individuals with preexisting conditions. Thirty-six percent of individuals surveyed reported being turned down, charged higher premiums or had specific exclusions added when purchasing health insurance coverage in the individual market before the ACA.47 In another survey, 54 percent who had individual health insurance coverage worried about losing their coverage if they became seriously ill or sick.48

Post-ACA, health insurers can no longer upcharge or deny coverage to anyone with preexisting conditions, nor can they limit benefits for those preexisting conditions. The ACA has allowed individuals with preexisting conditions to obtain coverage more easily. As a survey from The Commonwealth Fund indicated—as shown in Figure 9—70 percent of people with health problems stated it was difficult or impossible to buy coverage in 2010, and only 42 percent of people felt that way in 2016.49

Figure 9: People With Health Problems Who Have Difficulty Purchasing Health Insurance

Hover Over Image for Specific Data

Public opinion overwhelmingly supports preserving coverage for preexisting conditions. As of October 2018, 81 percent of voters think it should be illegal to deny/limit coverage, and 95 percent of U.S. employers say Congress should preserve coverage for preexisting conditions should the ACA be overturned.50,51,52 The preexisting condition provision potentially is the biggest success of the ACA, as it receives support from both sides of the political aisle.

CONCLUSION

Although the overall successes of the ACA can be debated and scrutinized by politicians, consumers and all interested stakeholders, there are components of the ACA many would deem as net positives. These successes include reducing the uninsured rate, increasing coverage for benefits such as maternity and mental health services, and offering a wider range of benefit plans for low-income individuals. As the ACA begins its second decade, it—or at least some of its components—may continue to be resilient in a tumultuous health care environment.

References:

- 1. Segarra, Marielle. “Skinny” Short-term Health Insurance Plans Expand Under Trump. Marketplace, August 1, 2018 (accessed December 15, 2019). ↩

- 2. Centers for Medicare & Medicaid Services. The “Metal” Categories: Bronze, Silver, Gold & Platinum, How to Pick a Health Insurance Plan. HealthCare.gov (accessed December 15, 2019). ↩

- 3. Families USA. 10 Essential Health Benefits Insurance Plans Must Cover Under the Affordable Care Act. Families USA, February 9, 2018 (accessed December 15, 2019). ↩

- 4. MacDonald, Ilene. Judge Gives Trump Administration the Green Light on Sale of “Skinny Plans,” ACAP Vows to Appeal Ruling. RISE, July 23, 2019 (accessed December 15, 2019). ↩

- 5. Kaiser Family Foundation. Estimated Total Premium Tax Credits Received by Marketplace Enrollees. Kaiser Family Foundation (accessed December 15, 2019). ↩

- 6. Committee for a Responsible Federal Budget. The ACA’s Cost-Sharing Reductions (CSRs): A Primer. Committee for a Responsible Federal Budget, August 29, 2017 (accessed December 15, 2019). ↩

- 7. Antos, Joseph R. and James C. Capretta. The CSR Saga: An Appropriation That Really Would Lower Spending and an Incorrect Baseline’s Perverse Effects. Health Affairs Blog, March 20, 2018 (accessed December 15, 2019). ↩

- 8. Fann, Greg. The Cost-sharing Reduction Paradox: Defunding Would Help ACA Markets, Not Make Them Implode. Axene Health Partners, August 9, 2017 (accessed December 15, 2019). ↩

- 9. Fehr, Rachel, Rabah Kamal, and Cynthia Cox. Insurer Participation on ACA Marketplaces, 2014–2020. Kaiser Family Foundation, November 21, 2019 (accessed December 15, 2019). ↩

- 10. Corlette, Sabrina, Kevin Lucia, and Maanasa Kona. States Step Up to Protect Consumers in Wake of Cuts to ACA Cost-sharing Reduction Payments. The Commonwealth Fund, October 27, 2017 (accessed December 15, 2019). ↩

- 11. Supra note 7. ↩

- 12. Gaba, Charles. 2018 Rate Hikes. ACASignups.net (accessed December 15, 2019). ↩

- 13. Kaiser Family Foundation. Marketplace Average Benchmark Premiums. Kaiser Family Foundation (accessed December 15, 2019). ↩

- 14. Kaiser Family Foundation. 4.2 Million Uninsured People Could Get a Bronze Plan in the ACA Marketplace with $0 Premiums After Tax Credits. Kaiser Family Foundation, December 11, 2018 (accessed December 15, 2019). ↩

- 15. Nierengarten, Mary Beth. Silver Loading: Impact on 2019 Premiums. First Report Managed Care, May 2018 (accessed December 15, 2019). ↩

- 16. Supra note 10. ↩

- 17. Fehr, Rachel, Cynthia Cox and Larry Levitt. Data Note: Changes in Enrollment in the Individual Health Insurance Market Through Early 2019. Kaiser Family Foundation, August 21, 2019 (accessed December 15, 2019). ↩

- 18. Centers for Medicare & Medicaid Services. No Health Insurance? See if You’ll Owe a Fee, The Fee for Not Having Health Insurance. HealthCare.gov (accessed December 15, 2019). ↩

- 19. Kaiser Family Foundation. Enrollment in Individual Market Dips Slightly in Early 2019 after Repeal of Individual Mandate Penalty. Kaiser Family Foundation, August 21, 2019 (accessed December 15, 2019). ↩

- 20. Supra note 17. ↩

- 21. Eibner, Christine, and Sarah Nowak. The Effect of Eliminating the Individual Mandate Penalty and the Role of Behavioral Factors. The Commonwealth Fund, July 11, 2018 (accessed December 15, 2019). ↩

- 22. Kessler, Glenn. The CBO’s Shifting View on the Impact of the Obamacare Individual Mandate. The Washington Post, February 26, 2019 (accessed December 15, 2019). ↩

- 23. Cordina, Jenny, Erica Coe, Kyle Weber, and Elizabeth P. Jones. 2017 Individual Exchange Market Consumer Research Findings. McKinsey & Company, July 2018 (accessed December 15, 2019). ↩

- 24. Tolbert, Jennifer, Maria Diaz, Cornelia Hall, and Salem Mengistu. State Actions to Improve the Affordability of Health Insurance in the Individual Market. Kaiser Family Foundation, July 17, 2019, (accessed December 15, 2019). ↩

- 25. Kaiser Family Foundation. Marketplace Average Premiums and Average Advanced Premium Tax Credit (APTC). Kaiser Family Foundation (accessed December 15, 2019). ↩

- 26. Centers for Medicare & Medicaid Services. How to Get or Stay on a Parent’s Plan, People Under 30. HealthCare.gov (accessed December 15, 2019). ↩

- 27. Norris, Louise. Student Health Insurance: Required Reading. Healthinsurance.org, November 11, 2019 (accessed December 15, 2019). ↩

- 28 Centers for Medicare & Medicaid Services. The Center for Consumer Information & Insurance Oversight, Young Adults and the Affordable Care Act: Protecting Young Adults and Eliminating Burdens on Families and Businesses. CMS.gov (accessed December 15, 2019) ↩

- 29. Mizrachi, Dan. Obamacare Throws Lifeline to Young Adults Seeking Health Insurance. Daily Beast, July 11, 2017 (accessed December 15, 2019). ↩

- 30. National Center for Education Statistics. Percentage of 18- to 24-Year-Olds Enrolled in College, by Level of Institution and Sex and Race/Ethnicity of Student: 1970 through 2017. Digest of Education Statistics (accessed December 15, 2019). ↩

- 31. U.S. Bureau of Labor Statistics. Labor Force Statistics from the Current Population Survey. U.S. Bureau of Labor Statistics, February 21, 2020 (accessed February 24, 2020). ↩

- 32. Supra note 28. ↩

- 33. ADP Research Institute. ADP Annual Health Benefits Report. ADP, 2016 (accessed December 15, 2019). ↩

- 34. Brandeisky, Kara. Why Young Millennials Are Turning Down Health Coverage at Work. Money, April 15, 2015 (accessed December 15, 2019). ↩

- 35. Avery, Kelsey, Kenneth Finegold, and Amelia Whitman. Affordable Care Act Has Led to Historic, Widespread Increase in Health Insurance Coverage. ASPE Issue Brief, September 29, 2016 (accessed December 15, 2019). ↩

- 36. Berchick, Edward R., Jessica C. Barnett, and Rachel D. Upton. Health Insurance Coverage in the United States: 2018. U.S. Census Bureau, November 2019 (accessed December 15, 2019). ↩

- 37. Centers for Medicare & Medicaid Services. What Marketplace Health Insurance Plans Cover, Health Benefits & Coverage. Healthcare.gov (accessed December 15, 2019). ↩

- 38. Norris, Louise. How Obamacare Improved Mental Health Coverage. Healthinsurance.org, July 5, 2018 (accessed December 15, 2019). ↩

- 39. National Women’s Law Center. Women and the Health Care Law in the United States. National Women’s Law Center, May 16, 2013 (accessed December 15, 2019). ↩

- 40. Davis, Elizabeth. Preventive Care: What’s Free and What’s Not. Verywell Health, June 24, 2019 (accessed December 15, 2019). ↩

- 41. National Center for Chronic Disease Prevention and Health Promotion. Health and Economic Costs of Chronic Diseases. Centers for Disease Control and Prevention, October 23, 2019 (accessed December 15, 2019). ↩

- 42. National Prevention Council. National Prevention Strategy. U.S. Department of Health and Human Services, Office of the Surgeon General, June 2011 (accessed December 15, 2019). ↩

- 43. Kaiser Family Foundation. Preventive Services Covered by Private Health Plans Under the Affordable Care Act. Kaiser Family Foundation, August 4, 2015 (accessed December 15, 2019). ↩

- 44. Fox, Jared B., and Frederic E. Shaw. 2015. Clinical Preventive Services Coverage and the Affordable Care Act. American Journal of Public Health 105, no. 1:e7–e10. ↩

- 45. U.S. Department of Health & Human Services. Pre-Existing Conditions. HHS.gov, January 31, 2017 (accessed December 15, 2019). ↩

- 46. U.S. Centers for Medicare & Medicaid Services. At Risk: Pre-Existing Conditions Could Affect 1 in 2 Americans, 129 Million People Could Be Denied Affordable Coverage Without Health Reform. CMS.gov (accessed December 15, 2019). ↩

- 47. Doty, Michelle M., Sara R. Collins, Jennifer L. Nicholson, and Sheila D. Rustgi. Failure to Protect: Why the Individual Insurance Market Is Not a Viable Option for Most U.S. Families. The Commonwealth Fund, July 2009 (accessed December 15, 2019). ↩

- 48. Kaiser Family Foundation. Survey of People Who Purchase Their Own Insurance. Kaiser Family Foundation, June 1, 2010 (accessed December 15, 2019). ↩

- 49. Collins, Sara R. The ACA Protects People with Preexisting Conditions; Proposed Replacements Would Not. The Commonwealth Fund, November 1, 2018 (accessed December 15, 2019). ↩

- 50. Japsen, Bruce. As Trump Strikes at ACA, Employers Sound Alarm on Pre-Existing Conditions. Forbes, March 27, 2019 (accessed December 15, 2019). ↩

- 51. Morning Consult + Politico. National Tracking Poll #180919, September 06–09, 2018, Crosstabulation Results. Morning Consult, September 2018 (accessed December 15, 2019). ↩

- 52. Umland, Beth. New Mercer Survey: Employers Overwhelmingly Support Preserving Coverage for Pre-existing Conditions. Mercer, March 27, 2019 (accessed December 15, 2019). ↩

Copyright © 2020 by the Society of Actuaries, Chicago, Illinois.