Thinking Beyond Price

The importance of assessing counterparty credit risk and strategic alignment in asset-intensive reinsurance transactions

January 2022Photo: iStock.com/shutter_m

Authors’ note: This article presents key factors for insurers to consider when selecting a counterparty to reinsure life and annuity blocks in today’s market, including:

- Putting a price on counterparty credit risk

- Evaluating counterparty strength and contract terms

- Ensuring a long-term collaborative partnership

Just as the pandemic increased consumers’ awareness of the value of insurance, it also increased insurers’ awareness of the value of reinsurance. Recent uncertainty has exacerbated regulatory and economic pressures on life insurance companies supporting capital-intensive life and annuity products. Now more than ever, insurers are utilizing “asset-intensive” reinsurance for a variety of reasons to position their businesses for profitable long-term growth:

- Shifting strategic focus. Reinsurance enables insurers to free up capital from noncore businesses to pursue new areas and execute strategic plans.

- Maintaining a strong financial position. Reinsurance can provide unique solutions to address financial pressures, specifically to meet the challenges of low interest rates and increased liability costs.

- Timing the market. Pricing and terms in the current environment can make a compelling case for executing transactions now to increase returns and accelerate business growth.

Background

“Asset-intensive” reinsurance refers to transactions for which the key element is often performance of the underlying assets—more so than any mortality or other biometric risk. The transactions usually are structured as coinsurance or funds withheld/modified coinsurance, and they often involve reinsurance of annuities, universal life and other savings-oriented products.

For insurers following any or all of these paths, reinsurers are likely to be well-equipped to offer a desirable solution. Many reinsurers have efficient capital structures with appetites for asset-intensive risks, supported by investment expertise and the ability to partner with ceding insurers (cedants) to service long-term contracts. While a growing list of potential providers—including private equity-backed firms and asset accumulators—has emerged in recent years, not all reinsurance counterparties deliver the same level of security. Choosing the wrong counterparty can create credit exposure from the large asset transfer and have costly implications.

Importance of Evaluating Counterparty Credit Risk

Life and annuity reinsurance is a long-term commitment, so a dependable reinsurance partner is critical. The reinsurance industry is built on that premise; however, occasionally a small number of reinsurers have found themselves under unexpected stress. These cases typically have stemmed from misaligned incentives for the reinsurer, leading to poor or even fraudulent decisions. Eventually, these decisions come to light with headlines in the media and financial disruption.

While price is certainly an important consideration, the cedant needs to know above all that the reinsurer will be there when the coverage is needed most. If a reinsurer does not have sufficient funding to cover reinsured claims, those claims come back to the cedant, typically through a “recapture” event. Once a reinsurer’s insolvency or default triggers recapture, the insurer must:

- Cover any financial losses.

- Post risk capital to support the recaptured business.

- Assume responsibility for the investments backing the business.

- Take legal action to try and recoup losses.

- Review the situation with regulators.

- Explore a new long-term strategy for recaptured business.

Working through all of these steps can take a number of years—with the outcome uncertain. A recapture event on its own is clearly not ideal. It is also more likely to occur when business operations and/or financials are already under stress from a market downturn or other negative events, which drives additional losses from the suddenly increased asset exposure.

Counterparty credit strength is therefore a major consideration in any reinsurance transaction, and it is critical to understand these downside risks in selecting a reinsurance partner. A cedant may have the choice between several different types of asset-intensive reinsurers, ranging from highly diversified, experienced professional reinsurers to offshore mono-line startups supported by asset managers and/or private equity. This presents a variety of trade-offs among price, terms and exposure limits that should be reviewed and, when possible, quantified as part of the decision-making process.

Framework for Quantifying the Cost of Reinsurance Counterparty Risk

On the surface, the cost of reinsurance appears to be simply a reinsurer’s quoted price to assume defined reserves and risks. The true cost, however, must account for counterparty credit risk, especially given the differences in creditworthiness among potential partners.

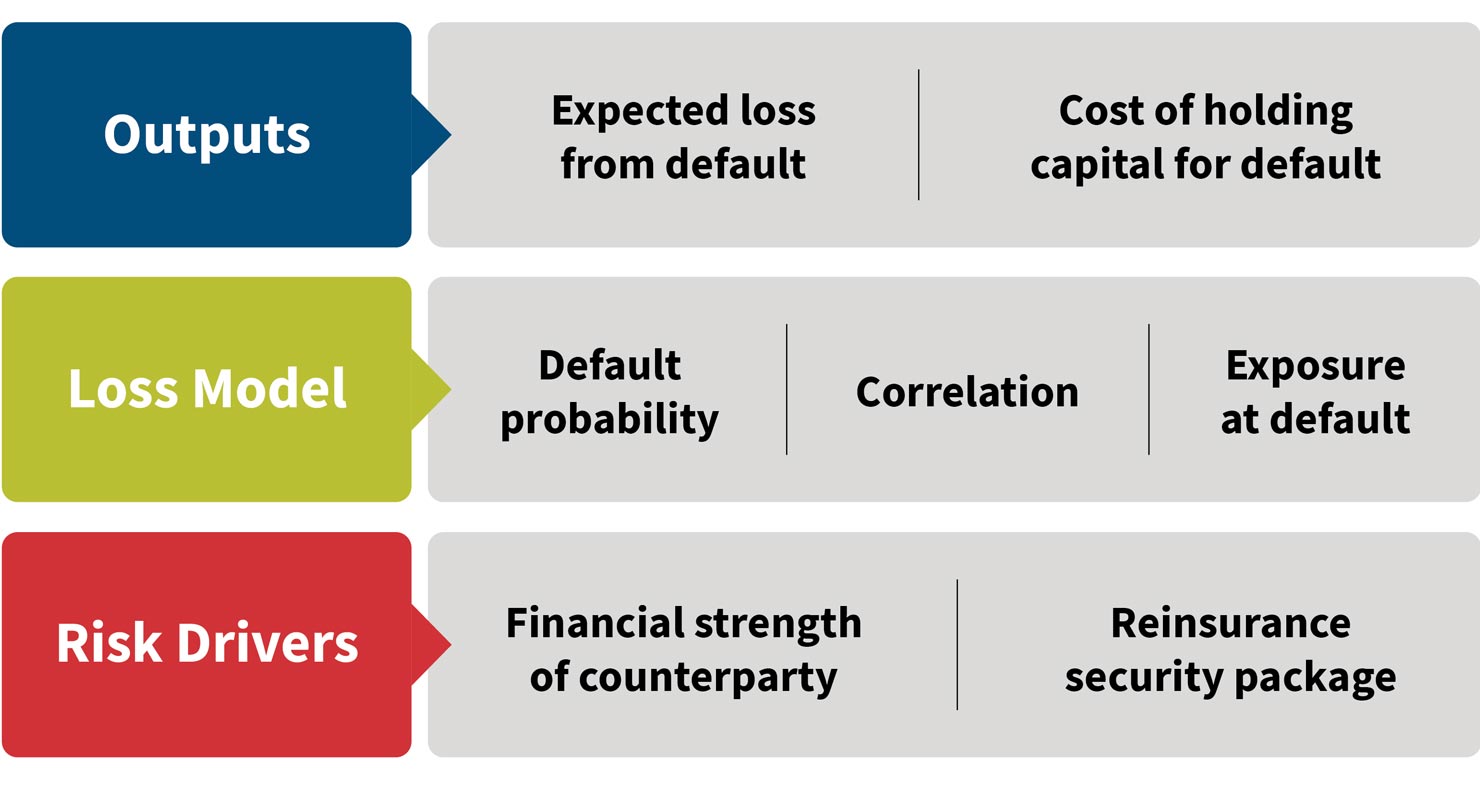

The cost of reinsurance counterparty risk can be quantified based on two components: the expected loss from counterparty default and the cost of holding capital for counterparty default, where the capital covers a tail loss, typically at the 99.5th percentile (see “Outputs” in Figure 1). In theory, the price adjustment for reinsurance counterparty risk should reflect the present value of these costs over the life of a reinsurance transaction. The loss from counterparty default is a product of the probability of default and exposure at default, which are primarily driven by the financial strength of the counterparty and the underlying security package, respectively.

Figure 1: Cost of Counterparty Risk: Building Blocks

The key question in assessing financial strength is: Will the reinsurer be able to cover the losses in a stress scenario? Among several factors to consider is the diversification of the reinsurer. A reinsurer with a diversified balance sheet designed to survive market stresses is better equipped to navigate an economic downturn. It is important to remember the insurer is paying for risk transfer in the event things go badly—not well.

Financial strength’s connection to probability of default can be observed over time based on documented default rates, with clear variation by industry. As shown in Figure 2, insurance companies historically have produced consistently low default rates (with the exception of the early 1980s), likely due to an emphasis on risk management and oversight. Default rates for the financial industry have been higher on average, in addition to being more exposed to the market environment and asset prices. During the 2008 market crash, the insurance industry saw limited deterioration in credit quality, much less the rate of insolvency. Financial companies, on the other hand, experienced a significant spike in defaults.

Figure 2: Historical Default Rates for the Financial and Insurance Industries

Sources: S&P Global Ratings Research and S&P Global Market Intelligence’s CreditPro®

© 2022 by Standard & Poor’s Financial Services LLC. Reprinted with permission.

Companies often turn to credit ratings from the major ratings agencies (S&P, Moody’s, A.M. Best and Fitch) to help determine financial strength. Ratings considered should be those assigned to the specific legal entity serving as the direct counterparty, as opposed to the ratings of the parent company. Ratings combine quantitative and qualitative factors, such as the support from a parent company and strategic significance of the reinsurance operation. In some cases, company ratings can be less established or a company may not be rated by all (or any) of the major rating agencies, both of which require additional due diligence.

As an illustration of the differences in financial strength, Figure 3 shows the S&P credit risk capital factors for 10-to-20-year bonds with different credit ratings, which represent the worst-case credit loss over an annual period at a 99.7 percent confidence level at different ratings and tenors. The factors increase materially for lower ratings, with BBB having nearly four times the risk charge of AA.

Figure 3: S&P Capital Factors by Credit Rating

| Rating | Capital Factor |

| AA | 1.61% |

| A | 2.16% |

| BBB | 5.84% |

| BB | 24.64% |

The security package a reinsurer offers is often customized and negotiated between the two parties of a transaction. The specific terms and provisions of a security package may include some of these elements:

- Dedicated collateral through a trust or funds withheld

- Quality of the investment portfolio, including credit, liquidity and duration

- Advanced recapture and top-up provision, although the counterparty risk analysis must consider the ability and willingness of the reinsurer to honor such provisions in a stress scenario

- Credit enhancements, such as letters of credit and parental/external guarantees

A crucial component of a credit risk model is the assumed correlation between the probability of default and the loss based on the underlying security package. For diversified reinsurers, stress scenarios that cause a deficiency in the collateral are less likely to be the same drivers of insolvency. Less-diversified reinsurance counterparties, on the other hand, may have significant levels of related exposure to the same stress scenario. These counterparties may be forced to make difficult decisions for nonstrategic operations when resources are scarce.

Given these factors, it is possible that while two reinsurers may offer the same level of trust funding and allocation to investment-grade bonds, their relative financial strength can lead to significant differences in the cost of the counterparty credit exposure. As a byproduct, the cost for a lower-rated reinsurer will be more sensitive to the security package, requiring additional scrutiny of the modeled asset stresses and other assumptions.

As highlighted in the illustrative example in Figure 4, more aggressive asset allocations result in a nearly 2 percent higher counterparty credit risk price adjustment for the lower-rated reinsurer. To make up for this, Reinsurer 2 will need to offer a commensurately lower price on the reinsurance or materially bolster the security package.

Figure 4: Sample Price Adjustments for Counterparty Credit Risk

| Reinsurer 1 | Reinsurer 2 | |

| Credit Risk (Illustrative) | AA-rated Onshore Reinsurer | BBB-rated Offshore Reinsurer |

| Conservative Allocation | + 0.3% | + 1.4% |

| Aggressive Allocation | + 0.4% | + 2.0% |

Illustration based on sample asset-intensive reinsurance transaction for a fixed deferred annuity block with a duration of 12 years. Asset allocation assumed to be the same between reinsurers at approximately 95 percent and 80 percent investment grade for the conservative and aggressive allocations, respectively.

Key Considerations When Selecting a Reinsurance Counterparty

Beyond raw numbers, there is much more to consider when partnering with a reinsurer than comparing strictly quantitative measures, such as ratings and quality of collateral. Cedants should only enter an asset-intensive reinsurance transaction with a counterparty upon which they can rely. More nuanced, and often more important, considerations include:

- Long-term commitment to the market. Will the reinsurer be able and willing to raise future capital to meet demands if needed? Is this business strategic or merely opportunistic to the reinsurer’s parent company?

- Ability to honor the terms of the agreement. If a reinsurer is liberal on terms and underwriting with one client, this same liberal approach likely carries over to the reinsurer’s other clients. Will the reinsurer be able to meet all future obligations—particularly in the scenario when needed most?

- Partnership mindset. Asset-intensive transactions can be complicated to complete and involve long and complex contracts that inevitably will need to be revisited, so the value of a true partner looking to build a lasting relationship and win-win solutions cannot be overstated. Does the counterparty have the capability and resources to execute the deal on their quoted terms and address any emerging issues on a mutually beneficial basis? Will they continue to work with the cedant fairly as a partner years in the future? Does the reinsurer have credible experience to prove this commitment to partnering on asset-intensive reinsurance?

Answering these important questions provides a more holistic counterparty assessment and can help cedants avoid entering a transaction in which the reinsurer later proves incapable of meeting obligations when financial pressures arise. The right reinsurance partner also can develop a range of customized options to meet an insurer’s specific business needs. This is where capacity meets capabilities.

Conclusion

The growth of asset-intensive reinsurance in recent years has led many new providers to enter the market. Without an established track record, however, these new entrants’ ability to withstand the test of time has yet to be determined, especially as they have not experienced an extended and severe market downturn. While these new players may offer better terms up front, they also may bring greater risk in the long term.

On the other hand, established, proven players in the asset-intensive space bring experience, added security and a commitment to servicing complex contracts. Such reinsurers have varying levels of diversification and degrees of exposure to financial markets, which is the predominant risk for asset-intensive reinsurance.

As with insurance for policyholders, reinsurance exists to support cedants when the unexpected happens—when circumstances take a turn for the worse. More than anything, an insurer needs to know its reinsurer will be there to honor commitments when called upon. A careful and comprehensive evaluation of counterparty risk can make the difference between a transaction that fuels an insurer’s long-term growth and one that leaves the insurer facing unsustainable losses.

Statements of fact and opinions expressed herein are those of the individual authors and are not necessarily those of the Society of Actuaries or the respective authors’ employers.

Copyright © 2022 by the Society of Actuaries, Chicago, Illinois.