What Were They Thinking?

Actuaries respond to the human side of longevity

August/September 2017The traditional job of actuaries includes measuring mortality; building mortality tables; and designing, pricing and conducting financial analysis for products with a longevity component. However, actuaries also are involved with the human side of longevity. This article will provide details on several projects from the Society of Actuaries (SOA) that are focused on this human side of longevity. Projects include research from the SOA’s Committee on Post-Retirement Needs and Risks, an actuarial longevity calculator, the Living to 100 and Beyond project and sponsorship of the Sightlines Project.

Why Should Actuaries Care?

Before discussing the specific projects, think about why actuaries would want to know about these issues. We know that people, at times, do not make decisions as rational economic beings, and we know quite a lot about the drivers of decisions. In a world where retirement security quite often depends on personal savings and defined contribution plans, the decisions individuals make—and their knowledge about longevity—are extremely important.

Actuaries are involved with a number of services and programs for this period later in life. These programs and services usually are focused on financial security and financing of health and long-term care benefits. But achieving success in old age is about more than money. Insights on the human and nonquantifiable aspects of aging enhance the chance that the programs and services with which actuaries are involved will be successful.

Projects from the Committee on Post-Retirement Needs and Risks

An ongoing public attitude survey research program enables us to understand how the public perceives and expects to manage risks associated with longer life. The program provides insights into the human aspects of longevity and how people feel and expect to act as they age. This research demonstrates that, for many people, action is a result of factors such as knowledge and feelings rather then purely being a mathematically-driven activity. While actuarial and mathematical analysis is an important driver of behavior for some people, it plays no role at all for others. This research program includes a biennial survey; three sets of focus groups, including focus groups with individuals who had been retired for 15 years or more in 2015; and some in-depth interviews. In 2015, in-depth interviews also were conducted with caregivers of people requiring long-term care.

The work of the committee through 2015 provides a strong indication of the human story. In 2017, late-in-life interviews will be conducted with retirees older than age 85 and, in some cases, their children. This 2017 work will fill a gap, focusing on the period usually missed in such research.

Findings From the Committee on Post-Retirement Needs and Risks

Some key findings from the Society of Actuaries’ (SOA’s) Committee on Post-Retirement Needs and Risks public attitude research include …

CONTINUE READING

Many of the findings from the committee’s public attitude research (see “Findings” sidebar) can be explained by “behavioral finance,” a scientific study of how people make financial decisions and behave. This is in contrast to traditional economics, which predicted that people would figure out the best solution for themselves and make the rationally economic choice after doing the analysis. During the last 30 years, we have learned a lot more about behavioral finance and its influence on financial decision-making.

The Longevity Calculator and Understanding Longevity

Understanding longevity is a challenge. The Post-Retirement Risk Survey indicates that more people underestimate longevity than get it right, and that many plan for too short of a period. Even those people who reasonably understand longevity often plan for too short of a time period, often much shorter than their lifetime horizon.

It is difficult for many people to remember that longevity is uncertain. If a large group of people all retired at age 70, a few will die in the year after retirement and a few will live beyond age 100. If a group of people all knew their average life expectancy and planned to use their money by that date, then about half of them would have planned a future where they run out of money.

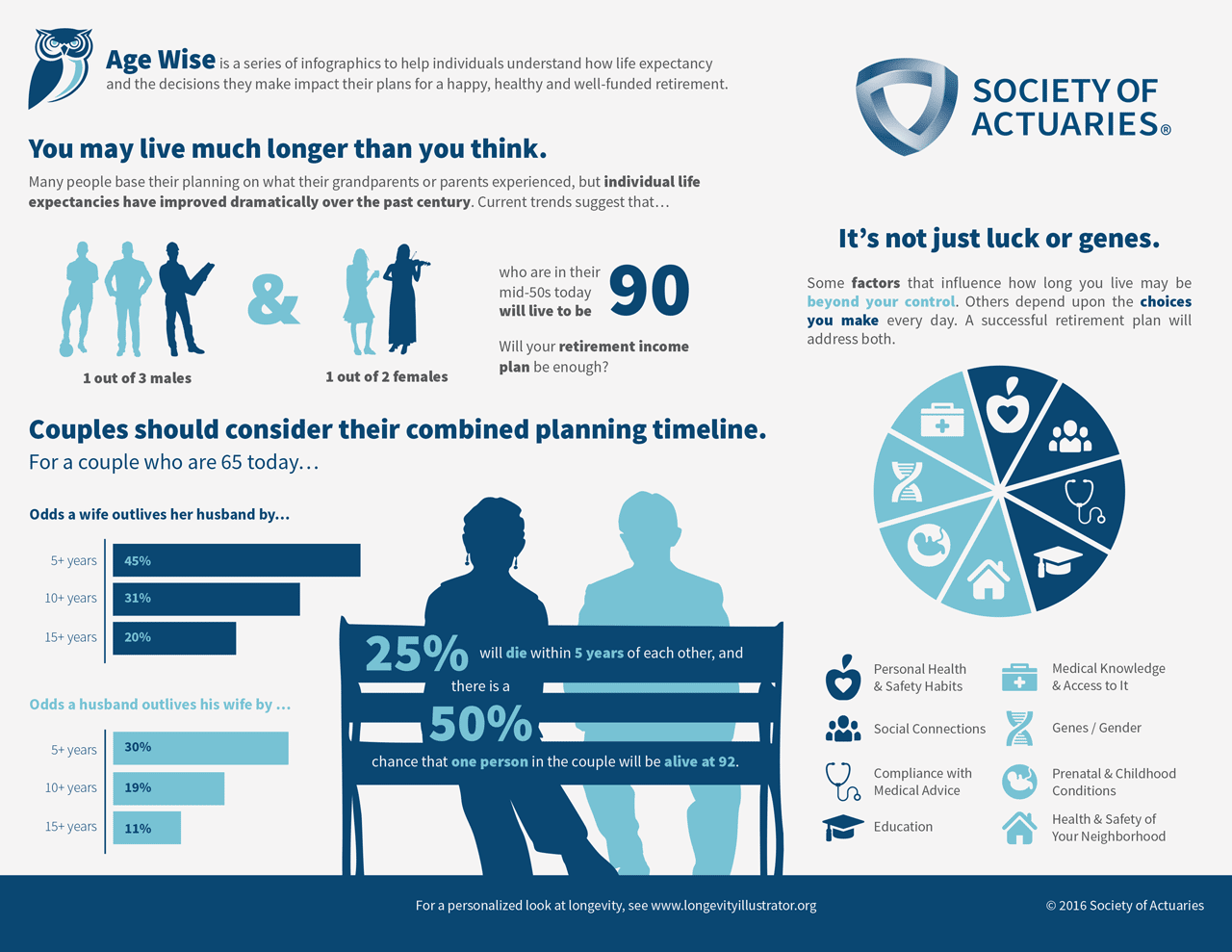

The SOA and the American Academy of Actuaries (the Academy), working jointly, produced the Actuaries Longevity Illustrator. This tool allows the user to calculate his or her expected lifetime, taking into consideration health status as well as age. For couples, the results include the probability of living to a various number of years—for each member of the couple, for either or for both. The charts help people understand the variability of life expectancy.

The Committee on Post-Retirement Needs and Risks created two different sets of materials to help with understanding longevity-related issues. One of the special topics in the 2015 Post-Retirement Risk Survey was understanding longevity, and there also is a special report on that topic. In addition, the committee prepared several infographics to be used with the tool, for various audiences who need to understand longevity. The first infographic is shown as Figure 1. Its key messages are:

- People may live longer than they think.

- Couples need to think about their joint longevity.

- A variety of factors contribute to longevity.

Figure 1: SOA Age Wise Longevity Infographic

Click to enlarge

The Sightlines Project

The Stanford Center on Longevity, together with a number of sponsors, including the SOA, conducted the Sightlines Project. This project is focused on helping people enhance their chances of living an independent 100-year life. The project investigates how well Americans are doing in three areas the research identified as critical to well-being as people age: financial security, healthy living and social engagement. While financial security and health have long been recognized as part of successful retirement, many people have not recognized the importance of social engagement. The findings are based on analyses of data from several large studies. The project includes recommendations for improving results in each area. It also identifies specific points on which progress is needed, as well as areas where Americans are doing well. The project is very exciting because it includes data and indicators that can be measured over time. These results are intended to stir national debate, guide policy development, stimulate entrepreneurial innovation and encourage personal choices that enhance living independent, 100-year lives.

The Living to 100 and Beyond Research Program

The SOA has sponsored a research program titled “Living to 100 and Beyond” for the last 15 years. This is a space for new ideas, exchange of information, controversies, learning how other disciplines view related issues, and identifying points of agreement and disagreement. The cumulative program output since 2002 includes more than 150 scientific papers, a number of presentations and panel discussions, and six symposia. The symposia, which occur every three years, bring together a diverse group of experts with varying perspectives on the need to understand changing life expectancies and adapt to longer life expectancies. One of the features of the 2017 Living to 100 Symposium was emphasis on improving living conditions and the human side of longevity.

ACCESS ADDITIONAL INFORMATION ABOUT LIVING TO 100

For each of the six Living to 100 symposia, there is a monograph on the Living to 100 website. The 2017 monograph that includes the new papers should be posted late in 2017.

Presentations from 2017 can be found embedded in the program on the website. All of the papers from 2002 to 2014 and the findings are summarized in a report prepared by Ernst and Young. This report is split between technical issues and implications. The report also highlights areas of agreement and differences, and it includes abstracts for all of the published papers in an appendix.

At the 2017 Living to 100 Symposium, a key topic related to the human side of longevity was “The Changing Face of Eldercare,” which focused on big ideas: making communities friendly to an aging population and steps that support people staying in the community longer. The World Health Organization (WHO) established a program of age-friendly communities and a process to help communities become more age-friendly. The eight domains of an age-friendly community are community and health care, transportation, housing, outdoor space and buildings, social participation, respect and social inclusion, civic participation and employment, and communication and information. There are 332 age-friendly cities today in 36 countries. The AARP is the U.S. affiliate of this network. The AARP program focuses on safe, walkable streets; age-friendly housing and transportation options; access to needed services; and opportunities for residents of all ages to participate in community life. Age-friendly communities do not replace the need for senior housing and nursing homes, but they give people new options and may make it feasible for them to stay active in the community longer.

Another trend focused on helping people live in their communities longer is the “Village” movement, or the formation of neighborhood-based groups for seniors that support people aging in the community. Such organizations are based heavily on volunteerism and people helping each other. The first village was formed in Boston in the Beacon Hill neighborhood in 2002. My view is that villages are very helpful and can supplement and take the place of extended family for seniors who need to be part of a support network where they live.

Public Policy Issues

Population aging is changing the fabric of our societies and affects many areas of policy. Much of the policy deals with human issues. Many societies are focused on helping people age successfully, and public programs offer some level of financial support and support for health care. They may offer additional support for the elderly. At the 2017 Living to 100 Symposium, major public policy issues related to aging were the subjects of a panel on big-picture issues. That panel provided perspectives from the United States, the United Kingdom and Canada.

David Sinclair, director of the International Longevity Center in the United Kingdom, provided insights into several big policy challenges in the United Kingdom. They include meeting the cost of aging, saving more, providing an adequate workforce, getting older people to spend more, delivering health and care (which we would call long-term care or long-term services and supports), maximizing the opportunity of technology and responding to the issues surrounding housing wealth. In my view, there is a major overlap with big underlying issues in the United States. These issues are all closely connected to human issues linked to aging.

Robert Brown, retired professor from the University of Waterloo, provided insights into the aging issues getting attention in Canada. Social Security benefits recently have been increased, and after an attempt to raise the retirement age, the legislation was reversed. The majority of the public does not have employer-sponsored benefits. There are challenges in the efficient and effective delivery of health and long-term care. Canada seems to be going in a different direction than many countries by increasing social benefits.

John Cutler, an attorney and senior fellow at the National Academy of Social Insurance, pointed to the huge uncertainty in the United States linked to the 2016 presidential election. Concern about jobs, particularly among mid-career people and those nearing retirement, as well as flat or declining wages seemed to be very important in the election. But other than encouraging manufacturing in the United States, it is unclear what, if anything, will be proposed to address these issues. The federal government plays a huge role in health care, and it is unclear how that role may change going forward. Proposals to modify that role are a high priority in the new administration, but there is no consensus about the replacement programs. Less visible but also very important are the need to bring Social Security into financial balance and several pension issues.

Conclusion

Actuaries are very familiar with measuring and projecting mortality and using information about longevity for financial analysis. But success with respect to management of longevity by many different stakeholders requires a greater understanding of longevity by individuals as they make decisions, consideration of what people think about when they plan for the future, and an understanding of what can make life better as people age.