HDHL Medical Insurance in China: Part 2

Further insights into a popular and essential product in the commercial medical insurance market

September 2021Photo: iStock.com/fatido

The article “HDHL Medical Insurance in China: Part 1,” published in August 2021, explored hot topics in the Chinese commercial medical insurance market, including high-deductible, high-limit medical reimbursement insurance plans (HDHL, or 百万医疗in Chinese). The article provided a market overview for HDHL plans and risk factor analysis based on sales strategy and geographic locations.

Here in Part 2, more risk factors—such as disease spectrum, patient behavior analysis and the impact of COVID-19 on the medical insurance industry—will be the focus. You may want to refer back to Part 1 to familiarize yourself with helpful background material as you continue your reading journey.

Analysis of HDHL Claim Cause

Different HDHL plans have different claim cause distribution across the disease spectrum. The deductible amount is one of the key factors.

The difference in claim cause between zero-deductible products and high-deductible products is shown in Figure 1. Obviously, the proportion of malignant neoplasms (tumors) is significantly higher in high-deductible products than in zero-deductible products due to the thick tail distribution on HDHL claim expenses.

Figure 1: Cause of HDHL Claims

Hover Over Image for Specific Data

Data source: Experience analysis of several HDHLs in the Chinese market

In addition to the deductible amount, the deductible type is noteworthy. There are two typical deductible types in HDHL: absolute deductible and relative deductible. Absolute deductible means the reimbursement from the social health insurance program (SHIP) is not considered. In the case of a relative deductible, SHIP reimbursement is factored in.

For example, an insured who has an HDHL with a 10,000 CNY deductible received a 7,000 CNY reimbursement from SHIP. In this instance, the absolute deductible remains 10,000 CNY, but the relative deductible becomes 3,000 CNY. This is why relative deductible is considered dynamic. In general, the product with a relative deductible of 10,000 CNY and the product with an absolute deductible of 2,000 CNY are equivalent. To better understand the impact of deductible type across the disease spectrum, see Figures 2 and 3.

Figure 2: Absolute Deductible Expenses Paid by Disease Category

Hover Over Image for Specific Data

Data source: Experience analysis of several HDHLs in the Chinese market

Figure 3: Relative Deductible Expenses Paid by Disease Category

Hover Over Image for Specific Data

Data source: Experience analysis of several HDHLs in the Chinese market

The proportion of malignant neoplasms claimants who have an absolute deductible is higher than those who have a relative deductible, which is consistent with the findings on deductible amount. The total medical cost level per claimant for absolute deductible by each disease category is generally higher than the relative deductible, which means the disease claimed in products with absolute deductibles is more severe than those with relative deductibles.

Furthermore, malignant neoplasms are the main cause of HDHL claims and continuing claims. The higher the number of continuing claims, the higher the incident rate will be in the following policy year. Also, the severity will increase with the proportion of malignant neoplasms claimants increasing. Overall, the average net cost tends to increase constantly. According to industry data, the proportion of malignant neoplasms claimants is 20 percent to 25 percent, 27 percent to 30 percent, and 33 percent to 35 percent in each policy year.

Insights on SHIP’s Emphasis From HDHL Claim Study

Generally, the claim payment in HDHL is total medical expenses minus reimbursement from SHIP and the deductible. The ratio claim payment over total medical expenses is commonly used to measure how protective the product is, which is referred to as the protection value. A high protection value demonstrates a powerful safeguard from HDHL. It varies by policy year and claim cause, and it is generally 30 percent to 40 percent. See Figure 4.

Data source: Experience analysis of several HDHLs in the Chinese market

The protection value goes up as policy years pass, so the insured could benefit by holding the product for a long period. As for claim cause, the protection value is extremely high when the claim is caused by malignant neoplasms and accidents. In other words, the benefits from SHIP for accidents and malignant neoplasms are insufficient. It is a result of two fundamental principles of SHIP: essential coverage and sustainable development. Based on that, SHIP mainly focuses on general disease treatment rather than accident. Subject to limited funds, SHIP can hardly afford the high costs of malignant neoplasms treatment. So using HDHL to cover these kinds of expenses outside of SHIP is popular in the Chinese market.

Analysis of Insured Behavior Changing in HDHL

Insured behavior depends on factors like medical accessibility, seriousness of disease, personal financial situation and so on. HDHL insureds do not need to worry about expensive medical costs, so they are inclined to choose the high-class hospital and advanced treatment—opposed to similar patients who only have SHIP coverage, as shown in Figure 5.

Figure 5: Choice for Different Tier of Hospitals

Hover Over Image for Specific Data

Data source: National Healthcare Security Administration (NHSA) public data and experience analysis of several HDHLs in the Chinese market

As shown in Figure 5, 79 percent of HDHL insureds choose to visit a tier-3 hospital, which is a much higher number of insureds than those who only have SHIP coverage. On the one hand, HDHL claims are more closely related to critical disease because of the high deductible, and medical resources for critical disease typically are centralized in tier-3 hospitals. On the other hand, without the concern of expensive medical costs, HDHL insureds tend to visit costly tier-3 hospital more often in general. Similarly, the average inpatient medical expense in HDHL is higher than in pure SHIP coverage, as shown in Figure 6.

Figure 6: Average Inpatient Medical Expense per Visit

Hover Over Image for Specific Data

Data source: National Healthcare Security Administration (NHSA) public data and experience analysis of several HDHLs in the Chinese market

Trend Study on Cost per Head of HDHL

When talking about medical costs increasing, it is worth mentioning medical inflation. Like the interest rates in common financial products, medical inflation varies within different medical insurance products. Research indicates that general medical inflation in the Chinese market is 6 percent to 8 percent. But when applied to HDHL average net cost, inflation is underestimated.

To make it clear, trend is used to represent the yearly cost increase per head in HDHL. Trend could be broken up into new business trend and in-force business renewal trend. In this article, the focus is only on the in-force business renewal trend.

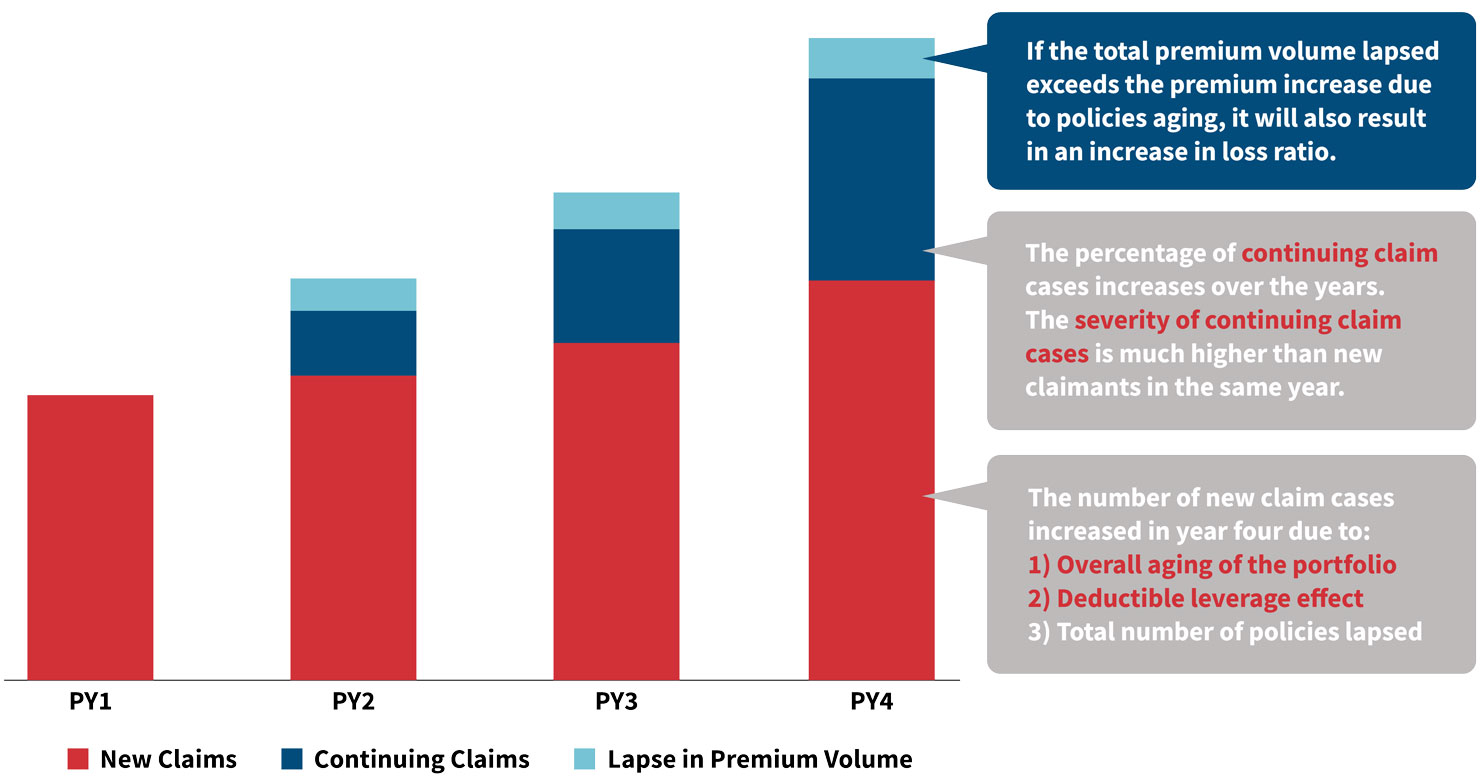

Renewal trend consists of three main parts: new claims, continuing claims and premium volume dropping due to healthy insured surrender.

In Figure 7, continuing claim cases are the major reason for renewal, and this trend is consistent with previous analysis. The probability of continuing claims in HDHL is higher than in common medical insurance products since its claim cause is more serious. In practice, the probability of continuing claims in HDHL is around 60 percent when the claim is caused by malignant neoplasms.

Figure 7: Medical Loss Ratio Analysis

Data source: Experience analysis of several HDHLs in the Chinese market

The second renewal trend is newly occurred claims. Considering the deductible leverage and the increasing average age of insureds, the rate of newly occurred claims is also growing year by year.

The last factor to consider is the decrease of premium volume due to healthy insured surrender. Thus, persistency management is important when running HDHL—especially the persistency of healthy insureds. Selective lapse of healthy insureds could bring about an insufficient premium issue and result in a booming loss ratio.

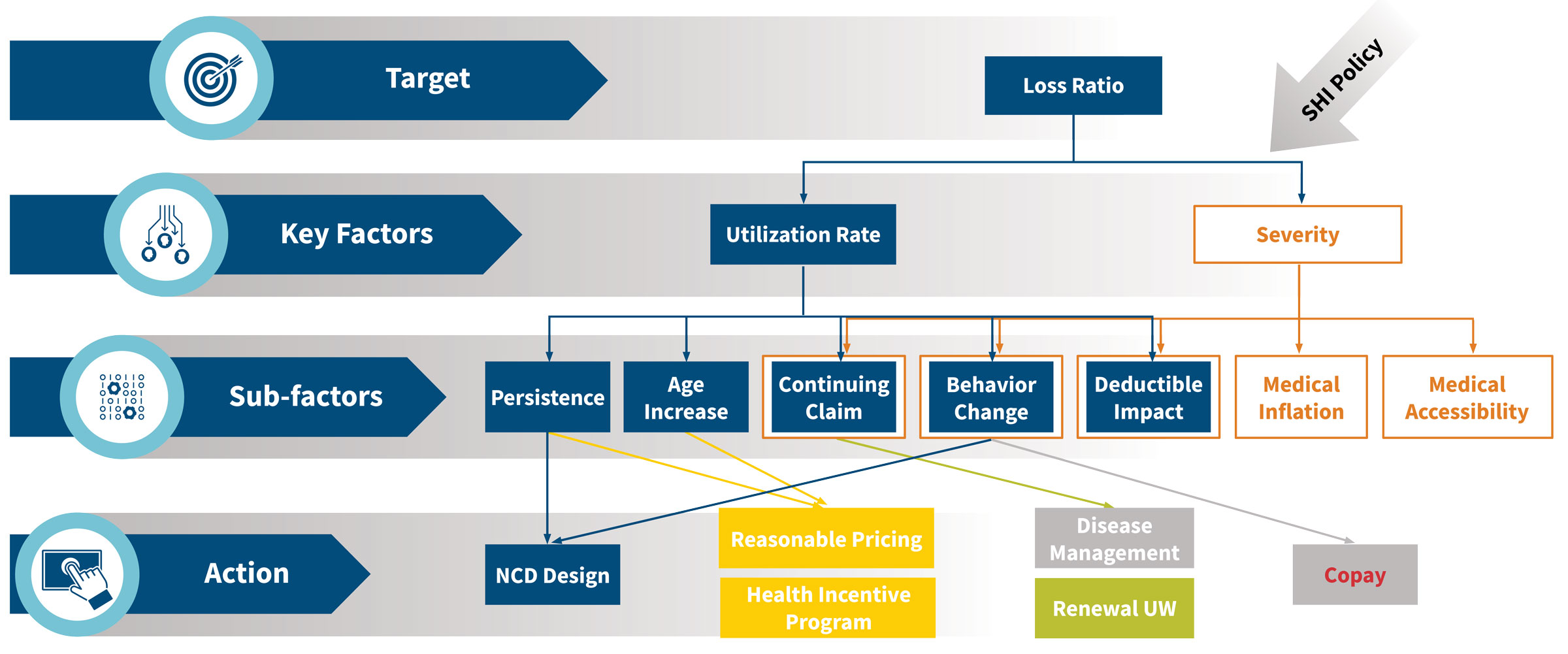

Based on these factors, the industry trend in HDHL is about a 30 percent loss ratio. However, it varies from 20 percent to 80 percent depending on the product, and it can even be more than 100 percent in extreme occasions. To better understand the difference, Figure 8 takes a deep dive into key elements affecting trend.

Figure 8: Trend Breakdowns for HDHL

In HDHL, loss ratio mainly depends on premium rate, benefits utilization rate and severity per visit. These three elements are accordingly influenced by persistency, deductible design, continuing claims, behavior change, age increases, medical inflation and medical accessibility.

Persistency is a high-impact factor on loss ratio and a key performance indicator in an insurance company. When healthy insureds lapse selectively, the utilization rate will grow significantly and eventually lead to the loss ratio growing as well. If this scenario lasts for a long time, the medical insurance product will go into a death spiral—like how bad money drives out good according to Gresham’s Law. According to data analysis, loss ratio is linear with persistency when persistency is within a specific narrow range, such as more than 70 percent. For example, when persistency turns from 75 percent to 70 percent, loss ratio will go up 5 percent. But when persistency is below 70 percent, the influence on loss ratio will be expanded.

Deductible design is also a high-impact factor on loss ratio since it determines the benefits utilization rate—the higher the deductible, the lower the utilization rate. However, high deductibles lead to a problem known as deductible leverage impact.

Deductible leverage impact means the utilization rate under a high-deductible plan increases much faster than the population as a whole. For instance, a product with a 100 CNY deductible covers three people whose medical expenses are 110 CNY, 95 CNY and 70 CNY, respectively, in the first policy year. Their claims that first year are 10 CNY, 0 CNY and 0 CNY, and the utilization rate is 33.3 percent. Assuming 10 percent annual medical inflation, the medical expenses in the second policy year will be 121 CNY, 104.5 CNY and 77 CNY, and the claims will be 21 CNY, 4.5 CNY and 0 CNY. The utilization rate will be 66.7 percent, which is double compared to the first year. In this example, the utilization rate increases 100 percent, which is much higher than the pure medical inflation rate of 10 percent—this is the deductible leverage impact.

Continuing claims also contribute greatly to loss ratio, and behavior change cannot be ignored. Patients who have HDHL coverage tend to choose superior hospitals and costly treatment, which can result in an abuse of medical resources. For example, an insured who has thyroid cancer chose to have proton and heavy ion therapy after surgery to remove the cancer—medically, this is considered overtreatment. But this patient still received a full claim payment, and the overtreatment generated an extra 300,000 CNY claim for the HDHL plan.

The final major factor for loss ratio is an unreasonable premium rate. Confronted with market competition and various distribution channels, insurance companies must adopt different pricing strategies to target clients in different age bands.

Pricing for people older than 50 is more radical than pricing for younger people. The premium deficiency in this higher age band produces a high loss ratio. Even though there is a premium increase tied to age risk, the loss ratio is increasing rapidly due to the premium deficiency of aged people. Furthermore, the mainstream HDHL in the Chinese market is priced by age band, and there usually are five ages in a band, so premium rate remains the same when age increases within an age band. However, the average cost per member per year increases 5 percent for each year aged. From this perspective, pricing by age band brings about an additional increase in loss ratio.

Facing these challenges, the various players in the Chinese market have taken a variety of actions. In long-term medical insurance products, some insurance companies have started to price by exact age instead of age band and adjust the premium curve to overcome the premium deficiency of older people.

Overall, HDHL is still new to the Chinese market and profitable. Most insurance companies have not realized they are supposed to take action to deal with the rapidly rising loss ratio. Loss is starting to occur in the first HDHL that launched in 2016. Several actions have been taken proactively with the help of regulatory policies, such as “Short-term Health Insurance Regulation” and “Long-term Rate Adjustable Medical Insurance Product Regulation.” Predictions say the short-term product will no longer be the only major medical insurance, but rather it will coexist with 10-year or longer rate adjustable products and five- or six-year rate fixed products.

National Regulation and the Impact of COVID-19

In addition to this micro-perspective on product analysis, the macro-view of regulatory policy and public emergency’s influence should also be considered. Namely, what is the impact of the COVID-19 pandemic?

“Health China 2030” is designed to prevent disease instead of providing therapy. Prevention keeps the source of disease under control, which means medical expenses are controlled. More and more, advanced health screenings are being promoted, and SHIP is even covering some of these. Additionally, the National Healthcare Security Administration takes strategic actions—such as massive purchasing and future diagnosis-related groups (DRGs)—to maintain a sustainable SHIP foundation. These actions will also indirectly influence HDHL claims in the long term.

National SHIP is limited by the fundamental principles of essential coverage, sustainable development and mass participation. For urban employees, SHIP individual account reform is aimed at improving outpatient coverage by adjusting the system design. In this view, it provides a theoretical foundation for commercial medical insurance to promote outpatient coverage. In addition, drawing on international experience, DRGs are helpful to control medical expenses in the short term, but it is hard to be effective in resisting medical inflation in the long run.

In 2020, countries all over the world suffered from COVID-19, and a corresponding impact is reflected on medical expenditures. The Chinese government has taken proactive actions against epidemics and brought the related treatment into SHIP coverage. As of July 19, 2020, the total number of medical cases reimbursed through SHIP had reached 136,000 CNY for both confirmed and suspected cases. Total medical expenses for COVID-19 in 2020 were 2.84 billion CNY, and the SHIP foundation paid 1.63 billion CNY (57.4 percent). Other government institutions paid most of the remaining costs, and COVID-19 patients paid very little.

Fifty-nine insurance companies in China have published their COVID-19 claims report for 2020 with total COVID-19 claim payments of 215 million CNY, which is equivalent to 13.2 percent of total SHIP expenditure. The average claim cost per claimant was 41,000 CNY. Most of the claim payments are from life insurance products given to health care providers/medical staff, but some are also from critical illness (CI) products. Both of those products are not for medical treatment, but for one-time payments for death or CI conditions.

Figure 9: COVID-19-Related Claim Summary

| 2020 Claim Payment From 59 Insurance Companies | CNY |

| Total claim | 215 million |

| Total cases | 5,236 |

| Claim amount per case | 41,000 |

| Claims for health care workers | 91 million |

| Cases for health care workers | 2,042 |

| Claim amount per case | 45,000 |

| Claims for commercial insurance products | 124 million |

| Cases for commercial insurance products | 3,194 |

| Claim amount per case | 39,000 |

Data source: Public claim reports from 59 insurance companies in China

Conclusion

Following the new regulatory policy, commercial medical insurance is a long-term trend in the Chinese market. Insurance companies are required to take the medical cost inflation into consideration and optimize their medical insurance operations. Chinese commercial medical insurance will come into the era of delicacy management in the foreseeable future.

Acknowledgments

Special thanks to those who contributed their knowledge and expertise in the preparation of this article:

- Chloe Wang, FSA

- Pricing actuaries Xin Chang, ASA; Xiaoyu Ding; Yingfei Ma, ASA; Xue Sheng and Teng Zhang

- Members from the Experience Analysis and Marketing teams from the SCOR Beijing Branch

Statements of fact and opinions expressed herein are those of the individual authors and are not necessarily those of the Society of Actuaries or the respective authors’ employers.

Copyright © 2021 by the Society of Actuaries, Chicago, Illinois.